Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

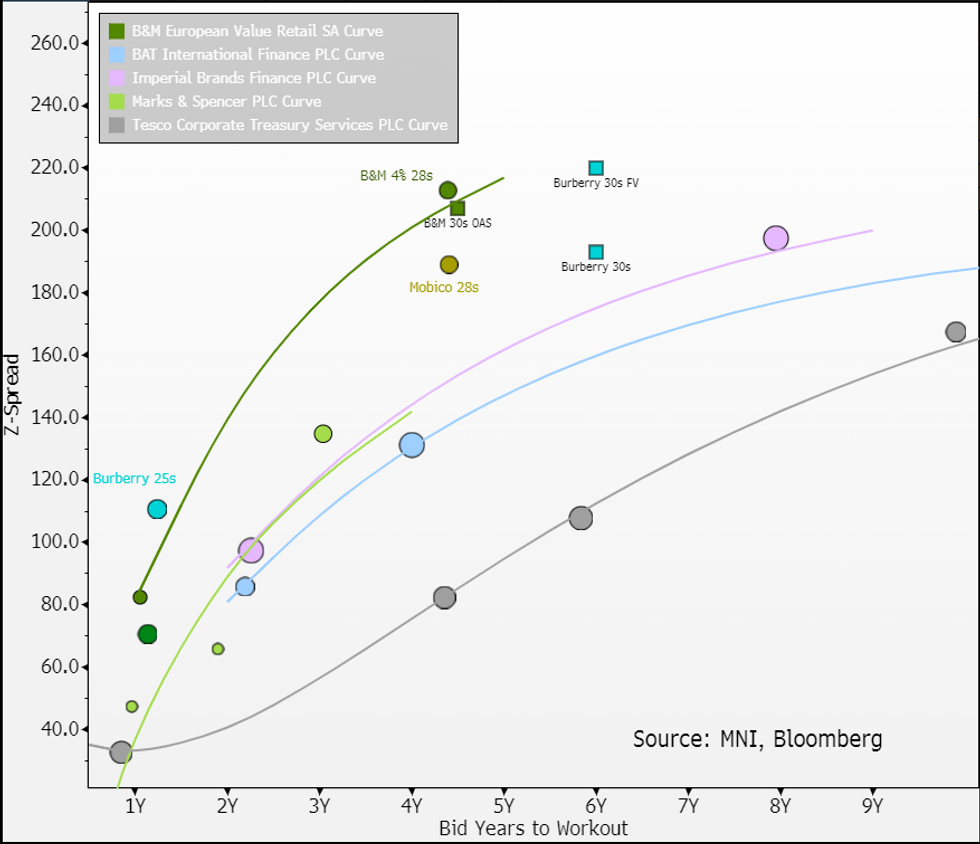

Equity moves being tied to another negative take from a analyst ahead of 1Q results on 19th of July. Reminder guidance is for 1H to stay rough (particularly in Europe wholesale). B&M 4% 28s are a cheap view at €92/6.1%/T+219/OAS+212 noting potential supply next year

- Equity sell-off has moved Debt to Equity leverage from 0.2x to 0.5x in a year. Still credit was happy to price the new 6Y -34bps through our FV.

- It's held flat there since (UKT +185) - impressive given comps have moved wider and now leaves it on the imperial curve (much safer risk in our eyes) and well inside the shorter B&M28s (Ba1/BB+).

- B&M28s screens value to us in isolation with optimistic equity analyst views, still expanding operations & protection from consumers trading down (value staple operator).

- We originally flagged the 30s as cheap but it's not ideal for those that want fixed duration - significant early call risk (8.125% coupon). It trades tad inside the 28s on OAS and currently working out to '28.

- We will blotter the 4% 28s this week into cheap views. We do see potential supply next year (see background on co linked below) but it doesn't affect our cheap view. 1Q results come 16th of July.

Background on B&M from other week here.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok