Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ASIA FX

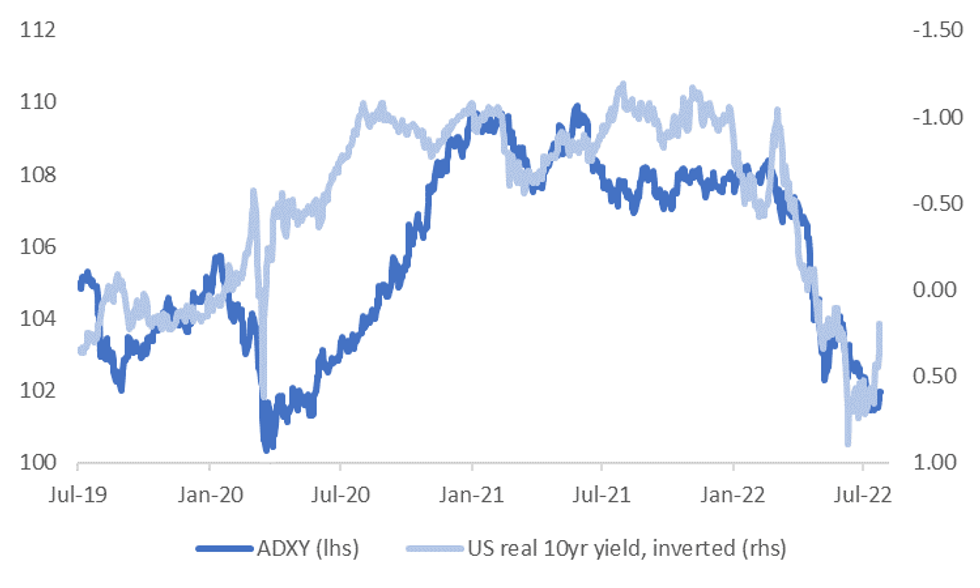

The ADXY currency index has certainly benefited from lower Fed tightening expectations in recent sessions. The first chart below plots the ADXY against the real US 10yr yield, note that the real yield is inverted on the chart.

- The relationship between the two series has been particularly tight since the start of the year.

- If we look at the individual USD/Asia currency pairs, the correlations for the past 6 months are strongly positive. That is, higher US real yields driver USD/Asia pairs higher, all else equal and vice versa when real yields fall. Most correlations are in the 80-90% range.

Fig 1: ADXY & US Real 10yr Yield

Source: J.P. Morgan/MNI/Market News/Bloomberg

Source: J.P. Morgan/MNI/Market News/Bloomberg

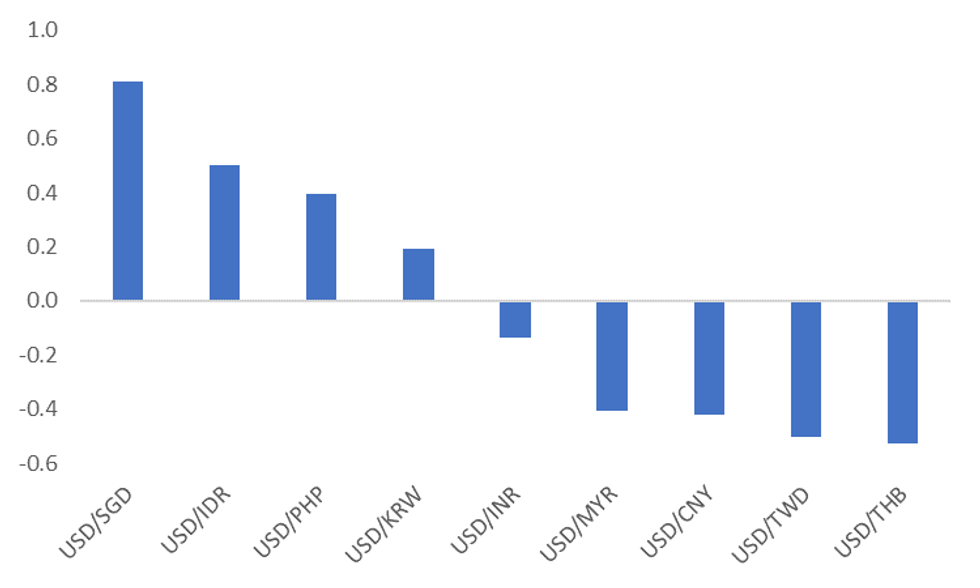

- On a shorter term basis, for the past month, correlations are quite divergent though. See the second chart below.

- If we continue to see real yields correct lower, current correlations suggest USD/SGD, USD/IDR, USD/PHP and USD/KRW may see greater downside compared to the rest of the USD/Asia bloc.

- Interestingly, today IDR and PHP have been the best performers within Asian FX, although clearly other factors could be at play other than the sharp US real yield drop overnight (from +36bps to +20bps).

- For SGD, we suspect this high correlation reflect its correlation the majors (EUR, JPY etc), which themselves are influenced by US yield shifts. For IDR and PHP, it likely reflects sensitivity to external financing conditions, particularly given high foreign ownership levels of Indonesian debt and the Philippines large current account deficit at the moment.

- For the other USD/Asia pairs, we can obviously see a shift in correlations, but it may be the case other drivers are more important for these currencies at the moment.

Fig 2: USD/Asia Correlations With Real US 10yr Yield - Past Month

Source: J.P. Morgan/MNI/Market News/Bloomberg

Source: J.P. Morgan/MNI/Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok