Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

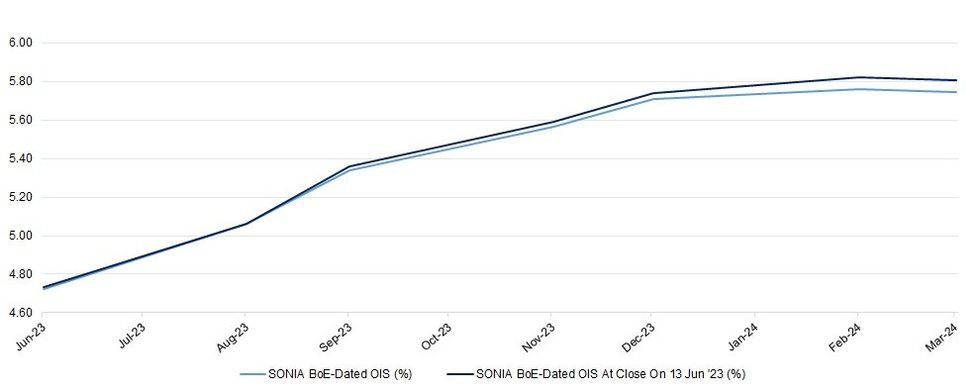

BoE-dated OIS eases a touch as core global FI markets see some light richening, although terminal rate pricing remains a little above 5.80% (6-7bp softer on the session) after yesterday’s labour market report-induced shunt higher.

- The next 3 BoE meetings still see a cumulative ~91bp of tightening priced, which equates to better than even odds of a >25bp hike in that window. Such a step would seemingly go against the general desire of the MPC as it stands, with a meaningful hurdle likely in play on that front.

- UK GDP and monthly economic production data was generally in line with exp., save soft construction readings.

- Late yesterday BoE chief economist Pill noted that “we are committed to doing everything we can to bring inflation back down to its 2% target because we recognise the huge effect it has on families and communities.”

- Plenty of questions remain re: how the UK would navigate the market-implied BoE policy rate path, in addition to still elevated levels of inflation (in at least the immediate term), general expectations surrounding fixed rate mortgage roll offs and what is expected to be another costly winter on the energy price front.

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Jun-23 | 4.721 | +29.2 |

| Aug-23 | 5.061 | +63.3 |

| Sep-23 | 5.339 | +91.1 |

| Nov-23 | 5.565 | +113.7 |

| Dec-23 | 5.708 | +128.0 |

| Feb-24 | 5.759 | +133.1 |

| Mar-24 | 5.743 | +131.5 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok