Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR FUTURES

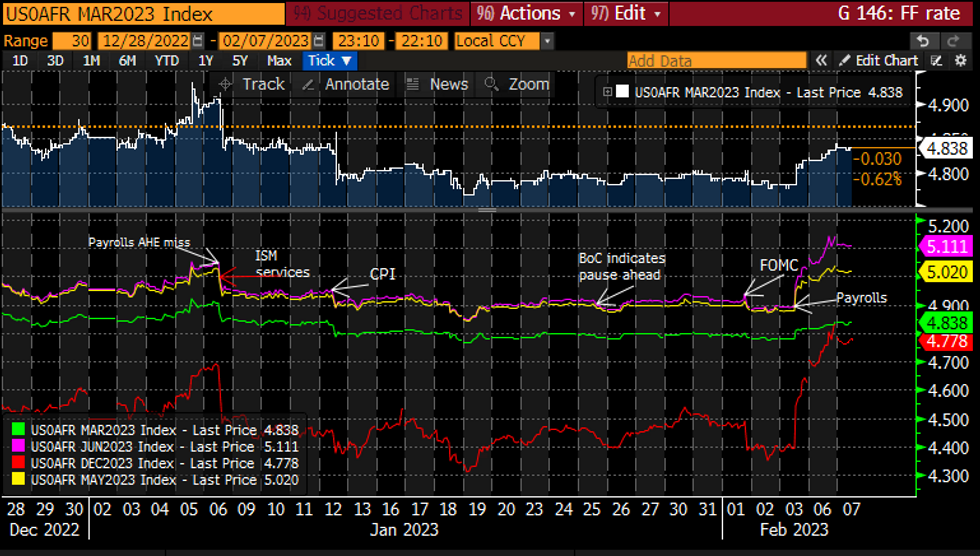

- Fed Funds implied hikes have trimmed some of yesterday’s continued climb although a largely parallel shift from the terminal onwards keeps 2H23 cuts near recent lows of 33bps (50bps pre-payrolls).

- 25.5bp for Mar (unch), cumulative 43.5bp for May (-1.5bp), 53bp to terminal 5.11% in Jun/Jul (-3/-4.5bp) before 4.78% Dec (-5bp).

- Chair Powell remarks expected to start 1240ET. Follows limited Fedspeak post-FOMC and payrolls. So far Bostic (’24) late yesterday still saw two more hikes as base case but the jobs data raised the possibility of a higher terminal, and Daly (’24) Fri saw the Dec dots as a good indicator of where headed but is prepared to do more if needed.

FOMC_dated Fed Funds futures implied ratesSource: Bloomberg

FOMC_dated Fed Funds futures implied ratesSource: Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok