Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

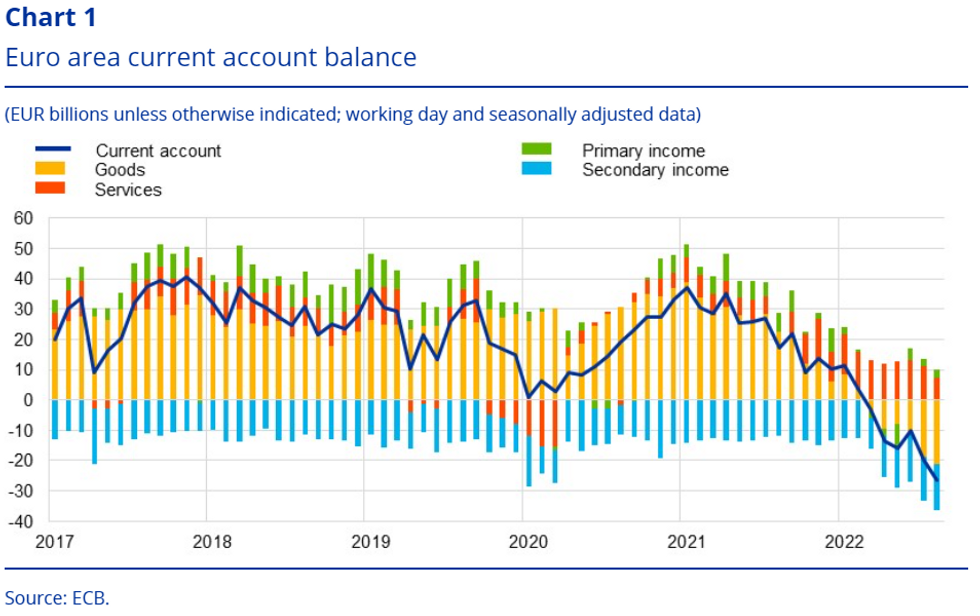

Eurozone current account dynamics deteriorated further in August, widening to E26.3bln from E20.0bln in July (slightly revised from E19.9bln), with wide deficits for goods (E21bln) and secondary income (E15bln) partly offset by services (E7bln) and primary income (E3bln) surpluses. See chart of detail.

- With soaring energy prices pressuring the goods trade balance, the E26.326bln deficit was just shy of the all-time monthly record deficit of E26.376bln in November 2009.

- The current account was in surplus between March 2012 and February 2022 before the Ukraine-Russia War.

- On a 12-month trailing basis, the euro area was in deficit by 0.1% of GDP (vs a 2.8% surplus a year earlier). That's despite an improvement in overall goods and services exports, and primary income credits, as a % of GDP - the main drag was goods imports rising from 16.9% of GDP to 21.6% of GDP.

- The flip from current account surplus to deficit amid deterioration of the eurozone's terms of trade (namely higher imported energy prices) is one of the key factors weighing on the Euro exchange rate, and there are no signs that relief is coming soon.

Source:ECB

Source:ECB

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok