Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

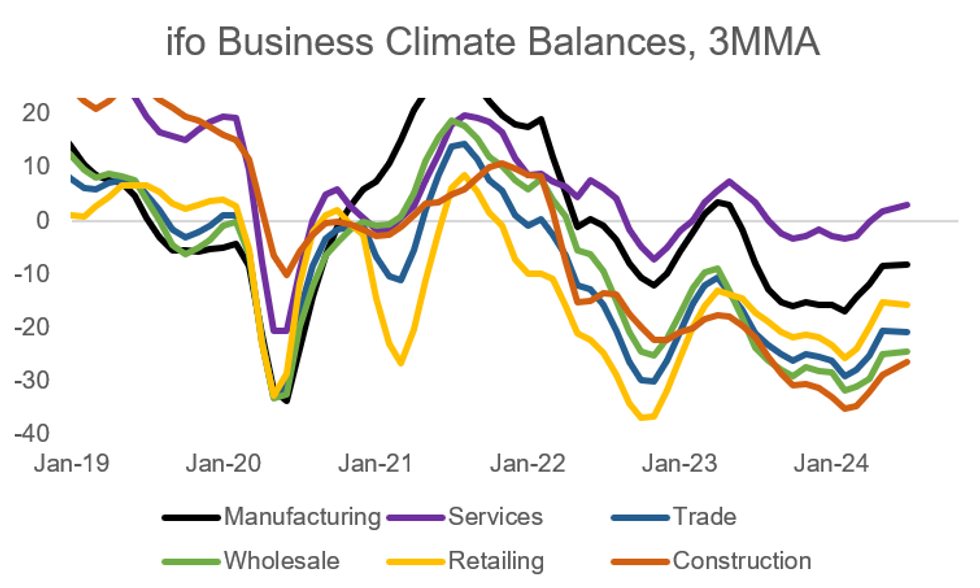

Germany's IFO Business Climate Index fell for the second consecutive time, to 88.6, remaining in contractionary territory in June and below the consensus of 89.6 and May print of 89.3. Although the headline has broadly moved in line with the June flash PMIs, there are different drivers, with the downtick in the IFO release driven by the manufacturing and trade sectors. Overall the IFO release points towards a potential stalling of the recent gradual recovery.

- The current assessment remained constant (88.3 vs 88.5 cons; 88.3 prior), while expectations worsened (89.0 vs 90.7 cons; 90.3 prior, revised from 90.4).

- The overall trade sectoral balance declined to -23.5 (vs -17.0 in May) - there were no specific drivers of this noted in the press release, and the survey period is not known publicly, but we note that the deterioration comes after EU tariff announcements of Chinese EVs, which fostered some cautious comments from auto industry representatives (some EU-China negotiations now have started on this, however).

- The manufacturing sector also saw sentiment deteriorate in June, with its respective balance declining to -9.2 after three consecutive upticks (-6.5 May). The decrease was only driven by expectations (-12.3 vs -6.1 May). The industry would also be highly exposed to an intensification of trade tensions with China.

- In contrast, services sector sentiment moved back in line with its medium-term uptrend after stalling last month (4.2 vs 1.8 in May, highest value since May 2023). Both the current assessment and expectations improved.

- The construction sector saw sentiment continue to improve (a trend in place since February), the sector remained in contractionary territory, and the speed of the uptrend slowed (-25.0 vs -25.6 in May).

- The less volatile 3MMA measure broadly mirrored the idiosyncratic developments from June.

MNI, IFO

MNI, IFO

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok