Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

TRANSPORTATION

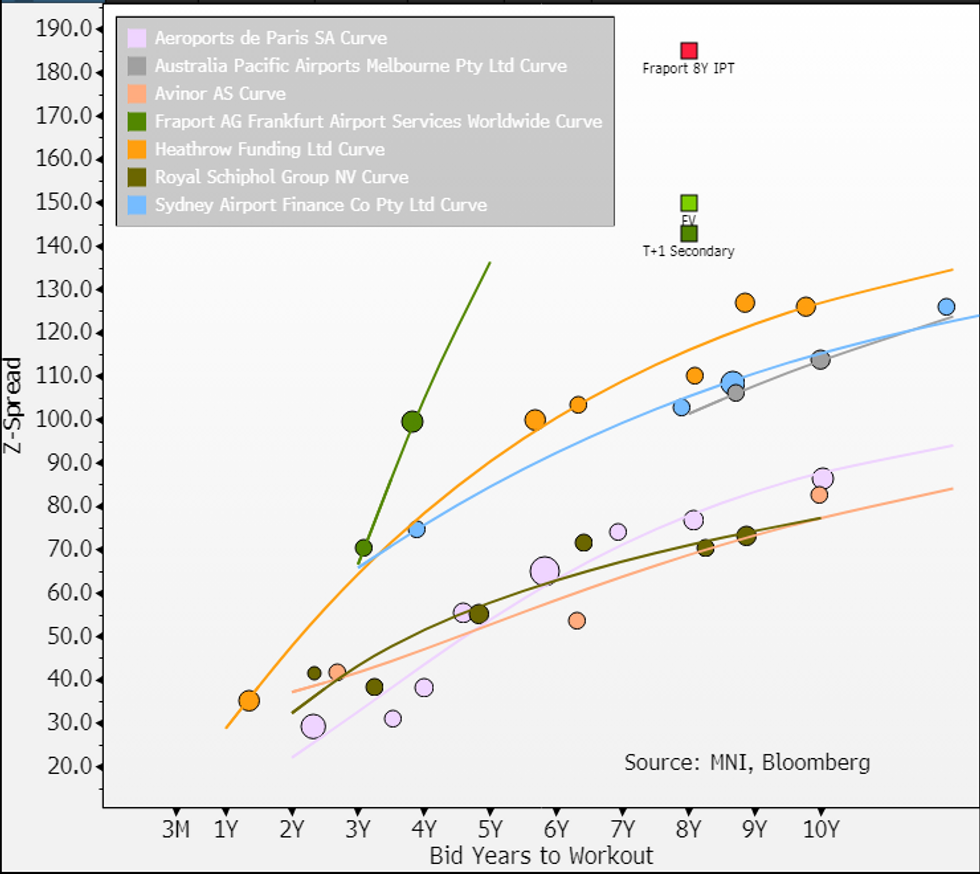

Perhaps the golden child for unrated issuers; tightened 30 in from IPT, gave no NIC, upsized books, still had 2.5x cover & moved -12 in secondary.

- 1k denoms might have helped bring in retail demand but the existing 28s & 27s are the same & our FV was based on their trading history. Its now spread +45bps to 28s for 4.2yr term extension - PVH, a IG retailer, gives the same for 1.5yrs.

- Its hard to pinpoint where this would have been rated but a publicly traded equity (vs. most airports private), regular quarterly reports & ~50% government ownership might be doing some work to offset the NR discount.

- Not a curve that shows any value to us; BS is gross 9.8x levered with guidance for net leverage at 6.4x to stay unch this year. Adding to that no positive FCF in sight on heavy capex for terminal development at Frankfurt & Lima (Capital of Peru).

- 2Q earnings come early August.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok