Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NORWAY

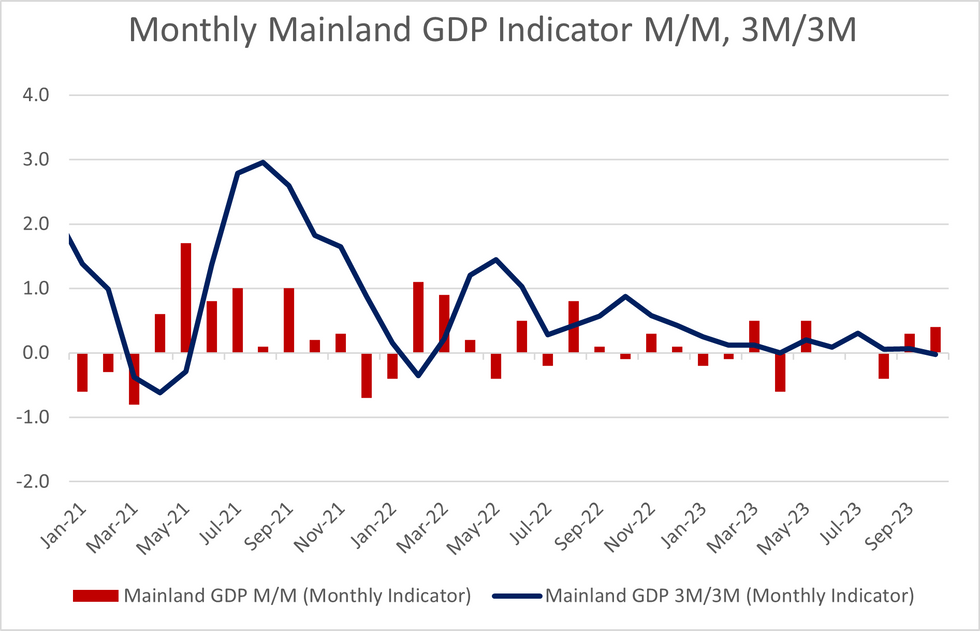

The Norwegian monthly mainland GDP indicator was firmer than expected in October, printing at +0.4% M/M (vs +0.0% cons; +0.3% prior). This is also above the Norges Bank's September projections of +0.1% M/M. However, on a rolling 3M/3M basis growth was flat in the August-October window vs. May-July, continuing to point to a subdued underlying economic growth environment.

- While a positive development, the volatility of the monthly indicator should mean today's print has a limited effect on the Norges Bank's decision on Thursday - where a hold in rates is expected. A reminder that the run of data seen since the previous Norges Bank meeting has tilted perceptions towards no further in tightening in monetary policy, despite the Bank guiding for a hike at this week’s meeting last time out.

- The overall GDP indicator was +2.1% M/M (vs a revised -2.2% prior).

- EUR/NOK fell 0.10% following the release and remains just below pre-data levels, given the modest positive impulses from the headline figures.

- On a 3M basis, the press release notes that electricity has had the largest positive impact on growth while agriculture and wholesale trade, alongside retail, have had the largest negative impact.

- Household consumption rose 0.9% M/M in October (in fixed prices), largely driven by electricity usage. As a result, goods growth was +2.3% M/M while services was just +0.3% M/M.

- Within the remaining components, gross fixed capital formation fell -3.2% M/M, exports rose +3.8% M/M and imports fell -2.7% M/M.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok