Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

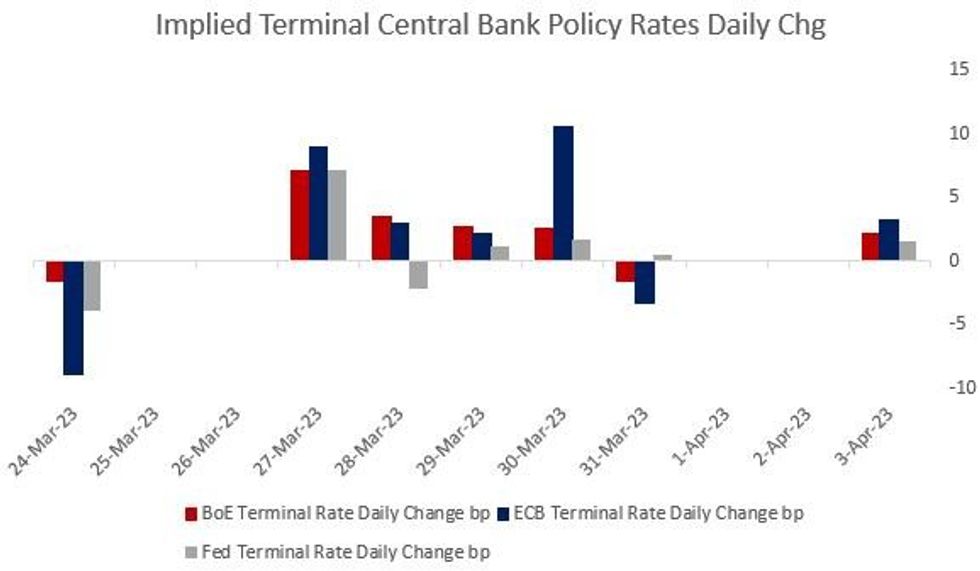

The surge in oil prices on the OPEC+ production cut has bear flattened yield curves early Monday but the bigger picture is it hasn't been hugely impactful on terminal central bank rate hike pricing on either side of the Atlantic.

- ECB/BoE peak pricing is a couple of bps off early session highs but have still gained more than Fed peak pricing this morning (which is still focused on May being the last hike, at only about 60%/40% prob of 25bp vs pause, and 55bp of cuts by year-end). We'll see if that changes as US desks come in.

- The wider terminal differential has probably helped contribute to keeping a lid on the dollar (as noted), with the broad index back to flat vs earlier gains of +0.4% on the OPEC surprise (which defied the usual inverse relationship between oil prices and USD).

- ECB terminal Depo rate pricing +4.1bp to 3.60%

- BoE terminal Bank Rate pricing +3.7bp to 4.70%

- Fed terminal Funds rate (upper limit) pricing +1.5bp to 5.16%

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok