Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

MNI (London)

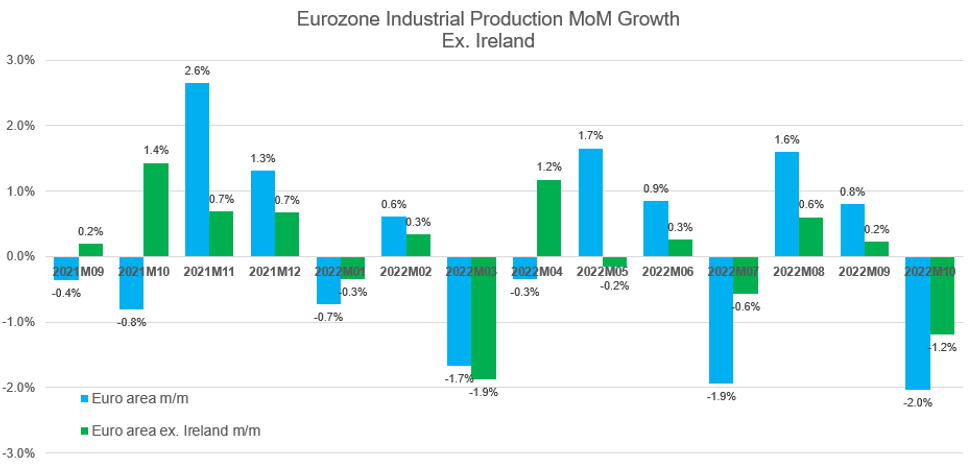

According to MNI calculations based on Eurostat weightings, headline October eurozone industrial production masks a softer decline.

- Irish readings are again distorting the aggregate print largely due to high volatility related to transfer pricing by multinational corporations. October saw a -10.7% m/m plunge following a September +7.1% m/m jump.

- As such, October euro area industrial production likely recorded a softer -1.2% m/m contraction when excluding volatile Irish data. This is 0.8pp higher than the -2.0% m/m fall published in today's headline data, signalling a less drastic slowdown in euro area production.

- On the other hand, there is a large element of supply-side bottlenecks easing allowing production to remain elevated, notably in the automotive sector -- also noted in UK data earlier this week.

- Backlogs boosting production implies the underlying health of the industry is worse than data suggests. These outstanding orders are declining sharply, as flagged by PMI surveys over the past months.

- The October industrial production data follows weak September growth (when excluding Irish data) and appears set to drag substantially on eurozone growth into Q4.

Source: MNI / Eurostat

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok