Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NORWAY

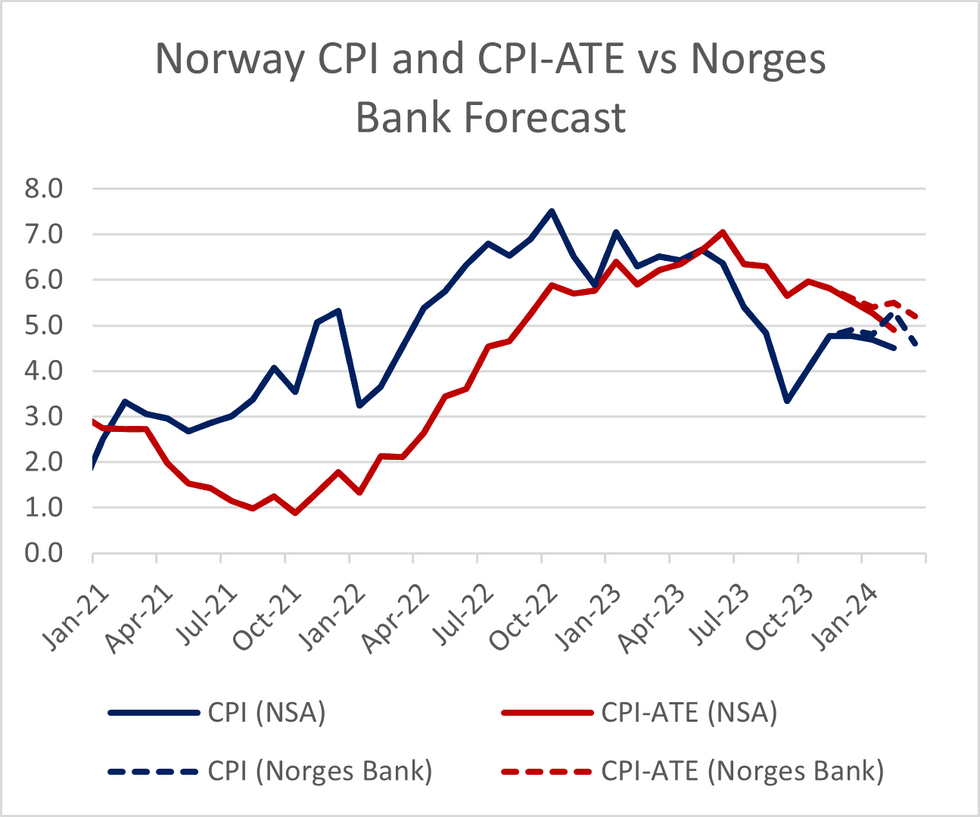

NOK saw an initial gap weaker as CPI-ATE comes in -0.4pp lower than conensus in January at 4.9% Y/Y (vs 5.3% cons and prior). The Norges Bank had forecasted 5.5% Y/Y, but this was from the December MPR which is at this point a stale forecast.

- However, EURNOK and NOKSEK are now back at pre-data levels. With core goods and services CPI-ATE still above 5% Y/Y, this won't be enough to change the Norges Bank's "higher for longer" stance ahead of the next meeting on March 21.

- Food and alcoholic beverages fell --0.6% M/M - most analyst previews we had read looked for a small NSA M/M rise around -0.4-0.6% M/M.

- This helped the annual rate on food fall to 6.3% Y/Y (vs 8.7% prior), explaning a large amount of the CPI-ATE miss.

- Despite this, core goods prices (including food) were steady at 5.1% Y/Y, likely as clothing and footwear CPI-ATE (a notably volatile category in February prints) accelerated to 6.9% Y/Y (vs 4.1% prior).

- Services ex-rent moderated to 5.0% Y/Y (vs 6.2% prior), aided by a deceleration in restuarants and hotels to 3.7% Y/Y (vs 6.3% prior) but offset somewhat by an acceleration of recreation and culture (8.5% Y/Y vs 7.2% prior).

- Headline CPI was also below consensus at 4.5% Y/Y (vs 4.7% cons, 5.3% Norges Bank and 4.7% prior).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok