Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

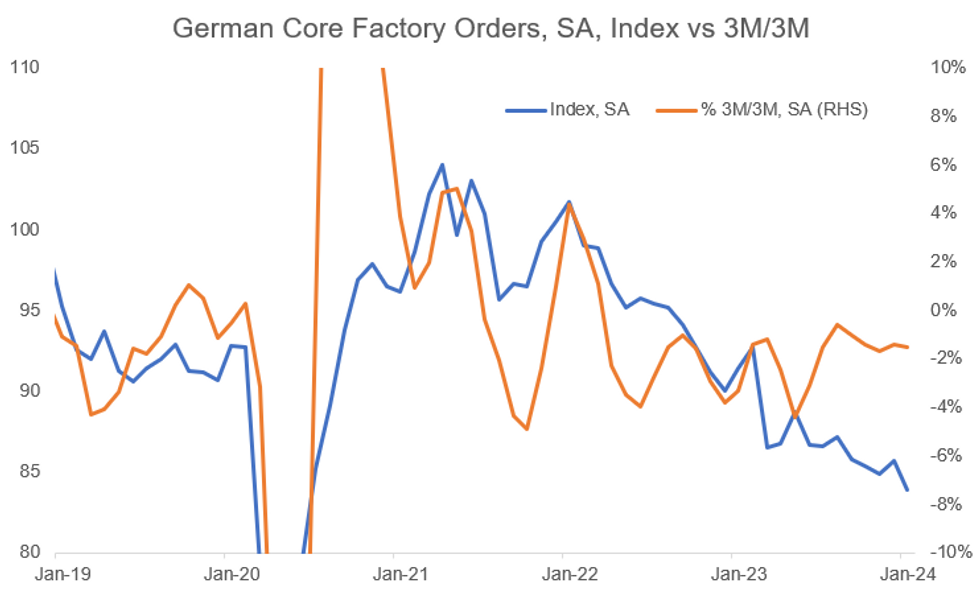

German factory orders for January fell by -6.0% Y/Y (calendar adj.; vs -6.0% cons; +6.6% prior, revised from +2.7%) and -11.3% M/M (seasonally and calendar adj.; vs -6.0% cons; +12.0% prior, revised from +8.9%). Even after accounting for the December upside revisions, which were based on late registrations of companies in several sectors of the economy, according to Destatis, the January (SA) index came in -3.0% lower than the consensus estimate would have without revisions.

- Excluding one-off big ticket items, "core" new orders declined -2.1% M/M (vs +0.9% prior, revised upwards by +3.1pp). The less volatile 3M/3M measure came in at -1.5%, in negative territory for the 22nd consecutive month, and was largely in line with the prints of the last few months (-1.4% Dec, -1.7% Nov, -1.4% Oct). The bigger picture here is that factory oders are continuing their long-standing downtrend.

- January's print also saw an update to the weighting of the individual categories (alongside a rebasing), from 2015 to 2021 values for all prints from 2021. The strongest decrease in weighting could be observed for the "manufacturing of motor vehicles and parts" category, which declined by 2.9pp to 25.4%. The decrease was made up for by incresases in weighting in a wider variety of categories, including a +0.9pp rise to 7.3% in the "computer, electronic and optical products" category and a +0.8pp rise to 19.9% in the "machinery" category.

- The motor vehicles category saw a smaller decrease than the overall headline (-5.0% M/M), suggesting that using the old weights would have seen the headline index see a smaller fall. We do not think this has a large impact on the longer term trend, however, which is clearly negative.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok