Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

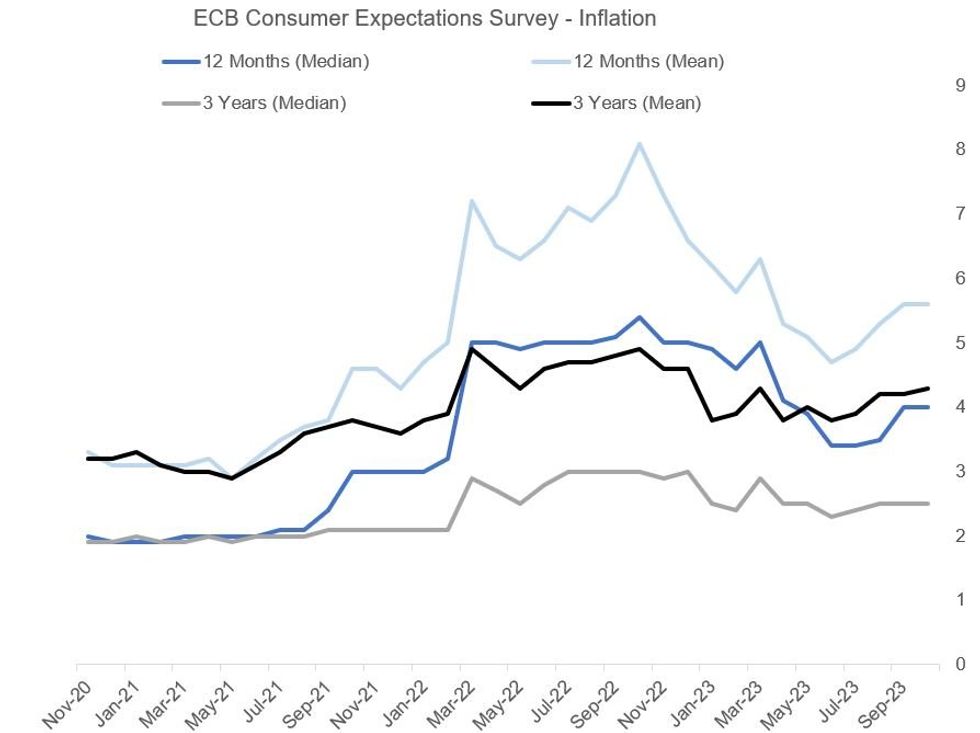

The ECB's October Consumer Expectations Survey showed fairly flat but still-elevated inflation expectations vs September's Survey, with the mean results suggesting a modest bias to the upside: median 12-months ahead was unch at 4.0%/mean 5.6%; median 3-years ahead was also unch at 2.5%/mean up 0.1pp to a 7-month high 4.3%.

- We wouldn't read deeply into the monthly survey results, but the broader context - following last month's upside surprise - is that near-term inflation expectations have stabilised and have headed slightly higher in the past few months, with the longer-term median expectations remaining at 2.5% for a third consecutive month, above the ECB's 2% target (vs in-line through early 2022).

- Between the start of the survey in April 2020 and the eve of the Russia-Ukraine war, the 3Y inflation median expectation averaged 2.0% and mean 3.5%; since then those have averaged 2.7% / 4.3% respectively.

- National divergences are visible under the surface, with German, Belgian, and Dutch median expectations dipping and between 2-2.5%, while French expectations have ticked higher and Spanish / Italian expectations around 3%. Notably the jump in Spanish inflation expectations, which we pointed out last month as having driven the overall eurozone reading higher, seems to have persisted.

- Beyond the inflation data, consumers' economic growth expectations declined, the unemployment rate expectation was unchanged, with higher expectations of both the unemployed finding a job / employed respondents expecting to lose their jobs. In parallel, nominal income and expectations ticked slightly lower, with expected nominal consumption also dipping.

- While the softer income/spending/growth outlook mean this is not a particularly worrying report for the ECB, the seemingly entrenched median long-term inflation expectations may be a lingering concern.

Source: ECB CES, MNI

Source: ECB CES, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok