Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

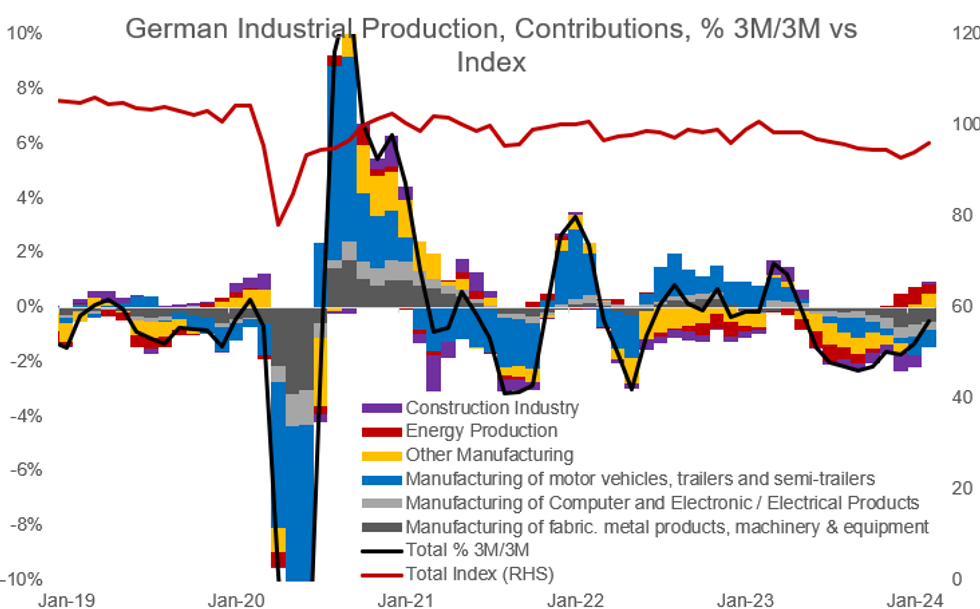

German industrial production exceeded expectations in February with a second consecutive monthly uptick of 2.1% M/M (highest since January 2023; vs +0.5% cons/+1.3% prior revised from +1.0%) but is still clearly in negative territory on a yearly comparison at -4.9% Y/Y (vs -6.8% cons/-5.3% prior revised from -5.5%).

- Overall this is a strong report, especially when considering the upward revision of last month, and was driven by strong developments in the construction and automotive industries. The less volatile 3M/3M measure also improved to -0.5% (vs -1.4% prior), which while still negative was the highest value since May 2023.

- Looking at individual components of production ex-energy and construction, the uptick was broad-based, with intermediate goods +2.5% M/M (vs +4.3% prior), investment goods +1.5% M/M (vs -1.5% prior), durable goods +3.0% M/M (vs +1.1% prior), non-durable goods +1.6% M/M (vs +4.0% prior) and consumption goods +1.9% (vs +3.4% prior).

- A split across industries shows strength especially in construction with its highest monthly increase since March 2021 (+7.9% M/M, vs +2.9% prior) as well as in automotive (+5.7% M/M, vs -4.0% prior, highest increase since August 2023) and pharmaceutical production (+6.4% M/M, vs -0.8% prior). There were some weaker sectors, also, however: energy production for instance came in at -6.5% M/M (vs -2.7% prior).

- Despite the strong IP figures, the outlook for German industrial activity remains clouded.

- Other hard data and surveys suggest no rebound is imminent, with February's factory orders surprising to the downside, manufacturing PMI falling to a 5-month low in March, and the March EC manufacturing confidence survey plumbing the lowest levels since the pandemic. Even the construction production growth appears at odds with very weak construction PMI.

- MNI's median of sellside analysts' estimates of Y/Y industrial production hasn't changed in the past month after downward revisions earlier in the year and sees continued falls through Q3 2024 (-5.5% Y/Y Q1, -3.6% Q2, -0.3% Q3, +1.9% Q4).

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok