Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

The magnitude of the October jump in hotel prices (vs -0.8% M/M average the prior 6 months, with no reading above 2%) suggests it could be a one off.

- But this is part of the overarching story of goods demand moving into services demand: with vacations/travel picking up, and hotel occupancy levels well above 2021 levels (and back to 2019 levels), it doesn't look like a category that will contribute to broader disinflation going forward as it has for much of the past half-year.

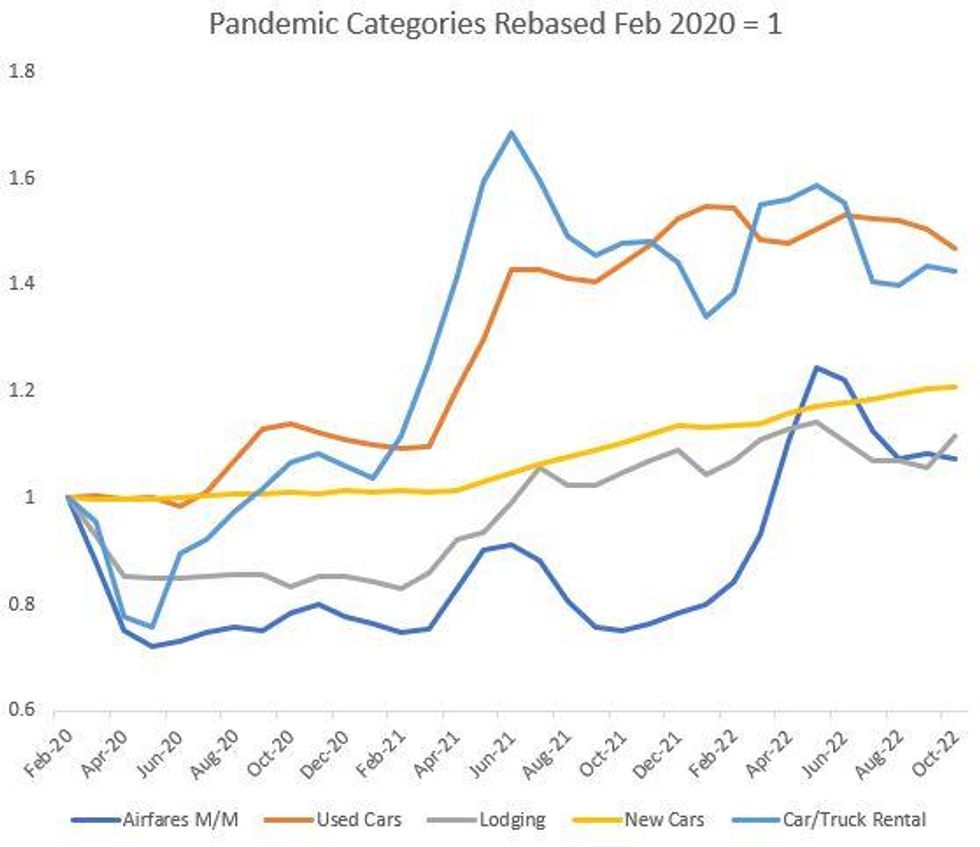

- Hotel price inflation never really hit the heights of the other pandemic reopening categories: while they picked up significantly in 2H 2021, that was from depressed pandemic levels.

- Hotel prices are now up 12% from Feb 2020, having peaked at 14% above.

- Used cars and auto rental are still 40% above pre-pandemic levels, and like airfares, lodging prices took longer to recover.

Source: BLS, MNI

Source: BLS, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok