Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

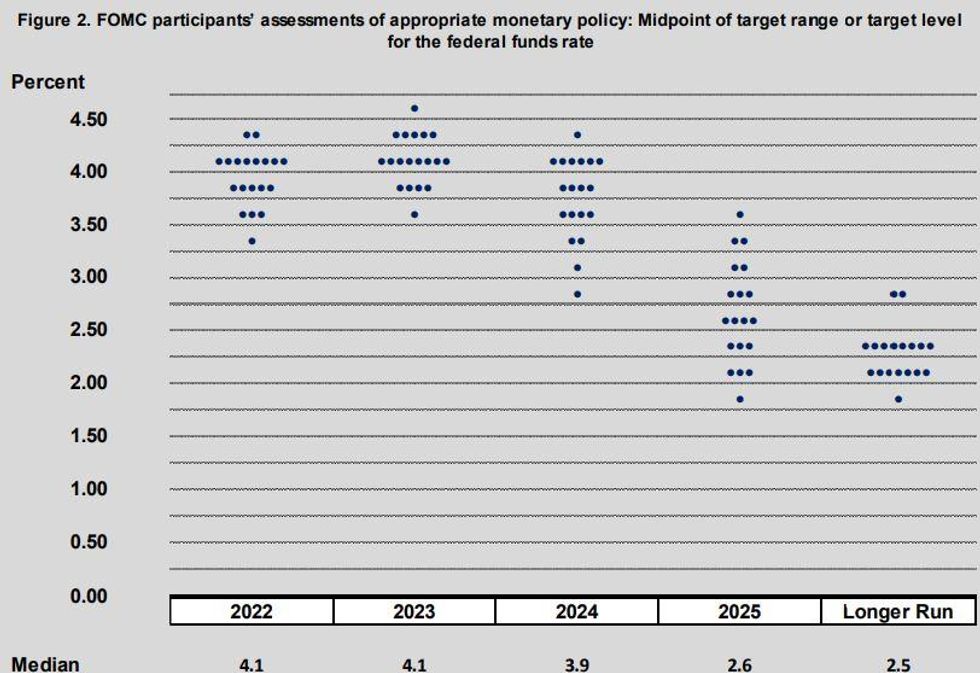

There will be two focal points to the September Dot Plot update – the end-2022 rate forecast (which will form clear expectations of what to expect at the next two meetings), and the 2023 "terminal" rate. MNI's expectations are below.

- We expect the 2022 median to be 4.1% (sell-side consensus of 3.9% / June 3.4% / market rate pricing 4.22%), with 2023 also 4.1% (sell-side split between 4.1% and 4.4% / June 3.8% / market 4.1%).

- A sub-4% 2022 dot is expected by almost half the sell-side, but we think that would be a dovish surprise given that it would mean the median participant sees under 100bp in hikes at the next two meetings.

- Most analysts expect the FOMC to eye further hikes in 2023, and the risks clearly lie toward a 4.4% median vs our 4.1%.

- But we think the median participant at this point will be minded to front-load large hikes to get well above the longer-run rate and see how things develop next year - as opposed to slow down immediately and get in a couple of 25bp increases in Feb / Mar.

- Additionally, recent messaging has been much more about Powell's "maintaining a restrictive policy stance for some time" and not "prematurely loosening". That points to lower 2023 peak, but a median at/close to 4% in 2024.

- The 2025 dots, which are new in this projection and which will be interpreted as convergence to the longer-run dot (which nobody expects to change from the 2.5% currently), will likely be largely disregarded as a strong signal.

Source: MNI

Source: MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok