Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWITZERLAND DATA

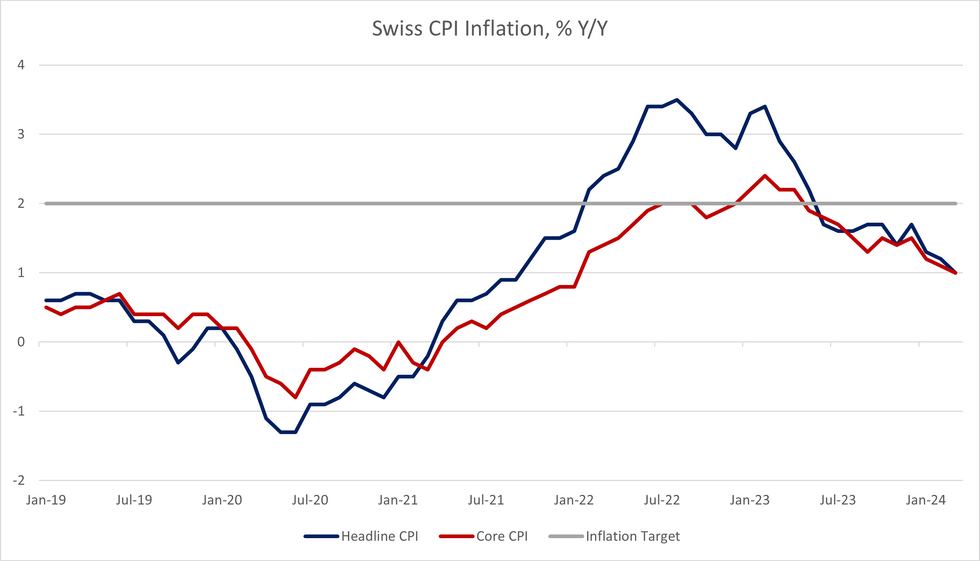

Swiss headline CPI was 1.0% Y/Y and 0.0% M/M in March (vs 1.2% Y/Y, 0.6% M/M prior). Analysts had forecasted a headline print of 1.3% Y/Y and 0.3% M/M.

- Core CPI also printed at 1.0% Y/Y, with the monthly reading at 0.1% M/M (vs 1.1% Y/Y, 0.7% M/M prior).

- Domestic product inflation was 1.8% Y/Y and -0.2% M/M (vs 1.9% Y/Y, 0.5% M/M prior), while imported product inflation remained negative on an annual basis at -1.3% Y/Y and 0.7% M/M (vs -1.0% Y/Y, 1.0% M/M prior).

- This means Q1 Swiss headline CPI averaged 1.17% Y/Y, broadly in line with the SNB’s March monetary policy meeting projections (of 1.2%).

- The CHF has unsurprisingly weakened on the release, with EURCHF 0.5% higher at typing. The cross has now weakened around 1.6% since immediately before the March monetary policy decision, where the SNB unexpectedly cut rates 25bps to 1.5%.

- Per the press release: “Prices for international package holidays and air transport increased, as well as those for clothing and footwear. In contrast, prices for supplementary accommodation and cars decreased, as did those for hire of private means of transport”.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok