Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

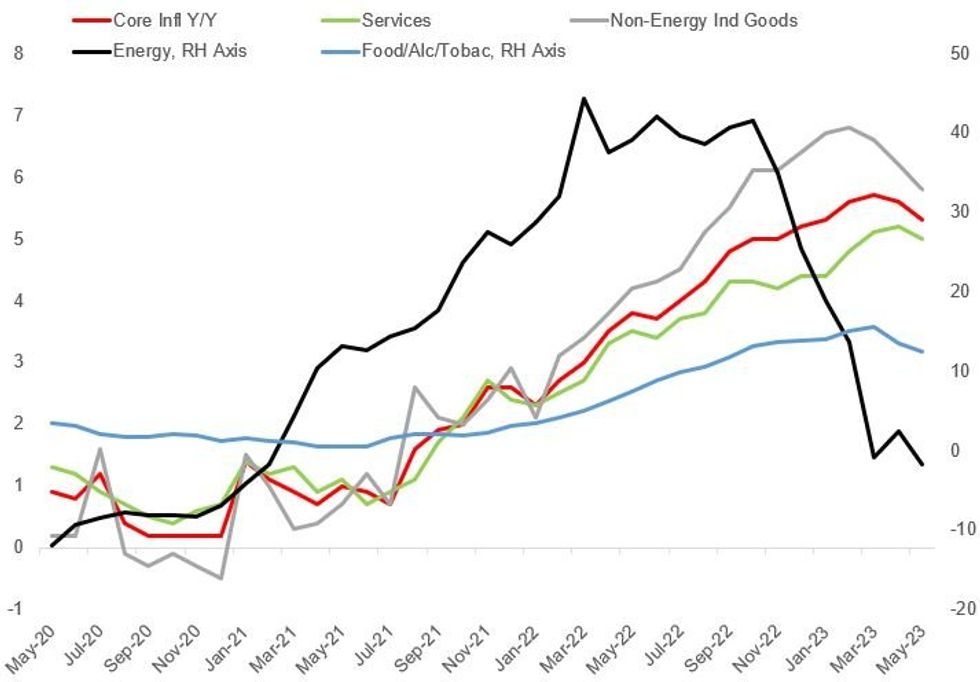

The inflation deceleration evident in May's flash Euro area prints last week brought little surprise after the marked-to-market estimates were implicitly revised down following the mostly softer national-level readings. Headline's 6.1% Y/Y was lower than the 6.3% expected going into the week and down 0.9pp vs April, with core of 5.3% Y/Y likewise softer than the 5.5% survey and 0.3pp down from April.

- Even with this apparent improvement there remains significant debate about both the significance of the May reading and the path forward: how the inflation picture looks for the rest of the year, and ultimately what it means for ECB policy.

- The optimistic appraisal begins with the fact that inflation was seen slowing across the board, from food to energy to core: non-energy industrial goods (5.8% vs 6.2% prior) and services (5.0% vs 5.2% prior) pointed to disinflationary pressures increasing as food (12.5% vs 13.5%) and energy (-1.7% vs 2.4%) continue to recede.

- But there are multiple caveats. Most importantly for the May reading, the services slowdown was impacted by German transportation subsidies in the month, and by several estimates, core inflation may have been flat absent that factor. And overall, core may tick back higher in the coming months, with services seen playing a resurgent role as core goods/energy/food price inflation recedes.

- June 16's comprehensive breakdown of the price data will provide a clearer picture albeit this will be a day after the ECB announces its rate decision.

- In the meantime we survey some of the more interesting angles on the May eurozone reading that we've seen, highlighting the general view that the eurozone is still some ways from seeing significant progress on underlying price pressures.

Eurozone Inflation By Category. % Y/YSource: Eurostat, MNI

Eurozone Inflation By Category. % Y/YSource: Eurostat, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok