Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

PLN

EUR/PLN has edged lower despite the generally dovish reception of macroeconomic data released out of Poland. The pair operates -136 pips at 4.4627, staying within its recent trading range. It has been trapped between 4.45-4.50 for the past week.

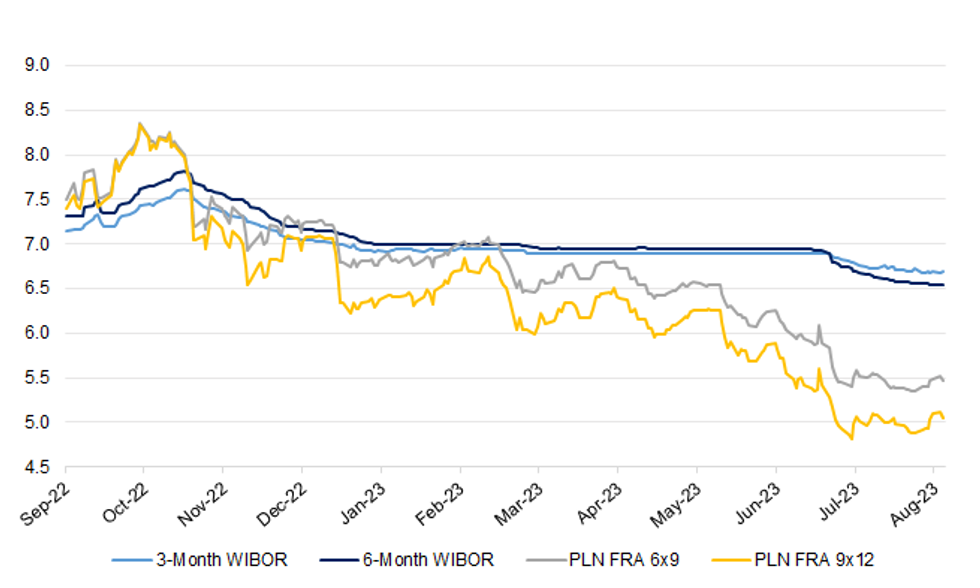

- Economic activity data from the start of the week have been interpreted as supporting the dovish wing of the MPC. Santander wrote this morning that "the recent weak economic data increase the probability of a rate cut in September," even as their baseline scenario is for a cut in October. Separately, mBank said that PPI deflation coupled with weak data from the real economy may encourate the MPC to lower rates in September, with such a scenario becoming increasingly likely with incoming data. According to Bank Pocztowy, data released this week "will serve part of the MPC as an argument for starting rate cuts in September," possibly even if inflation does not cool below +10% Y/Y in August. These views have been reflected in a downward adjustment to local FRAs, across most of the maturity curve.

- In their weekly note, Citi Handlowy cite an NBP study which estimates the FX pain threshold of Polish exporters at 4.24 for EUR/PLN. This means that the exchange rate has not reached this barrier. In addition, Citi argue that lower costs of imported inputs may have softened the blow to local exporters. However, they believe that the NBP is not looking to support further appreciation of the zloty, even as it would not necessarily inflict significant pain on exporters.

Fig. 1: 3-Month/6-Month WIBOR vs. PLN FRA 6x9/9x12

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok