Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMANY

Today's Eurozone data showed a 0.2% Q/Q rise in employment in Q2 2023, the slowest since Q3 2022, and a deceleration from 0.5% in Q1. While the national breakdown is as yet incomplete, German jobs growth slowed to 0.1% from 0.2%, with Spanish and Dutch employment slowing sharply as well, helping offset an acceleration in French gains.

- The stagnation in German employment since the first half of 2022 is one of the key factors behind the slowdown, with the country accounting for over one-quarter of eurozone employment. Our estimates of the German Beveridge curve last week showed evidence of a German labour market which was off its tightest levels, but perhaps still too hot for inflation comfort.

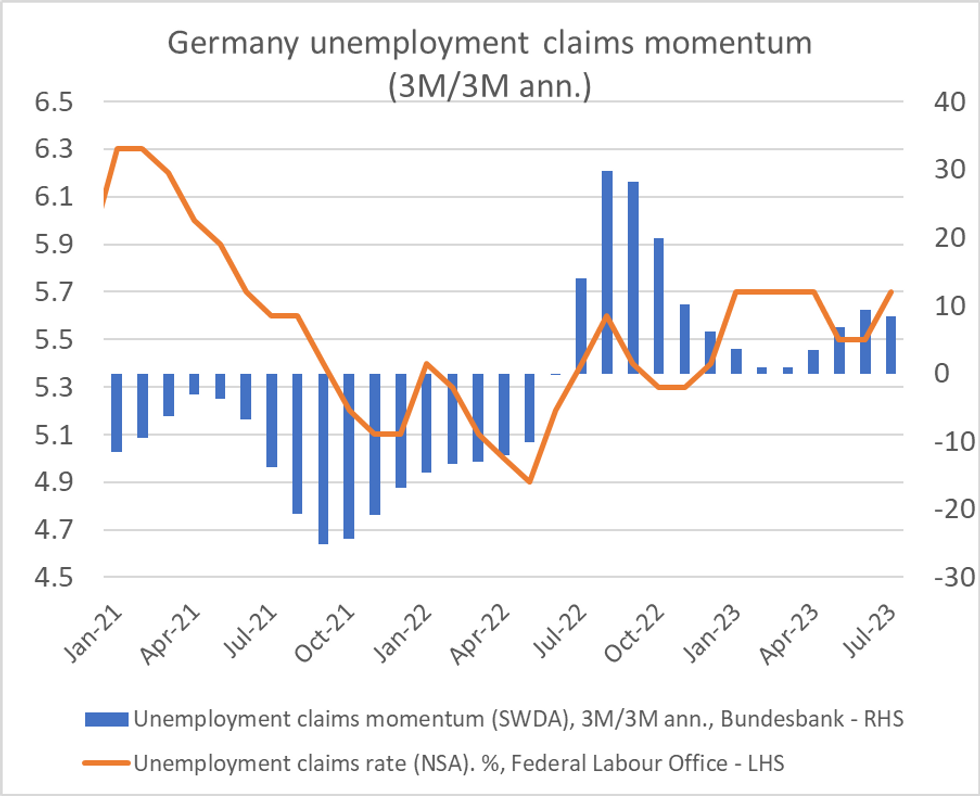

- The dynamics of German unemployment claims since 2021 are shown in the chart below, plotting unemployment claims momentum (on a 3M/3M annualised basis) against the unemployment claims rate.

- Labour market tightness built up throughout 2021 as the economy recovered from the pandemic.

- The geopolitical and energy shock resulting from Russia's invasion of Ukraine prompted a sharp reversal higher in unemployment claims in summer 2022, before momentum faded to near zero at the start of 2023.

- Only in recent months has momentum in unemployment claims picked up again as demand and activity have weakened.

- For Germany, as in much of the Eurozone, the key is whether the ongoing cooling will continue to occur in manufacturing sectors, or if a deterioration in service sector employment will become more prominent.

- The IFO manufacturing employment barometer has been negative for the past 4 months, while the services employment barometer is on a 29 month streak of expansionary prints (albeit off from the highs earlier this year). For context: services jobs make up roughly 75% of total German employment, with manufacturing representing around 17%.

Source: Bundesbank, Federal Labour Office, MNI

Source: Bundesbank, Federal Labour Office, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok