Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

OAT

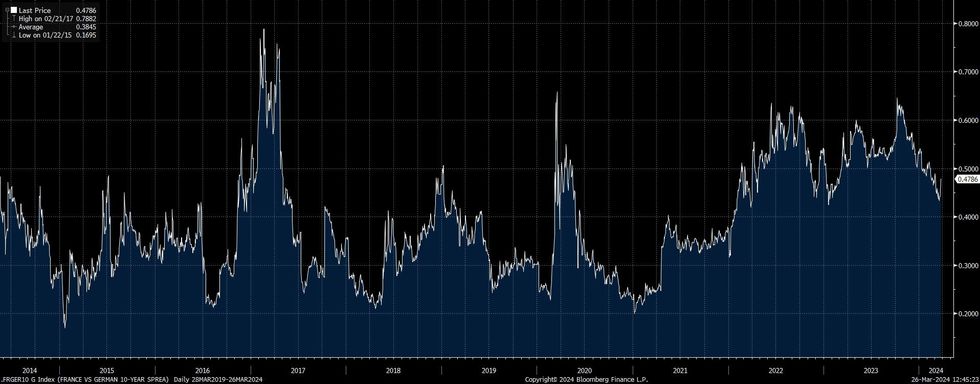

France’s ’23 deficit/GDP ratio printed at 5.5%. That was wider than the government’s 4.9% target and in line with pre-release reports/political commentary pointing to 5.4-5.6%.

- A reduction in the debt/GDP ratio also failed to meet the government’s target.

- The wider deficit was driven by softer-than-expected revenues.

- This cements upside risks to the government’s ’24 deficit/GDP target of 4.4%, making further spending cuts likely. Finance Minister Le Maire indicated as much post-release.

- The expected impact on long end issuance is seemingly limited (medium- and long-term OAT auctions have already been upsized), with Citi suggesting that the deficit overshoot will mostly be funded via bills.

- France could also lower the size of its OAT buybacks, as the country’s funding target is net of buybacks.

- France’s sovereign credit rating is scheduled to be reviewed by Fitch, Moody’s, S&P and Scope Ratings across April & May.

- S&P’s update (31 May) is likely to get the most interest as they currently have France at AA, with a negative outlook.

- Fitch has France one notch below at AA-; Outlook Stable.

- OATs had already widened vs. Bunds, DSLs and OLOs in recent days, on the back of the ‘leaks’ of the deficit/GDP ratio, limiting market reaction/widening today.

- The pre-release widening will reflect at least some risk of an S&P downgrade.

- Limited OAT issuance feedthrough and the recent OAT spread widening should limit the impact of a one-notch downgrade by S&P (assuming the outlook is changed to Stable), if it does materialise.

- Spread widening risks include S&P maintaining a negative outlook after a downgrade and/or Fitch moving their outlook to Negative, particularly given ECB balance sheet plans.

Fig. 1: France/Germany 10-Year Yield Spread (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok