Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

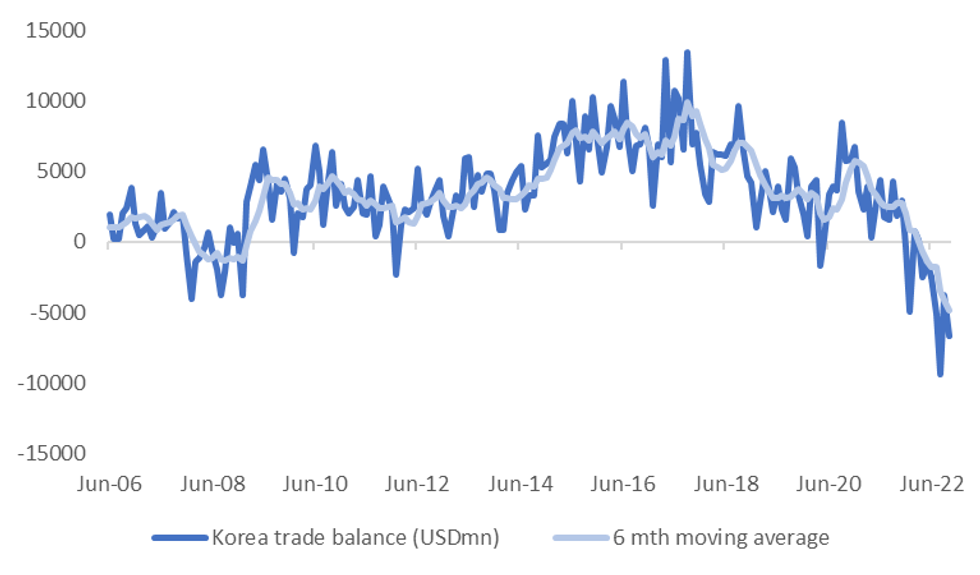

South Korean trade data disappointed on the downside. Export growth fell to -5.7% y/y, versus -2.1% expected. Import growth was firmer, +9.9% y/y, against a +6.6% expectation. This saw the trade deficit balloon back out to -$6.7bn, nearly double the consensus estimate of -$3.5bn.

- This is the weakest y/y export print since August 2020, when the global economy was emerging from the Covid induced recession. Accounting for working day effects didn't improve the picture, with this number down -7.9% y/y.

- The detail showed export growth to China down -15.7%, while chip exports fell by 17.4% y/y. Exports to the US held up better, +6.6%.

Fig 1: South Korean Export Growth - Total & To China Y/Y

Source: MNI - Market News/Bloomberg

- Energy imports surged to +42% y/y, driving the upside import surprise. This unwound some of the recent improvement in the trade deficit and comes despite the further improvement in the Citi Korean ToT proxy, which we highlighted yesterday.

- USD/KRW moved higher post the release, spot got above 1429, but we are now back to the low 1427 region, as firmer local equities (+0.90% for the Kospi) is helping sentiment.

Fig 2: South Korea Trade Deficit Improvement Proves Short-Lived

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok