Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

AUSTRALIA

The earlier preliminary PMI prints for Australia didn't produce much of a reaction in the AUD FX or rates space. This is not a huge surprise as the releases aren't forecast by the market. However, the results point to some softening to Australia's resilient business conditions backdrop. The services PMI is now in contraction territory, (49.6), as is the composite index. The manufacturing index eased back to 54.5 but remains comfortably in expansion territory.

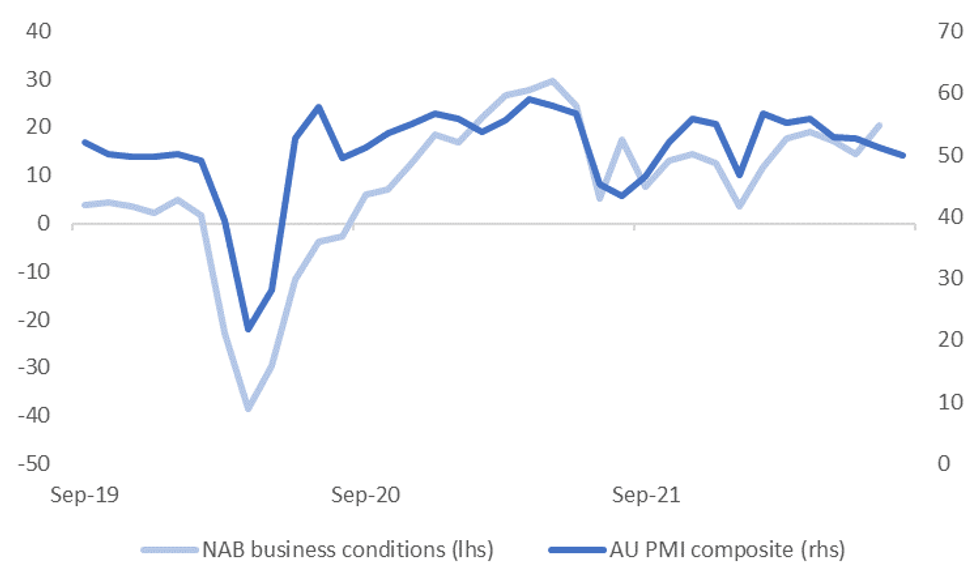

- The caveats with the PMI prints are the relative short history (at least available on Bloomberg). Still, the first chart below shows the reasonable correlation between the PMI composite against the NAB business conditions index, which has a much longer history, over recent years.

- The loss of momentum in the composite index does suggest some downside risks to the next NAB business conditions reading, although the next print is not out until mid-September.

Fig 1: AU PMI Composite Versus NAB Business Conditions

Source: S&P/NAB/MNI/Market News/Bloomberg

Source: S&P/NAB/MNI/Market News/Bloomberg

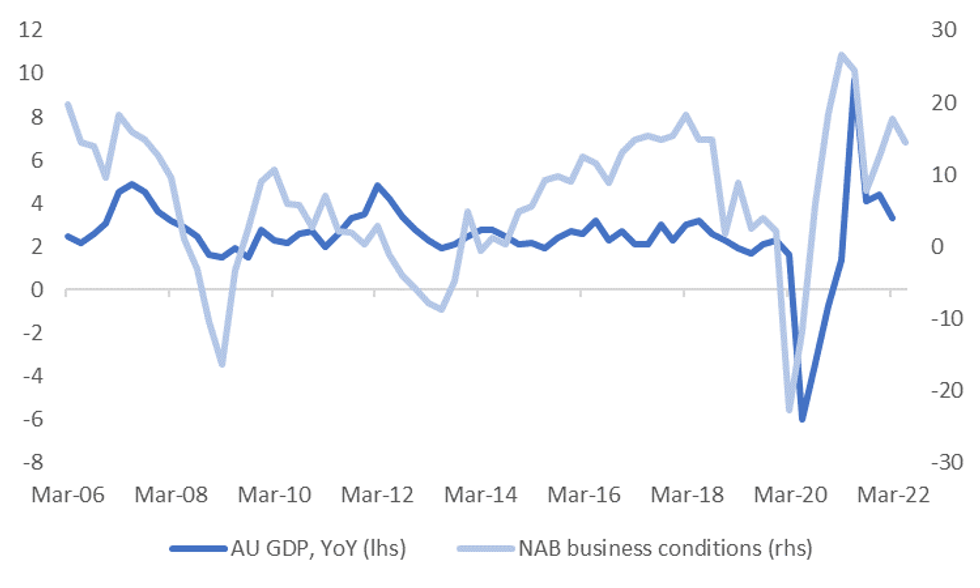

- The second chart below plots the NAB business conditions index against Australian GDP YoY. The rolling 5yr correlation between the two series sits at just under 50%.

- Note as well, the correlation between the PMI composite and service readings is reasonably elevated with Australian retail sales. This is the next major data print in Australia, out next Monday.

- Levels of the PMIs (services and composite) and YoY retail sales have a correlation of around 57%. For MoM retail sales the correlation remains positive, but is around half this level.

- In any event, today's PMI prints suggest some of the softness in global sentiment is starting to seep into Australian conditions, along with tighter financial conditions domestically.

Fig 2: NAB Business Conditions & AU GDP YoY

Source: NAB/MNI/Market News/Bloomberg

Source: NAB/MNI/Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok