Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

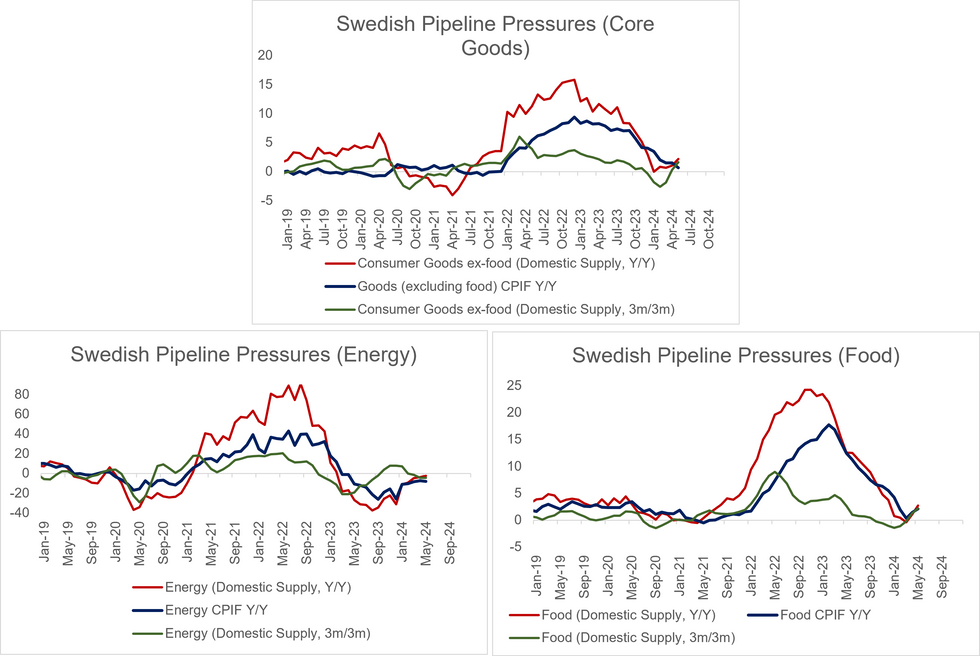

Swedish PPI rose 2.6% Y/Y in May (vs 0.9% prior) and was unchanged M/M. There was no consensus for the print. The increase in the annual rate comes following a very soft May 2023, where PPI fell 1.7% M/M.

- The price index for domestic supply, which takes into account domestic PPI and import prices, also rose 2.6% Y/Y (vs 0.6% prior). Excluding energy, this index rose 3.6% Y/Y (vs 1.5% prior) and 2.1% on a 3m/3m basis (vs 1.0% prior).

- Details show that core goods pipeline pressures accelerated in May, with capital goods domestic supply prices up 4.5% Y/Y (vs 3.6% prior) and 1.4% 3m/3m (vs 1.1% prior) and consumer goods ex-food rising 2.2% Y/Y (vs 1.1% prior) and 1.6% 3m/3m (vs 0.3% prior).

- The SEK strengthened against the EUR, USD and NOK on an annual and monthly basis in May, which may have offset some of the rise in imported prices.

- The chart pack below suggests both core goods and good CPIF disinflation is likely to fade in the coming months, putting the onus on services to ensure CPIF ex-energy continues its return to the 2% target.

- Energy pipeline pressured fell in May, due to lower electricity and refined petroleum prices.

- Focus remains on the Riksbank meeting tomorrow though. Our preview is here.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok