Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

German August flash inflation came more or less in line with state-level estimates earlier in the day, with the headline CPI index printing 6.1% Y/Y (in line with MNI's 6.14% estimate made this morning).

- That's a slight deceleration from 6.2% in July, though above the 6.0% expected coming into today. The 0.3% M/M figure was the same as Jul and in line with consensus coming into today.

- Core CPI came in at 5.5% Y/Y, the same rate as July.

- Headline HICP - which feeds into the eurozone-wide inflation measure - was 6.4% Y/Y, vs 6.5% prior (and 6.3% expected), with M/M at 0.4% (slight deceleration from 0.5% prior, but high vs 0.3% expected).

- Looking at the limited breakdown from Destatis, goods price inflation ticked higher to 7.1% Y/Y, vs 7.0% prior. Note that energy prices rose 8.3% Y/Y, accelerating from 5.7% in July and 3.0% in June, but that was in large part due to base effects of a government energy relief package last year. Food prices decelerated to 9.0% vs 11.0% in July.

- As such while goods prices were higher, core goods inflation probably decelerated (though this wasn't entirely clear-cut from the state-level breakdowns which showed mixed movements in core goods items).

- Services prices continued to be boosted Y/Y by the base effect of the 9-euro transport ticket, which will drop out of the base in September - though they decelerated by 0.1pp for the 2nd consecutive month, to 5.1% Y/Y.

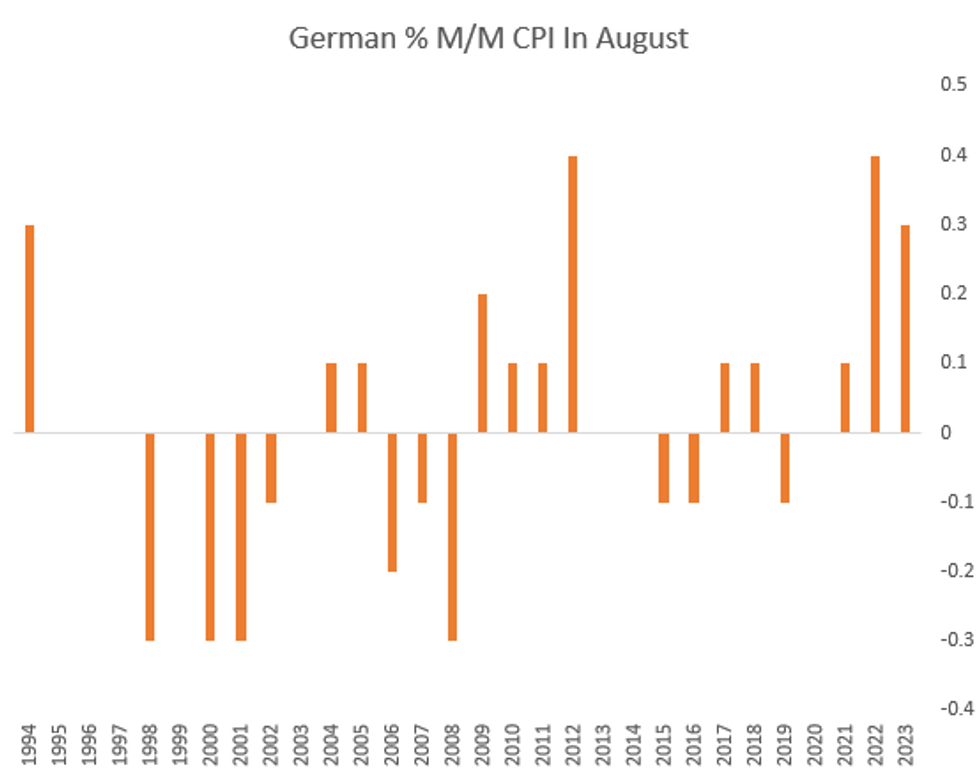

- While there is a lack of detail in the flash release (final is out Sept 8th), it shows that inflation has almost certainly peaked in Germany but has come down only slowly on a Y/Y basis. The 0.3% M/M CPI figure was just below 2022's August figure of 0.40%, and is the joint-3rd highest August print going back 30 years.

- Base effects and other statistical quirks suggest a sharp dropoff in Y/Y inflation is coming in the final months of the year, so the stubborn prints shouldn't be too worrying.

- However this is not a report that provides much ammunition for ECB doves, with little progress apparent in August prices, and any significant improvement in the inflation data having to wait until after the September meeting.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok