Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

While talk of fragmentation focuses largely on the euro area bond market, we take a wider perspective and consider broader economic forces that can signal intensifying stress within the euro area.

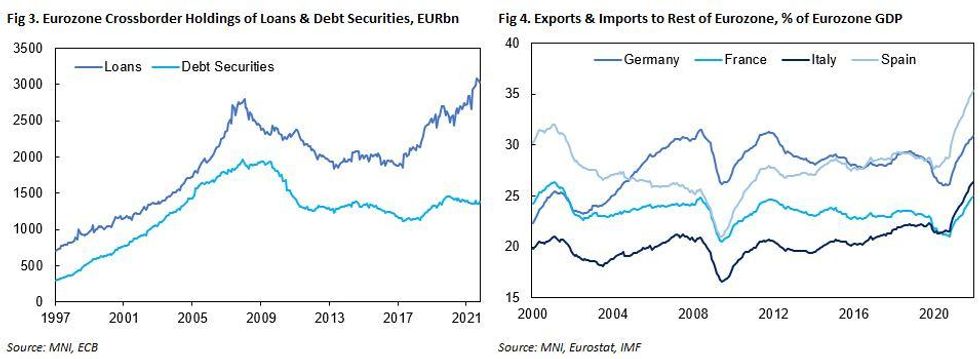

- In Fig 3 we show the total cross-border holdings of loans and debt securities in the eurozone. During the sovereign debt crisis cross-border holdings noticeably fell, raising the risk of a de facto financial balkanisation of the euro area. During this period, concerns among creditors and national regulators about exposures to foreign banks and government debt underpinned a shift towards asset onshoring inside national borders. However, the situation today is again markedly different from that era with cross-border lending surpassing pre-crisis peaks, while holdings of debt securities have stabilised.

- In Fig 4 we combine measures of trade openness (exports + imports as a % of GDP) with trade exposure (% trade concentration) by looking at the total exports and imports of four largest eurozone countries with the rest of the euro area, relative to GDP. During the debt crisis there was some evidence of regional trade deteriorating - particularly in Germany and France where total trade with the euro area fell relative to GDP - which likely reflected the weaker demand during the austerity years. Again, the situation today is markedly different with trade integration within the euro area appearing to deepen coming out of the pandemic, further suggesting that economic and financial fragmentation risks have materially fallen.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok