Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

The consensus looks for little change in both the manufacturing and non-manufacturing PMIs, which print later today. Other survey measures point to downside risks for both indices, which would be consistent with a softer economic backdrop in recent months. The Citi China EASI has fallen to -76.30 from April highs above 160. Still, the market reaction to any downside surprises may be limited given fresh stimulus measures are being announced, with the efforts to boost consumption growth a clear focus point.

- The consensus for today's July official manufacturing sits at 49.0, unchanged versus June. The range of forecast estimates is 48.5 to 50.0.

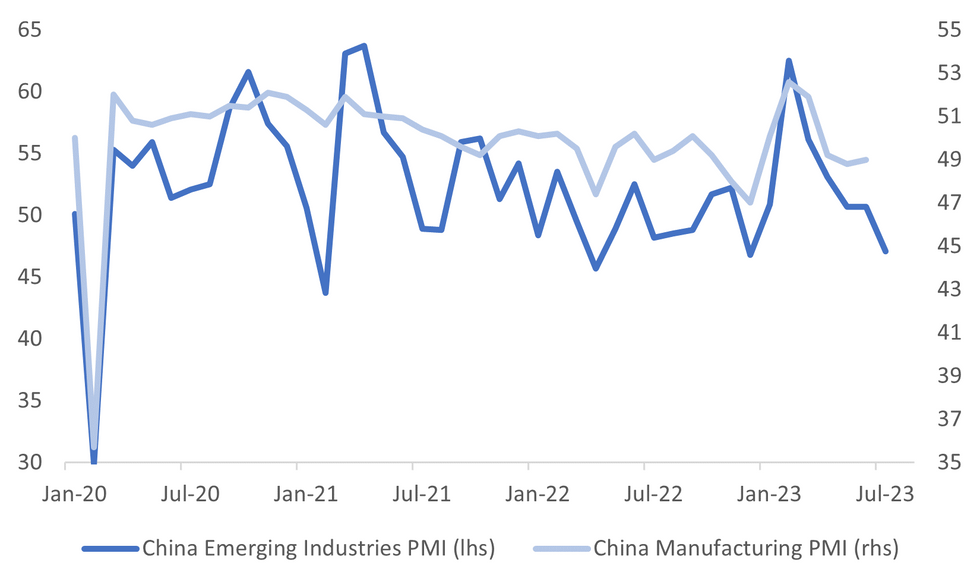

- The chart below plots the official PMI index against the China emerging industries PMI, which has already printed for July. This index slumped to 47.1 from 50.7 in June. There are of course some caveats to be mindful of. The emerging industries PMI has typically tracked below the official PMI and often experiences deeper troughs compared to the official index.

- Still the correlation between the two indices is +64% in the past 2 years. A manufacturing PMI which remained in contraction territory and/or lost some momentum in July would be consistent with the general sense of the economy losing momentum and needing fresh policy support in recent months.

Fig 1: Official Manufacturing PMI and Emerging Industires PMI

Source: MNI - Market News/Bloomberg

- On the non-manufacturing or services side, the consensus estimate sits at 53.0, versus a 53.2 outcome in June. The range of forecasts is 52 to 54.

- The Standard Chartered China SME confidence index fell further in July to 50.7, lows back to late 2022 for this index. This is consistent with a further loss of momentum on the services side, although the consensus is still expecting conditions to remain in expansion territory.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok