Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

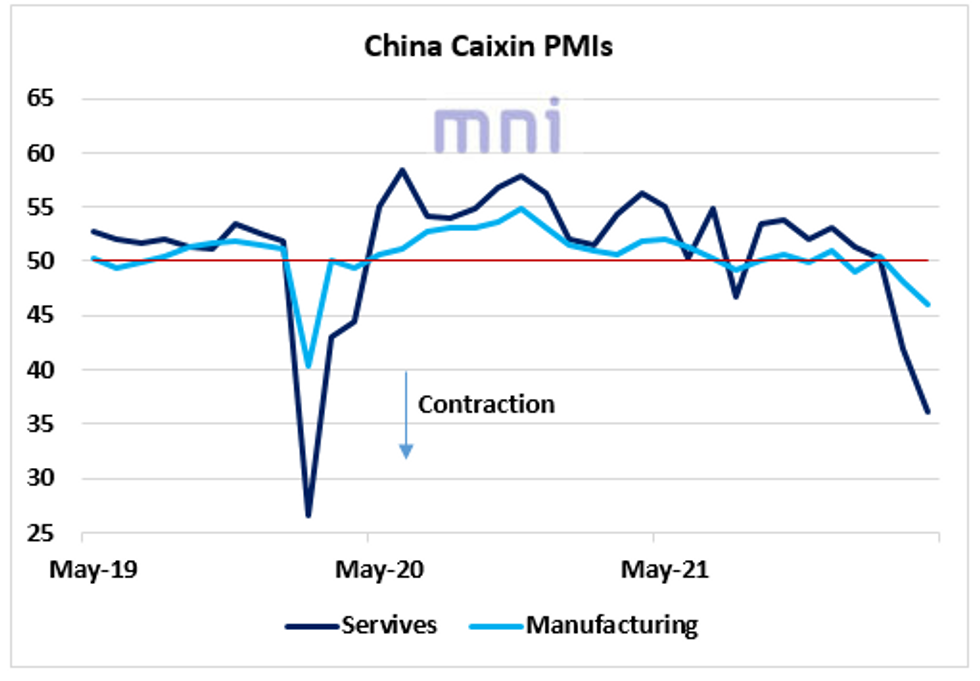

- Fundamentals continue to deteriorate in China, with China Caixin PMI services plunging to 36.2 overnight (significantly below expectations of 40), its lowest level since February 2020, down from 42 the previous month.

- This follows the downtick in manufacturing PMI last week, which fell to 46 (vs. 47 exp), raising investors’ concerns over China’s GDP growth target of 5%-5.5%.

- The economic costs of the strict lockdown policies imposed by the government in recent weeks have been surging, forcing Chinese officials to send more easing signals to stimulate both the real economic activity and domestic risky assets.

- A number of sell-side firms have been revising their 2022 growth forecasts significantly lower. For instance, Fitch recently cut its growth forecast to 4.3% YoY, down from 4.8% previously.

- We have seen lately that China officials have been introducing a series of measures to rebuild confidence on the equity market: crackdown on ‘malicious short sellers’, cutting A-share stock transaction fee, pausing on the campaign against tech companies.

- However, China equities remain fragile in the short term; Hang Seng index is still down over 30% from its high reached in February 2021, which also corresponds to the peak in the Chinese economic activity.

- HSI index has been testing its 21,287.60 resistance in the past week, which corresponds to the 23.6% Fibo retracement of the 18,235.50 – 31,168.30 range.

- In addition, the bearish sentiment in US equities in recent months and the global risk off environment are also not helping China risky assets at the moment.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok