Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SINGAPORE

SGD interest rates have eased over the past week from what DBS called "overly stretched levels". 2-year SOR swaps have fallen by about 10bps to 0.44%, retracing about half of the increase since the start of February. Contributing factors include expectations of improved liquidity and some pre-positioning ahead of the MAS's biannual statement release April 14. While the MAS is not expected to tweak its policy settings, a shift towards a better outlook could portend an October move.

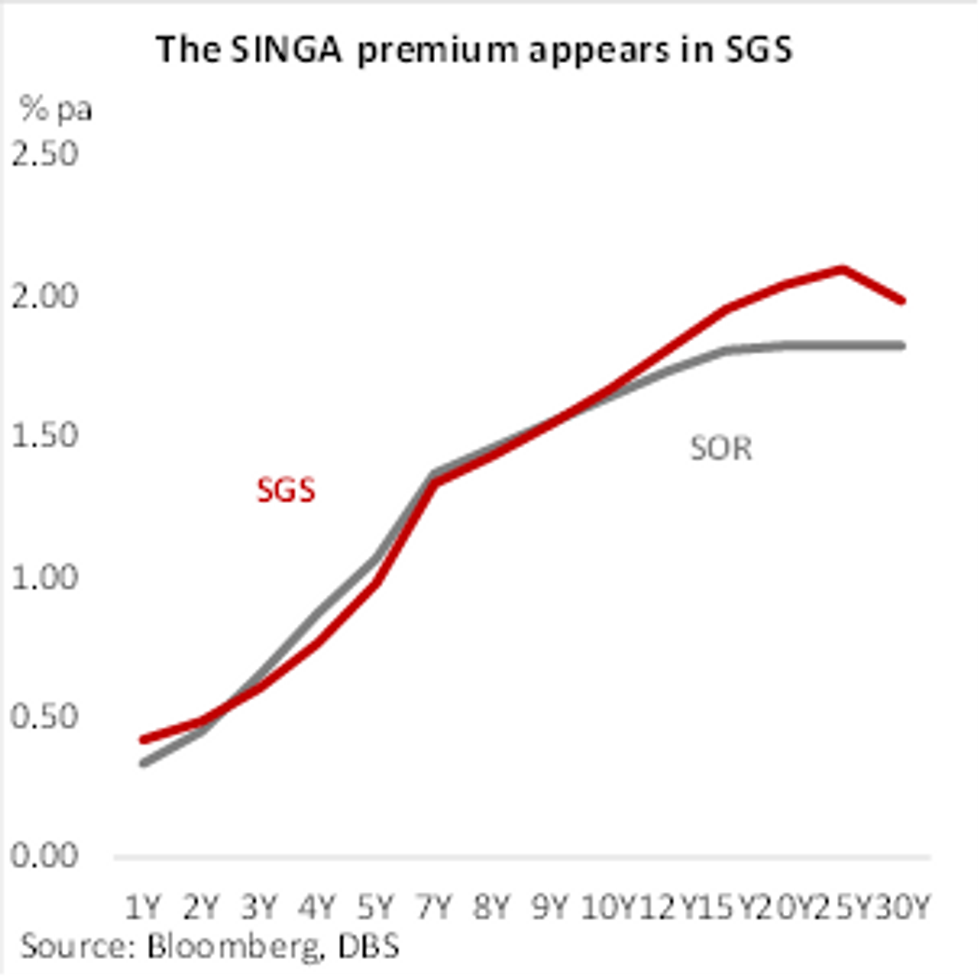

- DBS research says there is evidence of a Singapore premium that has worked its way into the longer tenor Singapore government securities. Some of this is attributed to several long tenor SGS issuances (15-year ,10-year and 20-year in April, June and August respectively). Taking the 1-year tenor as a guide, the SGS-SOR spread (defined as SGS yield less SOR) is around 8bps. However, in the longer tenors (15-year to 30-year), this premium hovers between 15-22bps, an excess of around 7-15bps. DBS says "We suspect that this premium will linger until there is greater clarity on net SGS issuances (Market Development and Infrastructure). "

- Fig.1: SGS v SOR

Source: DBS

Source: DBS

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok