Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SGD

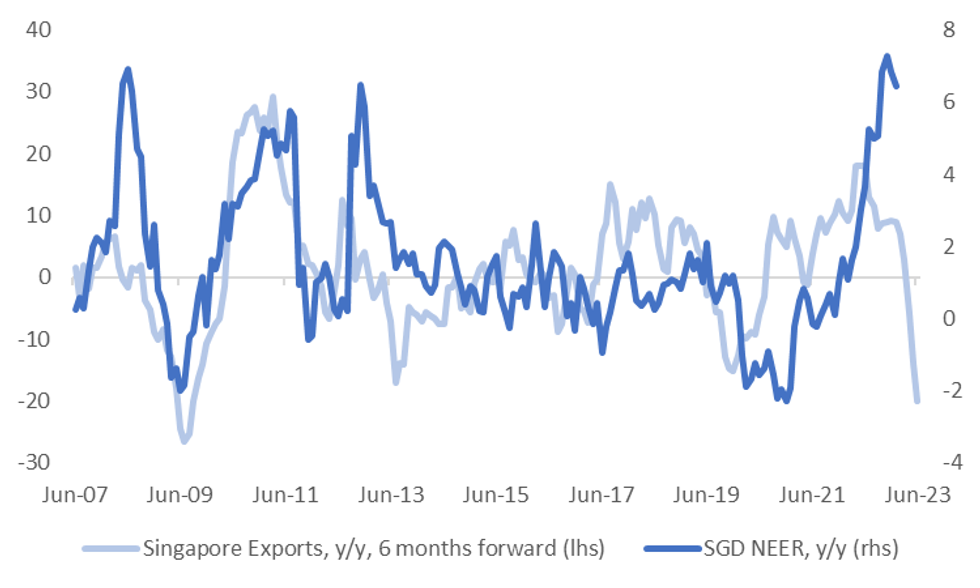

Singapore export data was a little below expectations in y/y terms (-25% y/y, -21.9% expected, prior -20.6%). Electronic exports weakened to -26.8% from -17.9% prior. The m/m data was better than expected though, +0.9%, versus -1.0% forecast, while Dec was also revised higher to -2.9% (from -3.3%).

- Base effects from 2022 is only factor driving the weaker y/y result, while a couple of sub-sectors also recovered sharp falls, which may reverse somewhat in Feb.

- Still, the picture is broadly consistent with other export orientated economies within the region (such as South Korea and Taiwan). Singapore export growth was weak in y/y terms to all major economies/regions except for the EU.

- As we have highlighted in recent months, export weakness/global growth slowdown concerns suggest the best of SGD NEER gains is behind us, see the updated chart below.

- The MAS will no doubt take this into account in April at the next policy meeting, although inflation outcomes may trump slowdown fears. Next week delivers Jan CPI figures, which are expected to show a pick up in y/y pressures.

- In terms of today's data, the SGD NEER (per Goldman Sachs estimates) remains close to recent highs, last around -0.59% below the top end of band.

- For USD/SGD the pair is ~0.1%% firmer in early dealing. Having broken through the 50-day EMA bulls can now target the January high at $1.3490. Bears target February lows at $1.3032.

Fig 1: SGD NEER & Singapore Export Growth (Y/Y)

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok