Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

October and November's positive monthly GDP prints suggest upside risks to the Riksbank -0.4% Q/Q forecast for Q4 '23, though analysts have noted that the monthly indicator is not generally a good predictor of the quarterly figure.

- The November GDP indicator came in above consensus at +0.2% M/M SA (vs -0.6% M/M cons, +1.0% prior). Weak imports of goods were highlighted as a driver for the indicator remaining above zero.

- Overall, this doesn’t change much for the Riksbank policy outlook. The growth outlook is known to be weak and the bar for additional rate hikes is extremely high. Only a much higher-than-expected CPI print next Monday would call into questions analysts' calls for no further tightening in Sweden.

- The positive GDP print comes in spite of overall business production falling -0.3% M/M SA and -1.2% Y/Y, and consumption data showing continued signs of weakness.

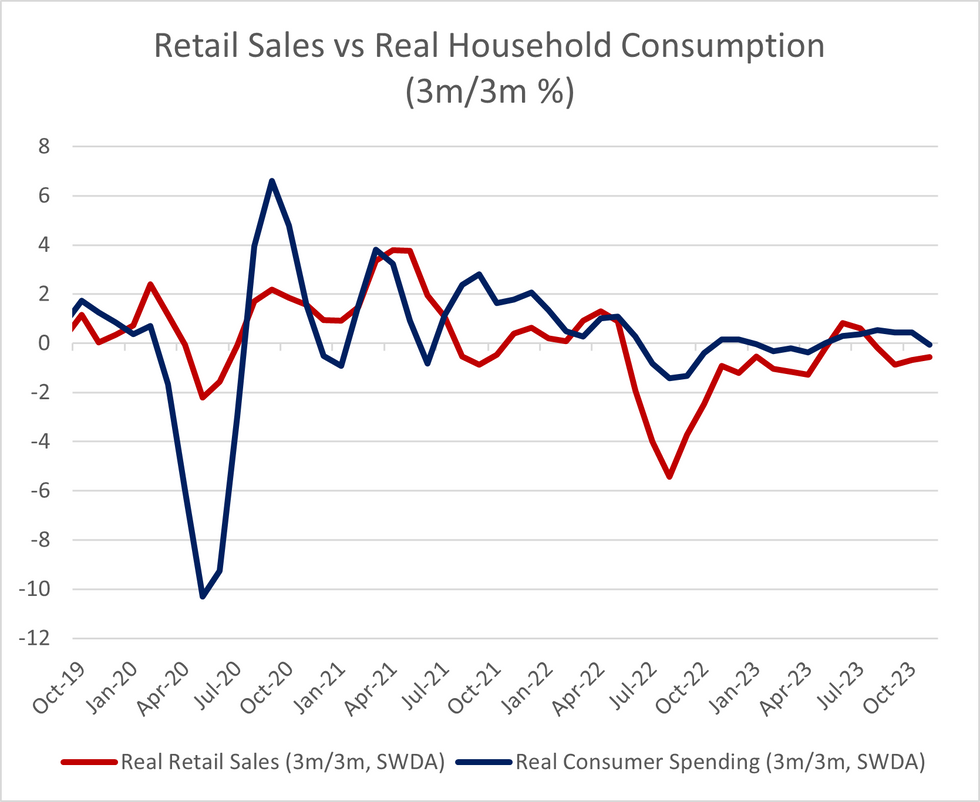

- Retail sales, released alongside the monthly GDP data, fell -0.5% M/M SA (vs an upwardly revised +1.7% prior) and -1.7% Y/Y (vs an upwardly revised -0.4% prior), with consumable goods printing weaker than durable goods counterparts. Household consumption fell -0.5% M/M SA (vs an upwardly revised +0.5% prior) and rose +0.1% Y/Y (vs an upwardly revised 0.7% prior). The largest negative contribution to household consumption came from recreation and culture, which fell -3.4% Y/Y, while housing, electricity, gas and heating was the largest upside contributor.

- The monthly indicators are volatile series, but the 3m/3m retail sales have been negative for the past four months, printing at -0.6% 3m/3m in November (vs -0.7% prior). Trends in household consumption have not been as negative, hovering either side of zero growth, but the weak picture remains clear.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok