Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

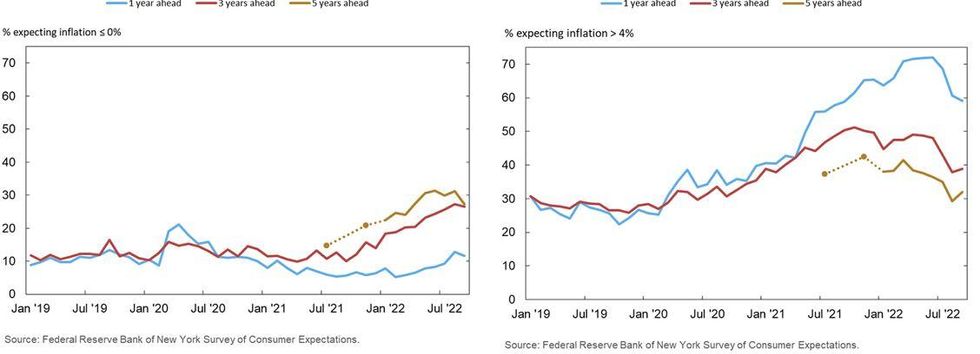

NY Fed President WIlliams'speech on long-term inflation expectations this morning concludes they remain well anchored: US households see the recent rise of inflation as "as likely being less persistent than in prior episodes", with professional forecasters still expecting inflation to remain close to 2% over the longer run.

- However, Williams notes a "surprising wrinkle" that is "worth further study" - there is an increasing divergence in consumer inflation "uncertainty" over the 3-5 year horizon, with rising disagreement in mean expectations as well as in the width of expected inflation distributions.

- While overall long-term inflation expectations have remained anchored since early 2021, there has been a significant increase in the share of respondents to the NY Fed's Survey of Consumer Expectations that expect deflation over the long term.

- The September SCE survey shows about 1/4 of respondents expect deflation 5 years in the future, similar to the proportion seeing inflation above 4% 5 years out. And if anything, the trend is toward rising deflation expectations, while expectations of 4+% inflation are falling.

- This counter-intuitive finding could be due to the way respondents think of inflation - are some respondents merely saying that inflation can't go higher from here, so disinflation is expected further out? (Williams notes the UMich 5-10Y inflation survey showed similar trends toward deflation.)

- Either way, this challenges the "uncertainty" part of Williams' 3 criteria for well-anchored expectations (the others are "sensitivity” and “level", which appear to be met).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok