Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

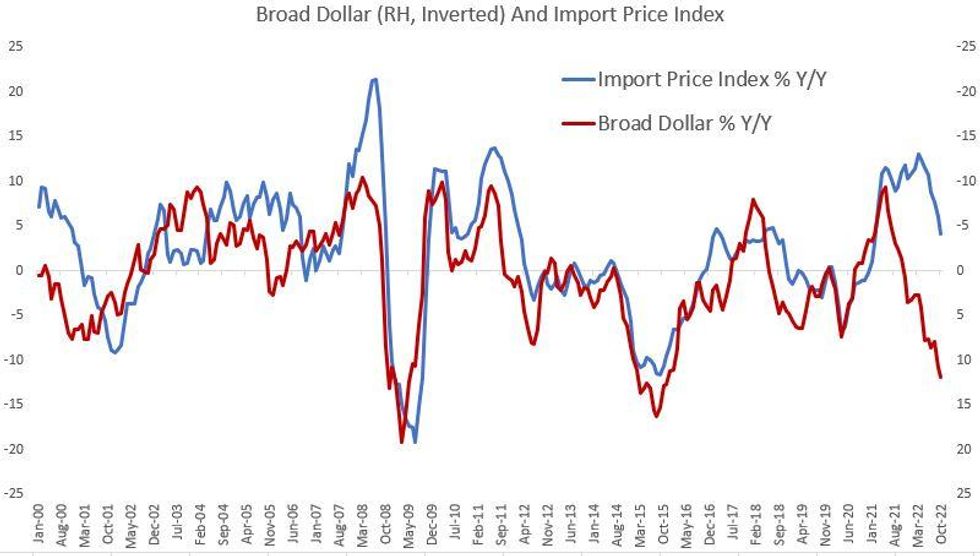

Double-digit Y/Y % gains in the US broad trade-weighted dollar index have typically been consistent with similar sized falls in the import price index. With today's release of above-expected October import price figures (+4.2% Y/Y, vs 4.1% survey), it's worth noting that relationship has broken down over the past year or so,

- The broad dollar has been positive Y/Y since November 2021, but import prices have continued to rise at a 10+% clip for most of the period since and are only starting to cool.

- Two possible explanations for this divergence: one is that petroleum import prices have remained stubbornly high even as the USD has strengthened, which is unusual vs previous periods and attributable to the Russia-Ukraine war fallout.

- But ex-petroleum import prices are also staying stubbornly high - this could be the result of supply chain issues keeping global prices elevated with dollar strength not enough to offset.

- It's likely that import prices will "catch down" to some extent with dollar strength and they are already moving in that direction, but the headwinds for inflation from a stronger USD aren't as strong as they have been in the past.

Source: BLS, Federal Reserve, MNI

Source: BLS, Federal Reserve, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok