Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TYS SUMMARY: Risk-Off Gains Momentum

Generally a nascent risk-off tone to midweek session: stocks pared gains/traded weaker while Tsys trade strong after the closing bell, just off late session highs (but off early overnight levels) yield curves mildly flatter, decent over all volumes (TYM >1.5M).

Indifferent data react, Tsy futures pared overnight gains, 2s-30s held just above steady on two-way flow post-data: Durables new orders -1.1%/ex-trans -0.9%. Two-way flow with slightly better buying in 10s-30s.- Small auction tail: Tsys slipped briefly after US Tsy $61B 5Y Note auction (91282CBT7) drew high yld of 0.850% (0.621% last month) vs. 0.847% WI; 2.36 bid/cover vs. 2.24 prior. Indirects drew 58.08% vs. 57.05% prior, directs 16.62% vs. 14.38% prior, dealers 25.31% vs. 28.57% prior.

- Rates gradually rebounded, inched higher in latter/second half of session as equities traded back to early overnight lows. Focus on Thursday's weekly claims and flurry of more Fed speakers.

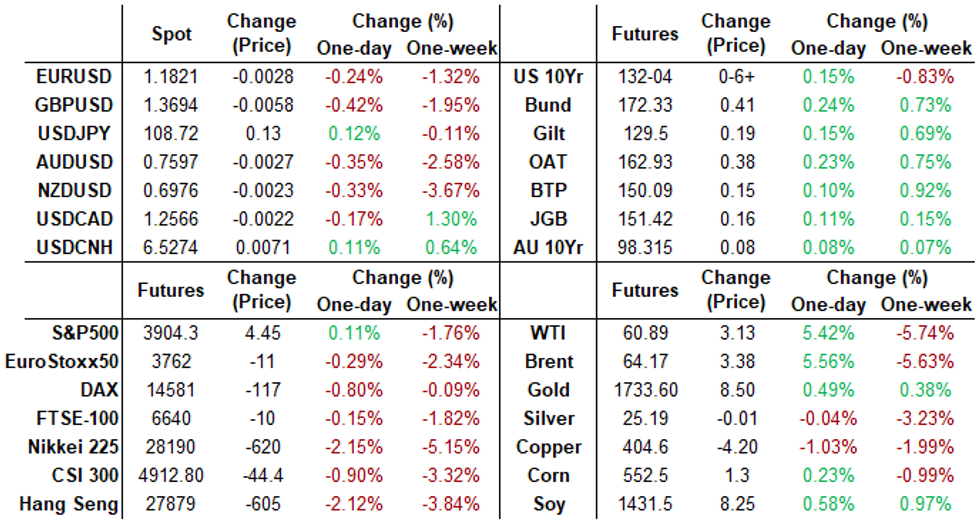

- The 2-Yr yield is down 0.1bps at 0.1446%, 5-Yr is down 0.8bps at 0.8076%, 10-Yr is down 1.4bps at 1.6067%, and 30-Yr is down 1.9bps at 2.3079%.

MONTH-END EXTENSIONS: Preliminary Barclays/Bbg Extension Estimates

Forecast summary compared to the avg increase for prior year and the same time in 2020. TIPS 0.07Y; Govt inflation-linked, 0.02. Notice the bounce in US Tsy, Agency and MBS estimates, and drop in Credit extension est vs. last year.

| Estimate | 1Y Avg Incr | Last Year | |

| US Tsys | 0.07 | 0.09 | -0.03 |

| Agencies | 0.03 | 0.05 | -0.03 |

| Credit | 0.09 | 0.09 | 0.16 |

| Govt/Credit | 0.08 | 0.09 | 0.06 |

| MBS | 0.12 | 0.06 | 0.03 |

| Aggregate | 0.09 | 0.08 | 0.04 |

| Long Gov/Cr | 0.1 | 0.09 | 0 |

| Iterm Credit | 0.09 | 0.08 | 0.09 |

| Interm Gov | 0 | 0.08 | 0.01 |

| Interm Gov/Cr | 0.09 | 0.08 | 0.05 |

| High Yield | 0.12 | 0.1 | 0.12 |

SHORT TERM RATES

US DOLLAR LIBOR: Latest settles:

- O/N -0.00050 at 0.07638% (-0.00050/wk)

- 1 Month +0.00162 to 0.11025% (+0.00187/wk)

- 3 Month -0.00550 to 0.19513% (-0.00175/wk) (Record Low of 0.17525% on 2/19/21)

- 6 Month +0.00412 to 0.20950% (+0.00712/wk)

- 1 Year +0.00062 to 0.28000% (+0.00375/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $71B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $247B

- Secured Overnight Financing Rate (SOFR): 0.01%, $896B

- Broad General Collateral Rate (BGCR): 0.01%, $383B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $349B

- (rate, volume levels reflect prior session)

- Tsys 2.25Y-4.5Y, $8.801B accepted vs. $24.564B submission

- Next scheduled purchases:

- Thu 3/25 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Fri 3/26 No buy operation

US TSYS/OVERNIGHT REPO: Specials See Slight Improvement

Overnight repo remains at special across the curve but see slight improvement along with Bills. Current levels:

T-Bills: 1M 0.0025%, 3M 0.0127%, 6M 0.0355%; Tsy General O/N Coll. 0.02% vs. 0.00% Monday.

| Duration | Current | Old Issue |

| 2Y | -0.02% | 0.00% |

| 3Y | 0.00% | -0.19% |

| 5Y | -0.31% | -0.01% |

| 7Y | -0.16% | 0.01% |

| 10Y | -0.18% | -0.14% |

| 30Y | -0.07% | -0.02% |

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +5,000 May 98 calls, 0.25

- +5,000 Dec 100 calls, 0.5

- -2,500 Green May 93/Blue May 86 straddle strip, 47.0

- +7,500 Red Jun 93/96 put spds, 2.5

- +5,000 short Aug 95/96/97 put flys, 3.5, paper adding to large position started Mar 8: appr 70k from 2.5-3.5

- over +21,000 Green Jun 91/95 put over risk reversals, 1.5

- +5,000 Green Jun 91/92/93 put trees, 0.0

- +2,000 Red Jun 93/96 put spds, 2.5

- Overnight trade

- 2,000 Green May 91/92 put spds

Treasury Options:

- -3,000 FVK 122.75/123.5 put spds, 8

- +8,000 USK 167 calls, 3

- -3,000 TYK 134.5 calls, 3

- over -4,500 FVM 121/122 put spds, 3-3.5

- +1,500 TYK 129.5/131.5 put strip 6 over TYJ 132 puts

- +1,500 TYJ 132 puts, 21

- -3,000 FVK 123.5 puts 13-14 earlier

- +1,000 FVJ 123.75 puts, 3

- Overnight trade

- +13,000 TYJ 131/131.5 put spds, 2-3 vs. 132-04 to -07.5/0.12%

- 5,500 TYK 129 puts, 5

- 3,500 TYM 128 puts, 10

EGBs-GILTS CASH CLOSE: Data Takes Top Billing

The Bund and Gilt curves flattened modestly Wednesday, but an early fall in yields fully reversed following stronger-than-expected PMI data for Germany, France, and the UK.

- Some mixed interpretations of the PMI data (ie survey taken before renewed lockdowns in the Eurozone) dampened the impact, however, with yields well off highs by session's end. Earlier, UK Feb inflation came in much weaker than expected, helping boost Gilts at the open.

- Periphery EGBs continued their recent impressive performance, tightening vs Bunds.

- EU-UK vaccine tensions simmered, though a WSJ reporter suggested a mutual statement on cooperation could be issued this evening. Looking ahead, Thursday's highlights include the European Council summit which will include discussion of the COVID vaccine situation.

- We also get Italian BTP linker + 2022 nominal auction Thursday, and appearances by BOE's Bailey and ECB's Lagarde among many others.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 0.3bps at -0.712%, 5-Yr is down 1.2bps at -0.682%, 10-Yr is down 1.2bps at -0.353%, and 30-Yr is down 2.1bps at 0.21%.

- UK: The 2-Yr yield is up 1.5bps at 0.061%, 5-Yr is up 0.4bps at 0.334%, 10-Yr is down 0.5bps at 0.758%, and 30-Yr is down 0.6bps at 1.282%.

- Italian BTP spread up 0.1bps at 94.4bps /Spanish spread down 0.6bps at 62.8bps

OPTIONS/EUROPE SUMMARY: A Bit More Downside Than Upside

Wednesday's options flow included:

- OEM1 134.25/136.25^^, sold at 10 in 1.5k

- RXK1 169p, bought for 9.5 in 2kRXK1 167p, bought 2.5 in 6k

- RXK1 174/175/176c fly, bought for 7.5 in 2k

- RXM1 175c, sold at 25 in 4k

- ERZ2 100p, bought for 3.5 in 4k

- 3RZ1 100/99.87ps vs 100.50/100.62cs, bought the ps for flat in 3k (ref 100.265)

- 3RZ1 99.87p, bought for 4 in 2.5k

- 0LU1 99.62/75/87c fly 1x3x2, sold the 3 at 1.25 in 2k

- 0LU1 99.87/100/100.12c fly, bought for 1 in 5k

- 3LU1 99.12/98.87/98.62p fly, bought for 3.25 in 5k

FOREX: GBP Skids to March Low as Inflation Disappoints

- Sterling held the session's losses throughout European and US hours after lower than expected inflation numbers out of the UK for February. CPI rose by just 0.1% m/m vs. Exp. 0.5%, with soft clothing prices largely responsible. GBP/USD took out support at the $1.37 handle, hitting new March lows in the process and narrowing the gap with key support at the 1.3619 100-dma.

- At the other end of the table, NOK traded particularly well on the oil price recovery, with WTI and Brent crude futures adding well over 5% apiece to enjoy the best session in months. The move allowed USD/NOK to undo some recent outperformance, pressuring the rate back below the 100-dma at 8.6440.

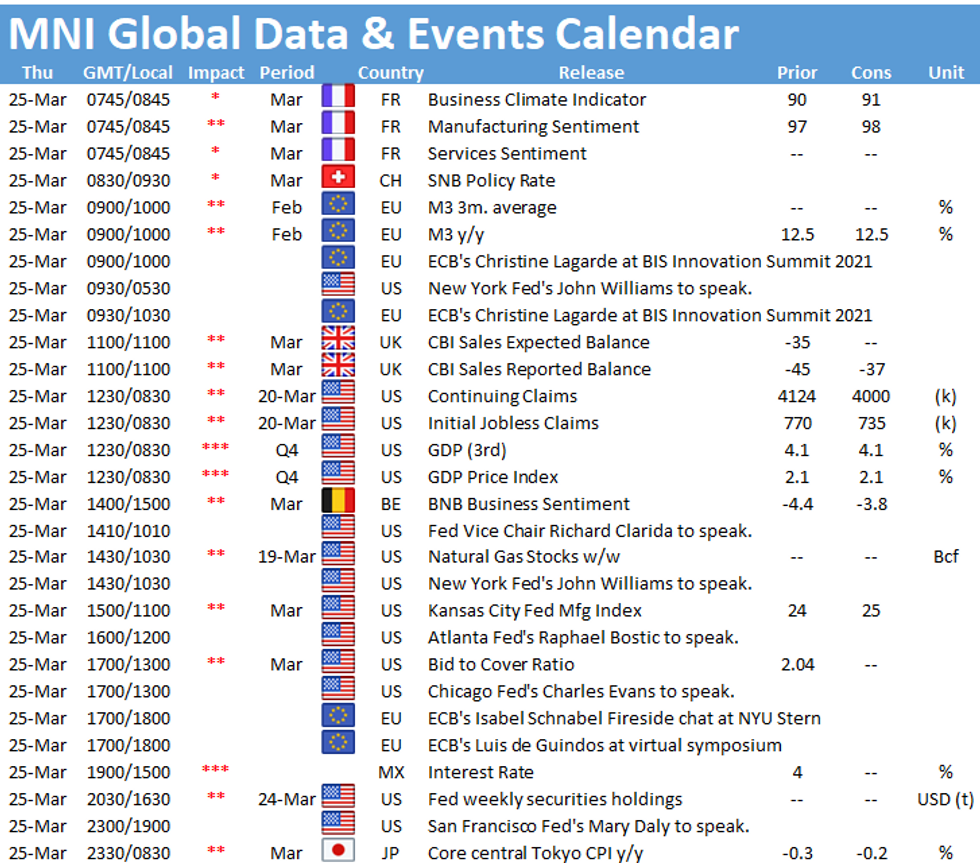

- Central banks are again a focus Thursday, with rate decisions due from the South African, Mexican and Swiss central banks.

- Data crossing Thursday includes weekly US jobless claims and tertiary Q4 GDP - neither of which will likely prove significant market movers.

FX OPTIONS: Expiries for Mar25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700-10(E1.2bln), $1.1800(E1.3bln), $1.1900(E610mln), $1.2000(E587mln)

- USD/JPY: Y106.90-107.00($1.0bln), Y108.80($530mln), Y109.25-30($1.5bln)

- EUR/GBP: Gbp0.8600(E1.1bln), Gbp0.8615-30(E1.4bln-EUR puts)

- AUD/USD: $0.7765(A$1.65bln)

- AUD/NZD: N$1.0745(A$576mln)

- USD/CNY: Cny6.30($1.1bln), Cny6.40($1.1bln)

PIPELINE: Late Issuers, London Stock Exchange Jumbo/Multi FX Chatter

- Date $MM Issuer (Priced *, Launch #)

- 03/24 $2.25B #ING $1.1B 6NC +92, $400M 6NC5 FRN SOFR+101, $750M 11NC10 +112

- 03/24 $1.85B #So-California Edison $350M 2Y +60, $400M 2Y FRN SOFR+64, $700M 3NC2 +80, 00M $3NC2 FRN SOFR+83

- 03/24 $1.4B #American Tower $700M each: 5Y +80, 10Y +110

- 03/24 $1.35B #Steris $675M each: 10Y +110, 30Y +145

- 03/24 $1.1B #Dominion Energy $500M Y +65, $500M 20Y +110

- 03/24 $650M #Mizrahi Tefahot Bank 10NC5 +225

- 03/24 $Benchmark ISDB (Islamic Development Bank) 5Y Sukuk +32

- 03/24 $Benchmark Ghana bond investor call

- On tap for Thursday:

- 03/24 $Benchmark MGM China 5.8NC2.8

- 03/25 $2B Imola Merger Corp 8NC3 investor calls

- 03/?? $Benchmark (w/EUR & GBP) London Stock Exchange multi-tranche

EQUITIES: Stocks Off Lows, But Mixed Performance

- US stock futures recovered well off the Asia-Pac session lows, with the e-mini S&P climbing well back above the 3,900 mark. Nonetheless, both Tuesday's and the week's highs are out of reach for now.

- This translated to a mixed performance in cash markets, with the S&P 500 rising around 0.5%, while tech-led NASDAQ lagged, slipping around 0.7% ahead of the close.

- US energy names led the way higher, with the surging oil price (WTI +5%) helping boost names that had suffered in recent sessions, explorers and oil services firms were among the main beneficiaries. At the other end of the index, communication services and consumer discretionary lagged. The likes of Viacom CBS fell sharply on a stock offering announcement as the company look to raise funds for streaming content.

- In Europe, Germany's DAX fell while Spain's IBEX-35 outperformed for a second session. The index closed higher by 0.6%.

COMMODITIES: Oil Prices Rebound, Entirely Reversing Yesterday's Sell-Off

- Both Brent and WTI futures rebounded on Wednesday, recovering the entirety of Tuesday's sharp sell-off. Optimism was renewed in a strong way with prices gaining just shy of 6%.

- One of the largest container ships in the world ran aground in the Suez Canal on Tuesday morning, severing a vital trade artery and threatening to disrupt global shipments for days. The Suez Canal Authority will suspend re-floating operations until Thursday because of weather concerns. Despite the fact there is plenty of spare capacity in pipelines around the Suez canal, the news bolstered sentiment and added a further tailwind for the rebound.

- Separately Reuters reported that OPEC+ oil producers at April 1 meeting likely to make similar decision to last gathering in March when they held output mostly steady, according to four Opec+ sources.

- Spot gold continued to adhere to the most recent 1725-1740 range, posting marginal 0.4% gains on the session despite a slightly stronger dollar.

- Silver consolidated towards Tuesday's lows. Yesterday's decline gathered momentum on a break of $25.39 price support which held as resistance today. Silver remains in a short-term technical bear leg with the next support residing at the March 5th low of $24.78.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.