Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: New 1Y Yield Highs

Reflation theme finished strong Friday, at least in Tsys -- selling off to new lows after recent headline from Sen Schumer re: fiscal stimulus bill on track for March 14 passage. Equities lagging as ESH1 pared losses late to 3912.0 vs Tue's high of 3960. New 1Y yield highs: 10YY 1.3601%, 30YY 2.1526%.

- Midmorning sell-off following better than expected existing home sales, bonds extended session lows into noon, curves making new 5Y highs (5s30s 156.326) as hopes improved vaccine inventory/distribution ahead spring spells for improved summer economic outlook.

- About an hour later several stimulus related headlines during second half rounding out the week on a positive note: SCHUMER SAYS SENATE ON TRACK TO PASS STIMULUS BEFORE MARCH 14, Bbg, while House Budget Comm just released text of stimulus bill ahead Monday's markup.

- Heavier futures trade, this time March/June futures rolling did play a part in driving volumes: >755k FVH/FVM by the bell making up just over 40% of total FVH volume on day. March Tsy option expiration contributed to flows as did continued positioning of put positions out and down in strike.

- The 2-Yr yield is up 0.2bps at 0.1068%, 5-Yr is up 2.6bps at 0.5791%, 10-Yr is up 4.9bps at 1.3448%, and 30-Yr is up 6bps at 2.1416%.

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N -0.00200 at 0.07813% (-0.00150/wk)

- 1 Month +0.00437 to 0.11550% (+0.00812/wk)

- 3 Month -0.00713 to 0.17525% (-0.01850/wk) ** Record Low (prior 0.18138% on 2/17/21)

- 6 Month -0.00188 to 0.19500% (-0.00575/wk)

- 1 Year -0.00450 to 0.28650% (-0.01325/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $73B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $215B

- Secured Overnight Financing Rate (SOFR): 0.03%, $872B

- Broad General Collateral Rate (BGCR): 0.02%, $365B

- Tri-Party General Collateral Rate (TGCR): 0.02%, $333B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $8.801B accepted vs. $22.442B submission

- Next scheduled purchases:

- Mon 2/22 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Tue 2/23 1010-1030ET: TIPS 1Y-7.5Y, appr $2.425B

- Wed 2/24 1010-1030ET: Tsy 7Y-20Y, appr $3.625B

- Thu 2/25 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Fri 2/26 1010-1030ET: Tsy 0Y-2.25Y, appr 12.825B

EURODOLLAR/TREASURY OPTIONS: Summary

Eurodollar Options:- 5,000 Gold Sep 97.875/98.25 put spds, rolling down

- 7,500 Gold Apr 82 puts, 8.0

- +10,000 Green Apr 99.56/99.687 1x2 call spds, 3.5

- +20,000 Green Jun 93 puts, 4.5

- +10,000 Green Jun 87/90 put spds, 0.75,

- Overnight trade

- +13,000 Mar 93/98 call spds, 0.5 vs. 99.8625/0.10%

- 5,000 Green Apr 99.562/99.687 1x2 call spds. 3.5

- 8,800 TYJ 136/136.5 call spds, 4 matches earlier Block

- -6,000 FVM 124 puts, 15

- Block, 8,000 TYJ 136/136.5 call spds, 4 vs. 134-15/0.07%

- Block, 11,000 USM 163 puts, 328 vs. 161-31/0.55%

- Block 20,000 TYJ 133.5/134.5 put spds,m 22

- -4,000 TYJ 132/136.5 strangles, 12

- -1,000 TYM 134.5 straddles, 211

- Overnight trade

- 30,000 (20k Blocked) FVJ 124.5/125.5 put over risk reversals, 1-1.5

- 14,000 TYH 136 calls, 1

- 13,000 TYH 135.5 puts, 2-4

- 10,000 TYH 136 puts, 18 last, from 10-21

- 9,000 TYJ 136 calls, 11

- 2,000 TYJ 133/134/135 put flys

BONDS: EGBs-GILTS CASH CLOSE: Real Yields Soar

Core curves ended the week with a bang at the long end, with a risk-on tone boosting real rates (breakevens were flat/down) and leading to sharp bear steepening in Bunds and Gilts.

- Equities rose all session with the EUR and GBP gaining ground on the dollar.

- Flash February PMIs were mixed w manufacturing beating expectations but services not so much. In the eurozone, Germany continues to outperform France.

- UK PMIs were stronger than expected, offsetting disappointing Jan retail sales. GBP hit a 3-yr high vs the USD above 1.40. The 10-Yr Gilt underperformed on the curve.

- BTP spreads and those of peripheries more broadly fell sharply on rising risk appetite.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 0.7bps at -0.681%, 5-Yr is up 2.1bps at -0.608%, 10-Yr is up 4.1bps at -0.305%, and 30-Yr is up 5.6bps at 0.213%.

- UK: The 2-Yr yield is up 2.7bps at -0.011%, 5-Yr is up 5.9bps at 0.199%, 10-Yr is up 7.6bps at 0.698%, and 30-Yr is up 6.6bps at 1.268%.

- Italian BTP spread down 6.5bps at 92.9bps / Spanish spread down 2.6bps at 66bps

OPTIONS: EUROPE SUMMARY: Several Large Rates Trades

Friday's options flow included:

- RXJ1 172.50/173.50/175c fly, bought for 9.5 in 2k

- RXJ1 172c, bought for 67 in 1.5k

- OEJ1 135.75/136.25cs, bought for 3 in 2k

- OEJ1 134.50/134.00 put spread bought for 9.5 in 4k

- ERU1 100.50/100.625/100.75 call fly bought for 4 in 15k

- 0RZ1 100.50/100.375 1x2 put spread bought for 0.5 in 8k

- 0LM1 99.87/100cs vs 3LM1 99.62/99.75cs, bought the 1yr for half in 6.5k

- 0LU1 99.875/99.75/99.625 1x3x2 put fly bought for 0.5 in 7k

- 2LU1 99.62/99.75cs x2 vs 3LU1 99.50/99.75cs, bought the 2yr for 3.5 in 12kx6k

- 2LU1 99.25p (v 99.58) + 2LZ1 99.25p (v 99.515), bought for 9.25 in 10k strips

- 3LH1 99.75/99.87cs, bought for half in 2.5k (ref 99.52, 2 del)

- 3LM1 99.62/99.37ps vs 2LM1 99.75p, bought the put for 0.75 in 5k

- 3LM1 99.62/99.75/99.87c fly, bought for 1.5 in 2k and 1.25 in 5k

- 3LU1 99.125/99.875/99.625 put fly bought for up to 3.25 in 22k on the day

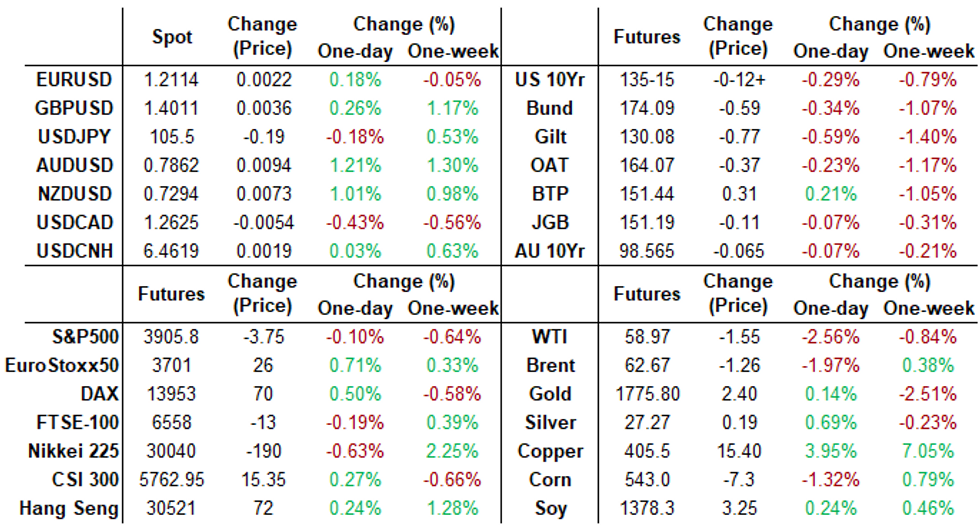

FOREX:: AUD, GBP Hit Multi-Year Highs vs. USD

AUD, NZD outperformed well throughout the Friday session, with AUD/USD topping the early January highs to high the best level since early 2018. A global commodity rally and the upward revision to Westpac's Australian yield forecasts were the primary drivers. This narrowed the gap with next resistance at 0.7885.

- The greenback traded poorly despite an uptick in both US Treasury yields and equity markets in the US and on the continent. This pressured the USD index toward the week's lowest levels printed on Tuesday at 90.12. A break below here opens key support at 90.05. The break of $1.40 in GBP/USD helped pressure the USD index further, with the pair touching new multi-year highs.

- Focus in the coming week turns to German IFO numbers, UK jobs data and personal income/spending & MNI Chicago PMI from the US. Highlight of the central bank speaker schedule will be the delivery of the semi-annual testimony from Fed's Powell.

FX OPTIONS: Expiries for Feb22 NY cut 1000ET (Source DTCC)

- USD/JPY: Y104.00($600mln)

- AUD/USD: $0.7715(A$640mln)

- NZD/USD: $0.7175-85(N$515mln)

PIPELINE: Global Payments Launched

Friday's sole issuer helps push high-grade issuance to $14.5B for the week

- Date $MM Issuer (Priced *, Launch #)

- 02/19 $1.1B #Global Payments 5Y +63

- $7.25B Priced Thursday

- 02/18 $3B *Charter Comm's $1.5B 20Y +162.5, $1B 30Y +183, $500M 2061 Tap +205

- 02/18 $1.5B *Masco $600M 7Y +60, $600M 10Y +80, $300M 30Y +105

- 02/18 $1.5B *Prov of Ontario 10Y +26

- 02/18 $1.25B *BNP Paribas PerpNC10 4.625%

EQUITIES: Stocks Solid, But Short of Alltime Highs

Having topped out at the Wednesday high, equities had looked fragile headed into Friday, but a bounce in European and US indices helped stall any protracted downside as prices stabilised. Industrials and materials traded well, helping support the S&P 500, while utilities and communication services lagged. The VIX traded lower as equities stabilised and traded within range of the 2021 lows printed in mid-February.

- The e-mini S&P traded inside Thursday's range, keeping the directional parameters intact. A break above 3936 would reignite the upside argument, opening another test on the 3959.25 all time highs.

COMMODITIES: WTI, Brent Bull Run Eases

After a fearsome rally over the past three weeks, WTI and Brent crude futures moderated Friday. Losses were muted, with WTI retreating just over 1% from the Thursday close. With inclement weather in the southern US states expected to ease over the weekend, a number of producers have begun to put production back online, soothing supply pressures into next week.

- The pullback in prices eased the overbought outlook for WTI. The RSI hit multi-decade highs mid-week, levels not seen since the 1990 oil price shock, in which prices more than doubled over the course of a few months.

- Gold and silver traded in minor positive territory, benefiting from a weaker greenback throughout the Friday session, but the bounce was shallow after prices touched new 2021 lows during Asia-Pac hours at 1760.67.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.