Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GLOBAL

Today's surprise UK CPI print in the UK, following close on the heels of last week's bumper US inflation report, has further intensified the debate around the nature of inflation (transitory or persistent). Regardless of how the inflation surge is being interpreted, central banks are facing increased pressure to respond.

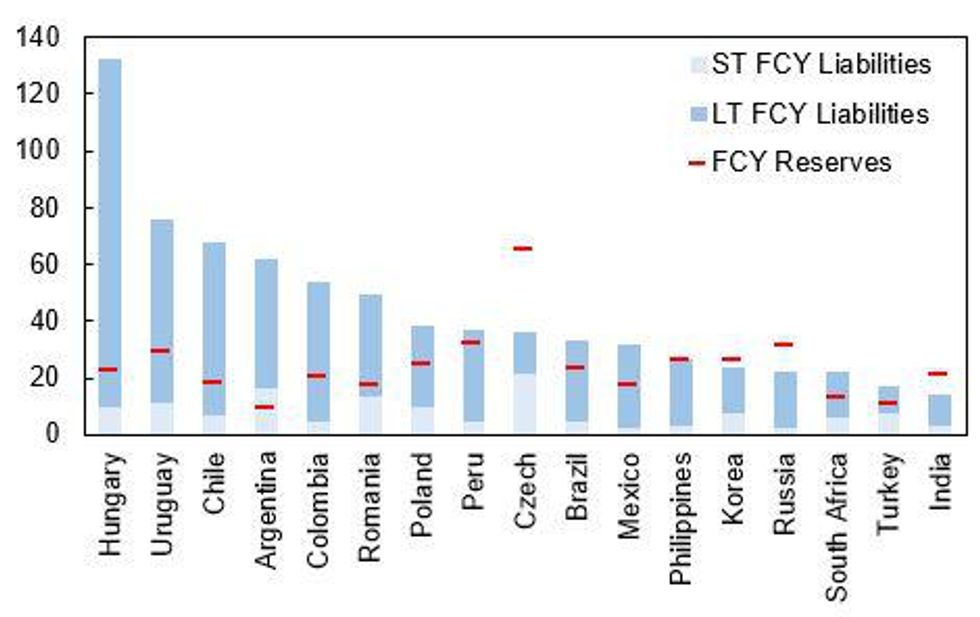

- The likelihood of a shift towards policy tightening in the coming quarter poses a risk to EMs where foreign currency liabilities have been left exposed by insufficient reserves of hard currency.

- The chart below uses the latest comparable Q2 data for foreign currency liabilities from the World Bank and IMF reserve data for the end of Q3 (both normalised by GDP) to give a sense of funding pressures across the EM majors.

- While there are substantial FCY liabilities for the likes of Hungary, Uruguay and Chile, the maturity composition is heavily tilted towards the longer term debt and reserves are more than sufficient to cover near-term funding needs.

- Perhaps unsurprisingly, the most vulnerable on our list is Argentina and Turkey where there is a relatively small reserve buffer for liabilities falling due in the short term.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok