Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

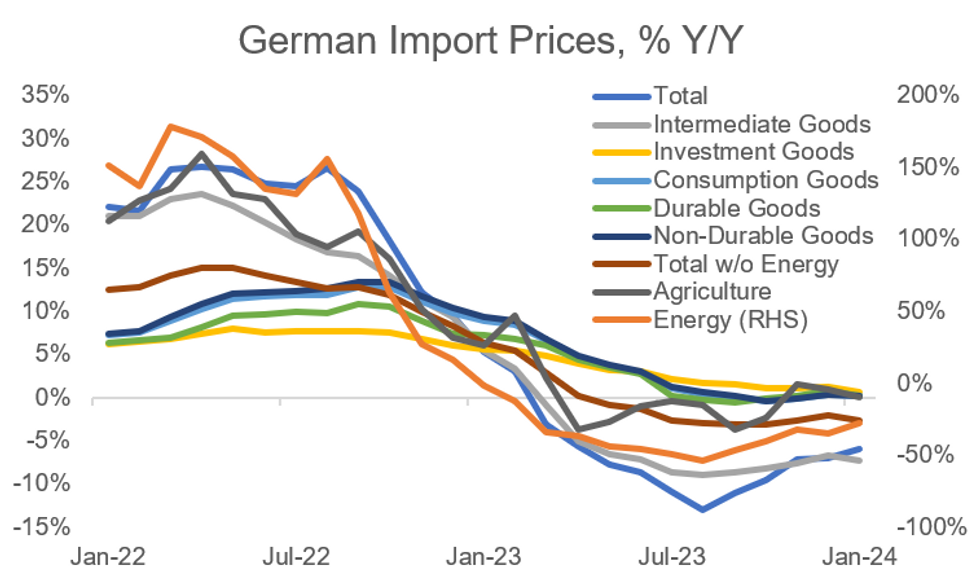

German January import prices came in above expectations at -5.9% Y/Y (vs -7.5% cons; -7.0% prior, revised from -8.5%) and 0.0% M/M (vs -0.4% cons; -1.0% prior, revised from -1.1%). On the yearly rate, this was the highest value since April 2023, and the fifth consecutive increase.

- Looking at the details of the release, energy price inflation remained the main downside driver overall but negative base effects are waning (-27.7% Y/Y vs -34.8% prior). Excluding energy, though, import prices actually decreased -2.5% Y/Y (vs -2.0% prior).

- Import prices primarily reflect goods and not services inflation dynamics, and are thus less important re ECB rate cut considerations as service inflation remains the main obstacle to potential cuts. Nonetheless, core German inflation should continue to be weighed down by subdued goods prices (NEIG prices have been relatively flat over the past 6-8 months).

- The import price data showed disinflationary trends in most categories. Intermediate goods import inflation broke a 4 month uptrend at -7.2% Y/Y (vs -6.7% prior), with the other main categories (investment goods, durables, non-durables, and agriculture) all coming in above zero but slower vs December on the yearly rate.

- Looking at the import prices' impact on economic activity, the fact that export prices decreased less quickly in the last months (-1.3% Y/Y Jan, -1.4% Dec) than import prices, should on balance be a positive positive development for German exporters. Producer prices have also continued to disinflate ex-energy in the past few months (latest data for February) - from this perspective, further goods consumer price disinflation might be in the pipeline.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok