Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

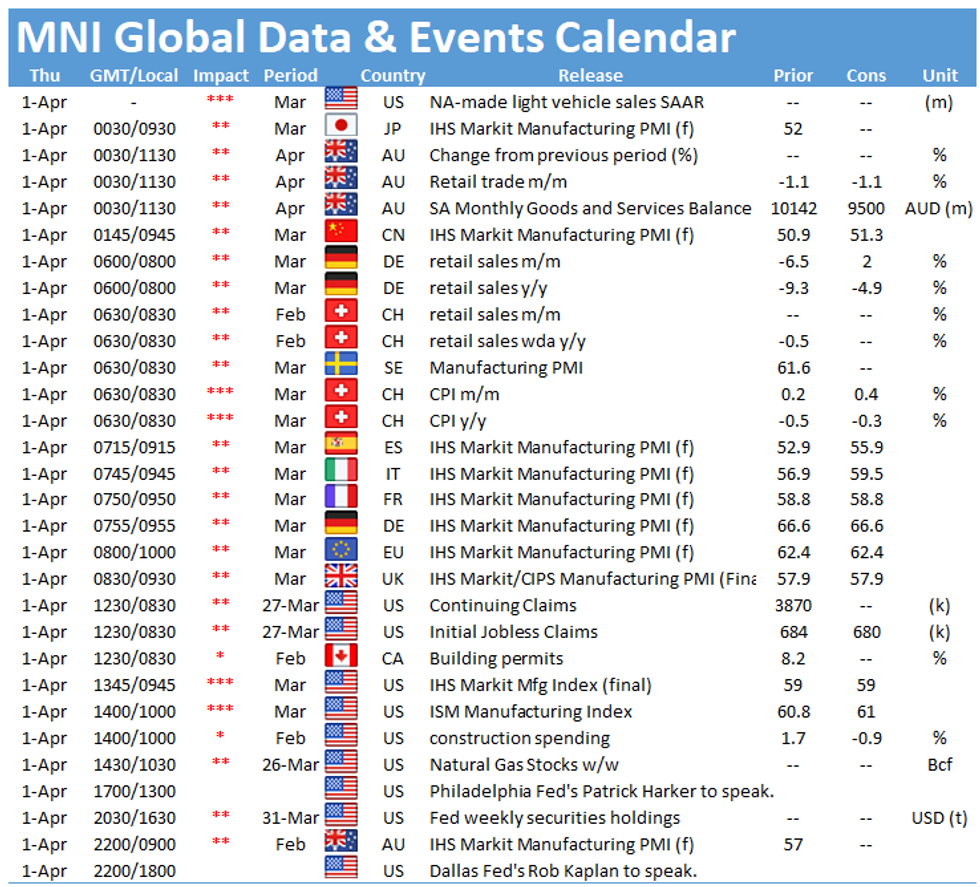

The main data events Thursday include German retail sales at 0700BST, followed by the final manufacturing PMIs for Spain (0815BST), Italy (0845BST), France (0850BST), Germany (0855BST), the EZ (0900BST) and the UK (0930BST). In the US the ISM Manufacturing PMI will closely watched at 1500BST.

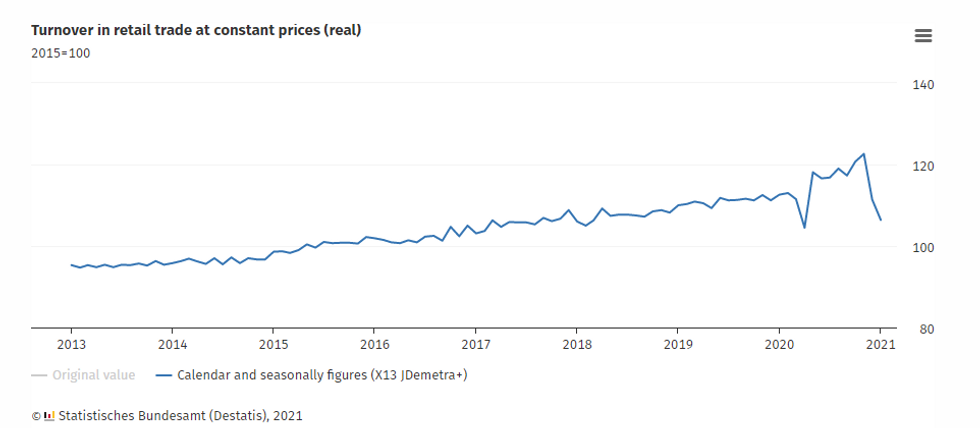

German retail sales expected to rebound

German retail sales are forecast to recover in February to 2.0%, after falling by 4.5% in January. Retail sales fell again in January as the hard lockdown led to the closure of many businesses and weighs on consumer spending. Annual sales were 8.7% lower than a year ago and 5.8% lower than in February 2020 before the pandemic. Looking ahead, sales are likely to rise further in March as several shops including garden centres and book shops could reopen in March in several states. Moreover, consumer sentiment improved as well in March and April, which bodes well with an increase in retail sales.

Europe's Manufacturing PMIs signal expansion

The final manufacturing PMIs are expected to register in line with their flash estimates showing strong readings for France, Germany, the EZ and the UK. All four flash results showed monthly gains in March with Germany and the EZ indices hitting record highs at 66.6 and 62.4, respectively. Meanwhile, the French manufacturing PMI edged up to 58.8, while the UK's index rose to 57.9 according to the flash results. The EZ flash report noted that a pickup in global demand boosted business activity in the euro area. On the other hand, the UK flash report suggested that export orders remained subdued in March. All flash releases reported longer delivery times and shortages of supplies which leads to higher factory gate prices.

The Italian and the Spanish PMI, for which no flash estimates are available, are expected to rise further in March and remain comfortably above the 50-mark, signalling expansion. While the Spanish index is forecast to rise to 56.0, up from 52.9 seen in February, the Italian manufacturing PMI is projected to tick up 2.9pt to 59.8 in March.

ISM manufacturing PMI seen higher in March

The ISM manufacturing PMI rose to a 36-month high of 60.8 in February after falling to 58.7 in January. The index now remains in expansion territory for nine consecutive months. In March, markets are looking for another increase to 61.5, which would be the highest level since December 1983. Prices paid are expected to decline to 82.0 in March after surging to the highest level since July 2008 in the previous month. Similar survey evidence is in line with market forecasts. The Chicago Business Barometer increased in March as did the Kansas City Fed manufacturing PMI and the Richmond manufacturing index. Several surveys indicated that the current supply chain disruption such as delivery delays and raw material shortages drive up prices.

The events calendar throws up a quiet schedule on Thursday with the only events worth noting being speeches by Philadelphia Fed's Patrick Harker and Dallas Fed's Rob Kaplan.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.