Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

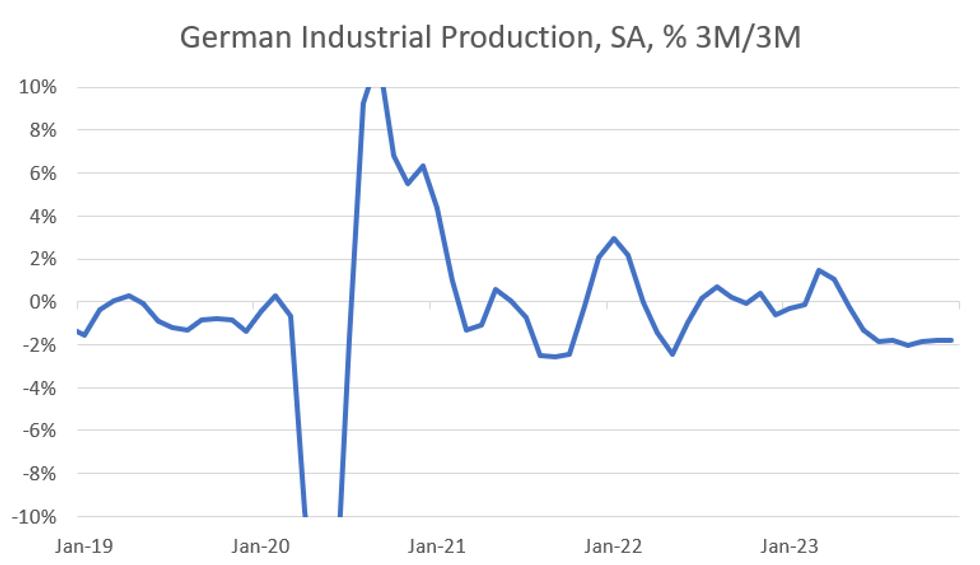

German Industrial Production missed expectations in December at -3.0% Y/Y (working day adjusted, vs -2.4% survey and -4.3% prior revised from -4.8%) and -1.6% M/M (seasonally adjusted, vs -0.5% cons and -0.2% prior, revised from -0.7%). This also marked the fourth consecutive miss against consensus for the M/M series and the seventh monthly decline in a row.

- The less volatile 3M/3M measure also paints a weak picture at -1.8% (vs -1.8% prior), the seventh month in a row below -1%.

- 2023 as a whole marked a weak year for the sector, with production decreasing -1.5% compared to 2022. Energy-intensive industries were particularly hard-hit with their production decreasing -10.2% Y/Y. Production in the chemical industry fell to the lowest level since 1995.

- Looking at individual components excluding the energy and construction industries, the declines in intermediate goods and consumption goods production accelerated to -5.2% M/M (vs -0.6% prior) and -0.9% M/M (vs -0.2% prior), respectively. On a slightly brighter note, investment goods production increased +1.3% M/M (vs -0.7% prior) after three monthly declines.

- In the construction industry, the decline seems to be intensifying but prior data got revised upwards. December production in the sector printed at -3.4% M/M (vs -0.9% prior).

- This report is consistent with other signs of industrial weakness in Germany at end-2023, with little evident momentum going into 2024. The substantial upside surprise in December factory orders growth (released Tuesday) was driven by one-off aircraft orders with the underlying core series painting a weaker picture.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok