Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

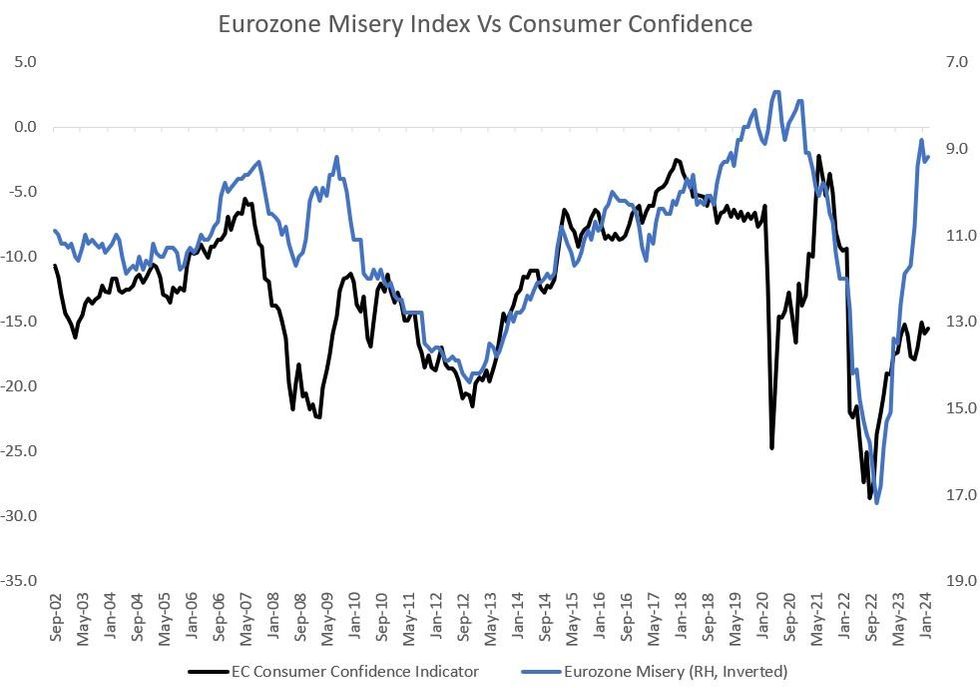

Eurozone consumer confidence picked up slightly in February in the European Commission's flash estimate, by 0.6pp to -15.5 points. That reading was exactly in line with market consensus, but as noted in the release, remains well below the long-term average.

- The release provides very limited commentary on the dynamics underlying the reading, but improvement from the Russia-Ukraine War depths of 2022 has appeared to stall over the past three months.

- Whereas the "misery index" (inflation plus unemployment rate) would normally point to above-average consumer confidence as inflation has fallen sharply from the peak and unemployment has steadied, that relationship has broken down since the Covid pandemic began in 2020. See chart below.

- The modest improvement in the consumer confidence indicator in the months to January were driven by upticks in the assessment in future financial/ economic/ employment situations - though confidence on the inflation outlook began deteriorating in summer 2023 albeit from very optimistic levels. We will get more details in the final February data on Feb 28.

- The bigger picture is that Eurozone consumption is likely to remain subdued for the next couple quarters, though a bit of an acceleration would probably be welcomed by the ECB and not a major obstacle to rate cuts. Pres Lagarde noted at the January press conference that "one of the reasons why we see growth coming up and the recovery beginning in the course of 2024; because of rising wages while inflation comes down, which will free up some purchasing power, which hopefully will stimulate consumption."

- As of the December 2023 ECB projections, real private consumption was seen ticking higher from 0.2% Q/Q in Q3 and Q4 2024, to 0.4% in Q1 2024 and levelling off at 0.5% in the next two quarters and slowing again thereafter.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok