Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

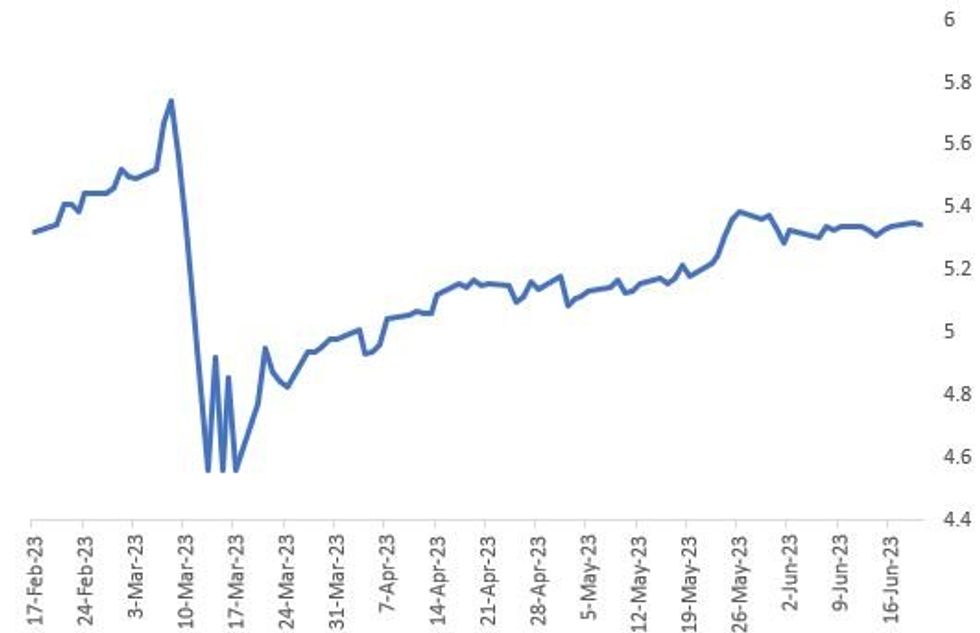

The OIS-implied Fed rate hike path is little changed vs last week's close, with Fed terminal Funds rate pricing +0.5bp, implying around 22-23bp of hikes remaining in the cycle.

- That includes 18bp at July's meeting (~70% prob of a 25bp raise, ~30% unch), and a cumulative 22-23bp through Sep/Nov to an effective rate of 5.30%- reflecting skepticism that this cycle will see another hike. End-year implied rates sit only 4bp below current and 8bp below peak, so cuts aren't forcefully on the agenda either.

- We get a few Fed speakers today (Bullard, Williams, Barr) and more housing data (starts / permits, after Monday's strong NAHB sentiment reading).

- But the main event of the week's US calendar is Fed Chair Powell's semi-annual Congressional testimony, which starts tomorrow - later today we'll preview what to expect.

Peak Implied Fed Funds Rate % (Midpoint of range)

Peak Implied Fed Funds Rate % (Midpoint of range)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok