Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

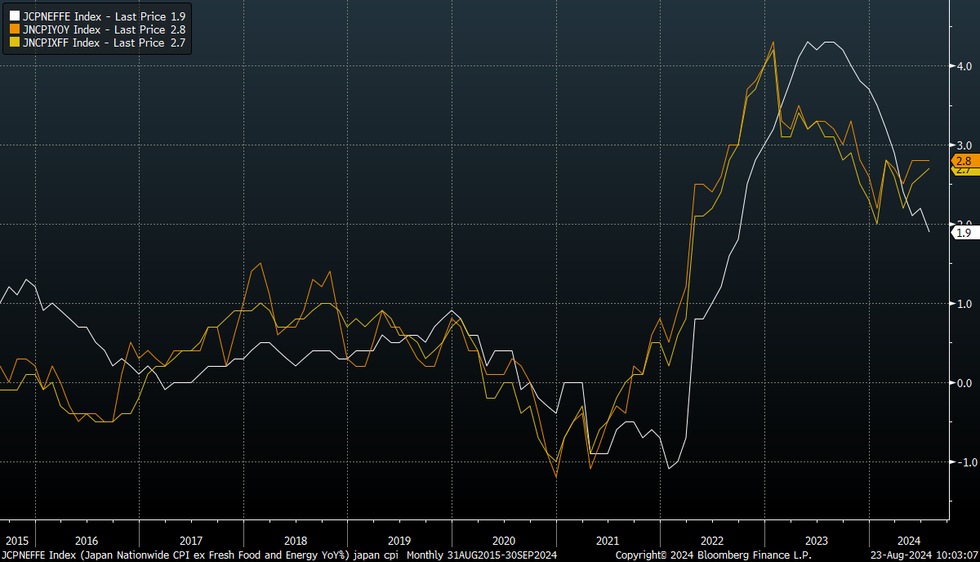

JAPAN DATA

Japan national July CPI was close to expectations. Headline rose 2.8%, against a 2.7% forecast. (June's print was 2.8%). Ex fresh food was 2.7% in line with market expectations, 2.6%y/y was the June outcome. Core, ex fresh food and energy, printed in line with market forecasts at 1.9%y/y but this was a step down from the June 2.2% pace.

- In m/m seasonally adjusted terms momentum was still reasonable. Headline CPI rose 0.2%, slightly down from June, while core ex fresh food was 0.3%, ex fresh food and energy 0.1%. Good prices rose 0.5%, while services were up 0.1%, although this is at risk of being revised away if history is a guide.

- The ex all food and energy measure rose 0.2% m/m terms (not seasonally adjusted).

- In terms of the sub-categories, fresh food (-1.8%m/m) and -1.2%m/m for clothing were the main drags. Entertainment rebound +1.0%, after falling in the previous two months. Other segments didn't display significant shifts relative to June outcomes.

- The data is unlikely to shift BoJ thinking materially. The watch point will be on core ex fresh food, energy y/y momentum being sub 2%, see the chart below (the white line).

- Base effects may bias y/y momentum lower through the remainder of Q3/early Q4. Still, the other inflation metrics remain comfortably above the BoJ's 2% target.

Fig 1: Japan National CPI Trends

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok