Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NETHERLANDS

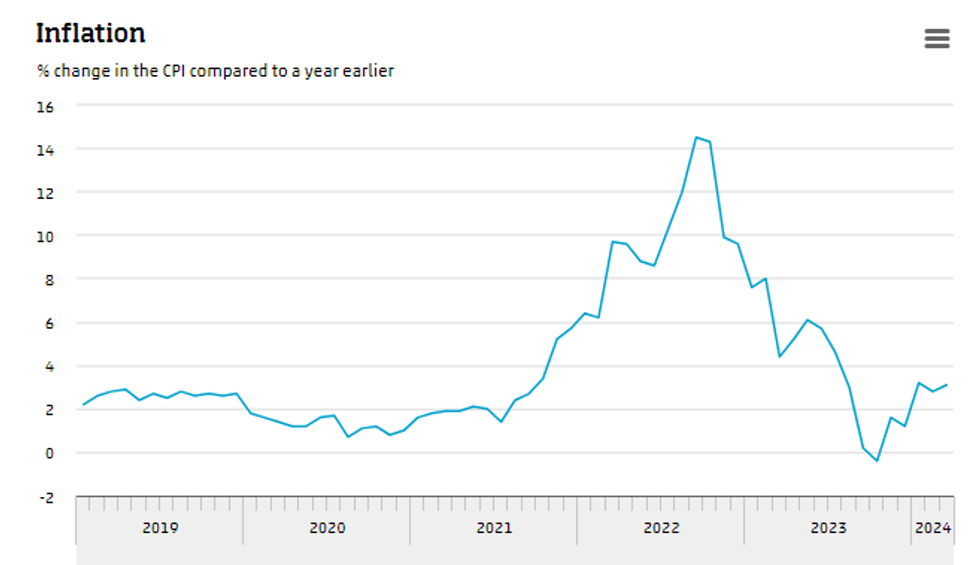

Dutch March flash inflation was 3.1% Y/Y (vs 2.7% prior) and 0.6% M/M (vs 0.9% prior). The consensus, formed of just 3 analysts, looked for a softer 2.8% Y/Y.

- Flash CPI was also 3.1% Y/Y (vs 2.8% prior).

- The increase in the headline rate was led by food (2.8% Y/Y vs 2.7% prior) and energy (3.7% Y/Y vs 1.1% prior)

- Looking at the core CPI sub-components, services accelerated to 4.6% Y/Y (vs 4.5% prior). This is a theme also seen in the German and Italian flash data, increasing the risk of Eurozone-wide services inflation hovering around 4.0% Y/Y again later today (EZ services HICP has been exactly 4.0% Y/Y in each of the previous 4 months).

- Non-energy industrial goods remained in deflation at -0.2% Y/Y (vs -0.5% prior).

- Dutch headline CPI has steadily risen from its low of -0.4% Y/Y in October 2023, as energy base effects dropped out of the annual comparison.

- Similar dynamics r.e. energy base effects will eventually be seen in the other countries and the Eurozone overall, underscoring the narrative that the path back to the 2% target may be bumpy over the coming months.

Source: CBS

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok