Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Risk Sours

Treasury futures trade steady/mixed after the bell, well off early session lows as risk appetite cooled by midmorning. Overall volumes remain muted due to limited holiday participation

- After rising to new all-time highs in early trade, equities reversed, near session lows in late trade. Trading desks citing various factors including asset re-allocation out of stocks into Tsys ahead month/yr end, headline risk associated w/stimulus relief vote in Senate, weakness in Apple shares after making new highs also noted.

- Midday selling after Sen Majority leader Mitch McConnell "BLOCKS SCHUMER MOVE TO QUICKLY PASS $2,OOO CHECKS" Bbg. Dow Jones reported soon after that "McConnell suggests he'll tie bigger stimulus checks to Internet, voting issues."

- No significant react to Case Shiller Home Index (+1.7%) nor the third consecutive weak note auction of the week: US Tsy $59B 7Y Note auction (91282CBB6) draws high yield 0.662% rate (0.653% last month) vs. 0.660% WI; 2.31 bid/cover vs. 2.37 prior.

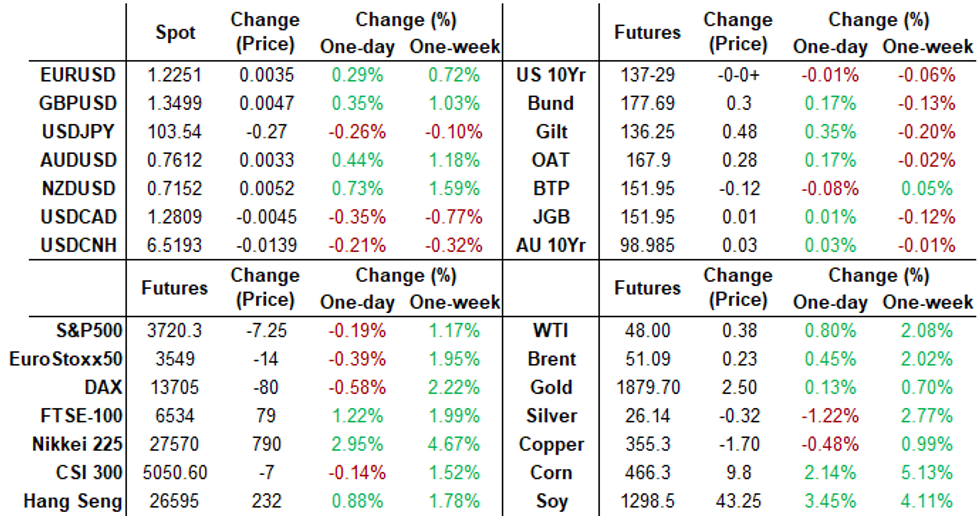

- The 2-Yr yield is up 0.8bps at 0.127%, 5-Yr is up 2.2bps at 0.3766%, 10-Yr is up 1bps at 0.9331%, and 30-Yr is up 1.2bps at 1.671%.

MONTH-END EXTENSIONS: Updated Bloomberg-Barclays US Extension Estimates

Forecast summary compared to the avg increase for prior year and the same time in 2019. TIPS -0.03Y; Govt inflation-linked, -0.04. Note MBS extension climbs to 0.14Y from 0.09 in preliminary.

| Estimate | 1Y Avg Incr | Last Year | |

| US Tsys | 0.08 | 0.09 | 0.07 |

| Agencies | 0.08 | 0.06 | 0.09 |

| Credit | 0.07 | 0.09 | 0.07 |

| Govt/Credit | 0.07 | 0.09 | 0.07 |

| MBS | 0.14 | 0.05 | 0.09 |

| Aggregate | 0.08 | 0.08 | 0.06 |

| Long Gov/Cr | 0.07 | 0.09 | 0.06 |

| Iterm Credit | 0.05 | 0.08 | 0.06 |

| Interm Gov | 0.09 | 0.08 | 0.07 |

| Interm Gov/Cr | 0.08 | 0.08 | 0.06 |

| High Yield | 0.08 | 0.08 | 0.09 |

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N +0.00638 at 0.08738% (-0.00338 net last wk)

- 1 Month +0.00162 to 0.14675% (+0.00138 net last wk)

- 3 Month +0.01375 to 0.25388% (+0.00438 net last wk)

- 6 Month -0.00950 to 0.25713% (+0.00813 net last wk)

- 1 Year +0.00087 to 0.34125% (+0.00638 net last wk)

- Daily Effective Fed Funds Rate: 0.09% volume: $73B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $161B

- Secured Overnight Financing Rate (SOFR): 0.09%, $946B

- Broad General Collateral Rate (BGCR): 0.07%, $354B

- Tri-Party General Collateral Rate (TGCR): 0.07%, $323B

- (rate, volume levels reflect prior session)

Updated NY Fed operational purchase schedule, $40.2B from 1/04-1/14

- Mon 1/04 1100-1120ET: Tsy 2.25Y-4.5Y, appr $8.825B

- Tue 1/05 1100-1120ET: Tsy 20Y-30Y, appr $1.750B

- Wed 1/06 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Thu 1/07 1100-1120ET: Tsy 20Y-30Y, appr $1.750B

- Fri 1/08 1100-1120ET: Tsy 0Y-2.25Y, appr $12.825B

- Mon 1/11 1010-1030ET: TIPS 1Y-7.5Y, appr $2.425B

- Tue 1/12 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Wed 1/13 1010-1030ET: Tsy 7Y-20Y, appr $3.625B

- Thu 1/14 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Thu 01/14 Next forward schedule release at 1500ET

EURODOLLAR/TREASURY OPTIONS: Summary

Eurodollar Options- -2,000 Dec 97 straddles 14.0 over Blue Nov 95/96 put spds

- +2,800 short Jun 95/96/98/100 call condors, 10.75

- +1,000 Red Jun 90/92/95/97 put condors, 3.5

- +2,000 Gold Jun 82/85/87 put flys, 2.5

- +2,000 Red Dec 96/97 put spds, 4.75

- +2,000 Red Jun 98 calls, 4.0

- -1,500 Red Mar 97 straddles, 13.0

- Overnight Trade:

- +10,000 Jun 100.12 calls, 0.25, negative rate

- +8,000 Jun 97/81 1x2 call spds, 1.5

- +4,000 Blue Feb 96 calls

- +1,500 Jan/Feb 81 call strips, 4.75

- +2,800 TYH 135.5/136.5 put spds, 9

- +4,000 TYH 137.5 puts 1 over TYG 138 puts

- -2,100 TYG 137.25/138.25 strangles, 33-34

- -1,000 TYH 138 calls, 42

- Overnight Trade

- +11,000 TYG 139.5 calls, 3

- +2,000 USG 168/170 put spds, 22

EGBs-GILTS CLOSE: EGBs-GILTS: Covid Concerns Continue, Focus On Equivalence

EGB and gilt markets have clearly been suffering from a holiday hangover. EGBs have remained within yesterday's ranges. Gilts rallied at the open to catch up with yesterday's moves and have pushed on a little higher but on little new news today.

- The market debate has focused on the final deal the EU and UK will strike on financial services, with the Brexit deal agreed before Christmas not specifically mentioning equivalence so some uncertainty still remains.

There has also been some focus on Covid-19 numbers across the region, as - There has also been some focus on Covid-19 numbers across the region, as concerns about the new strain first identified in the UK which spreads more easily has led to vigilance on the numbers of cases across the Eurozone.

Furthermore, media reports that it may take until the end of January for the - Furthermore, media reports that it may take until the end of January for the EU to sign off use of the AZ/Oxford vaccine has helped peripheral spreads widen on the day, led by Italy with 10-year spreads widening 2.3bp at writing.

EUROPE OPTIONS SUMMARY: Limited Volume

- RXG1 175p, bought for 8 in 7k

FOREX: Summary

Further USD selling continuation during the US morning session.

- EURUSD tested MNI tech resistance at 1.2273 High Dec 17 and the bull trigger, printed 1.2275 high.

- The pair has since faded back lower with better USD buying emerging, after Equities fell from their high of the session.

- AUDUSD extended gains, through high of the session.

- US stimulus and Brexit, is benefiting riskier and risk tied assets.

- While AUD trades on the front foot on the weaker Dollar, it is trading through the lowest levels versus the NZD since the 17th of Dec.

- Looking ahead, expect to see more Month End related price action as liquidity dissipates.

- Citi FX: Dec month-end points to moderate USD sales into the final month-end fix of the year

- Barcap FX: The passive rebalancing model points to strong USD selling versus majors at month-end. The signal is moderate against the EUR

FX OPTIONS: Expiries for Dec 30 NY Cut 100ET (Source DTCC)

- EURUSD: 1.2166 (358mln), 1.2250 (662mln), 1.2275 (407mln), 1.2300 (206mln), 1.2400 (880mln)

- GBPUSD: 1.3400 (523mln), 1.3600 (976mln)

- USDJPY: 103.00 (200mln)

EQUITIES: Midmorning Reversal, Bid Evaporates

Equities reversed course midmorning, ESH1 pared gains from a high of 3747.75 to 3714.5 low in late trade. Some desks suggest asset reallocation going into month/year end, others pointing to Apple shares leading early sale. Desk expect Month End hedges out of Equities following the big gains of late, and this is the most likely driver

- Japan's NIKKEI up 714.12 pts or +2.66% at 27568.15 and the TOPIX up 31.14 pts or +1.74% at 1819.18

- China's SHANGHAI closed down 18.249 pts or -0.54% at 3379.036 and the HANG SENG ended 253.86 pts higher or +0.96% at 26568.49

- The German Dax down 28.91 pts or -0.21% at 13761.38, FTSE 100 up 100.54 pts or +1.55% at 6602.65, CAC 40 up 23.41 pts or +0.42% at 5611.79 and Euro Stoxx 50 up 5.96 pts or +0.17% at 3581.37.

- Dow Jones mini down 82 pts or -0.27% at 30225, S&P 500 mini down 8.5 pts or -0.23% at 3719.25, NASDAQ mini up 6 pts or +0.05% at 12839.25.

COMMODITIES:

WTI and crude futures gained along with surging prices in metals Tuesday amid pressure in US$.

- WTI Crude up $0.34 or +0.71% at $47.95

- Natural Gas up $0.16 or +7.03% at $2.467

- Gold spot up $4.7 or +0.25% at $1878.26

- Copper down $2.05 or -0.57% at $355.1

- Silver down $0.1 or -0.38% at $26.1469

- Platinum up $20.18 or +1.95% at $1053.59

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.