Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Grinding Higher After ADP Miss, Tsy Refunding In-Line

Rates trading firmer after the bell, off late session highs amid moderate two-way positioning tending toward better buying after early post-ADP Chop. Tsy futures blipped off lows after ADP private employ came out lower than expected: +742k vs. +850k mean est.

- Rates reflexively sold off a few minutes later despite a largely in-line quarterly refunding annc from the US Tsy -- unchanged from the first quarter' record amount, $126B in 3s, 10s and 30s to auction next week. Tsy anticipates cutting T-bill auctions by USD150 billion in the months ahead and leaving longer-dated issuances steady, relying on its cash pile to fund the Biden administration's fiscal policies, as officials contend with uncertain debt limit deadlines to come at the end of July.

- Weakness was short lived as rates see-sawed higher by midday, finishing near session highs while equities pared gains, ESM1 near steady ahead the close. No obvious trigger or headline in play, amid decent overall volumes, TYM1 over 1.14M, that included sporadic buying in 5s and 10s from prop and fast$.

- The 2-Yr yield is down 0.4bps at 0.1546%, 5-Yr is down 1.8bps at 0.7997%, 10-Yr is down 1.2bps at 1.5801%, and 30-Yr is down 0.8bps at 2.2539%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00338 at 0.06788% (-0.00338/wk)

- 1 Month -0.00275 to 0.10563% (-0.00162/wk)

- 3 Month -0.00550 to 0.16988% (-0.00650/wk) ** (NEW Record Low vs. prior: 0.17288% on 4/22/21)

- 6 Month -0.00600 to 0.20063% (-0.00425/wk)

- 1 Year -0.00388 to 0.27900% (-0.00213/wk)

- Daily Effective Fed Funds Rate: 0.06% volume: $73B

- Daily Overnight Bank Funding Rate: 0.05% volume: $257B

- Secured Overnight Financing Rate (SOFR): 0.01%, $895B

- Broad General Collateral Rate (BGCR): 0.01%, $371B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $344B

- (rate, volume levels reflect prior session)

- Tsy 4.5Y-7Y, $6.001B accepted vs. $18.282B submission

- Next scheduled purchase

- Thu 5/06 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

US TSYS/OVERNIGHT REPO

Largely steady to prior session lvls, 10s and 30s continue to lead specials. Other current levels: T-Bills: 1M -0.0025%, 3M 0.0101%, 6M 0.0355%; Tsy General O/N Coll. 0.01%

| Duration | Current | Old Issue |

| 2Y | 0.00% | 0.00% |

| 3Y | -0.01% | -0.08% |

| 5Y | 0.00% | -0.06% |

| 7Y | -0.01% | 0.01% |

| 10Y | -0.14% | -0.10% |

| 30Y | -0.13% | -0.07% |

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +5,000 Blue Sep 90 calls, 4.0 vs. 98.52-.515

- +4,000 Green Jun 99.437/99.562 3x2 put spds, 5.25

- -5,000 Blue Jun 87 puts, 16.5 vs. 98.655/0.64%

- +15,000 Blue Jul 80/82 put spds, 4.25

- +85,000 Blue Sep 80 puts, 6.5

- -7,500 Green Dec 90 straddles, 44.0

- +4,300 Green Dec 85 puts, 8.5 vs. 98.945/0.08%, large offer

- +2,000 Blue Aug 77/80/82 3x5x2 put flys, 2.5

- +30,000 Dec 99.75/99.812/100 broken call fly, 1.75

- -2,000 Blue Sep 87/90 call spds 1.0 over 80/82 put spds

- Up to +35,000 Blue Dec 75/88 put over risk reversals, 1.0 vs. 98.31/0.38, makes some +65k since yesterday -- massive position build adding to appr +150,000 same put skew play in Blue Sep (rate hike insurance for latter half 2024)

- +5,000 Red Jun 90/92 put spds, 1.0

- +4,000 short Jul 99.687/99.75 call strips, 5.0 vs. 99.685/0.50%

- +6,000 Green May/Green Jun 99.187/99.25/99.312/99.43 call condor strip, 1.0-2.0cr

- -2,000 FVM 123.5 puts, 4

- +3,000 FVM 123/123.25 put spds, 1

- +3,000 TYN 128/129/130/131 put condors, 12

- -3,000 TYN 129.5 puts, 18

- +2,500 FVN 123.5 straddles, 59.5

- -2,500 TYN 129.5/133.5 strangles, 32-2,750 FVN 122/122.75 put spds, 8

- Overnight trade

- -20,000 wk1 TY 131.5 puts vs. +wk2 TY 131 puts, 0.0

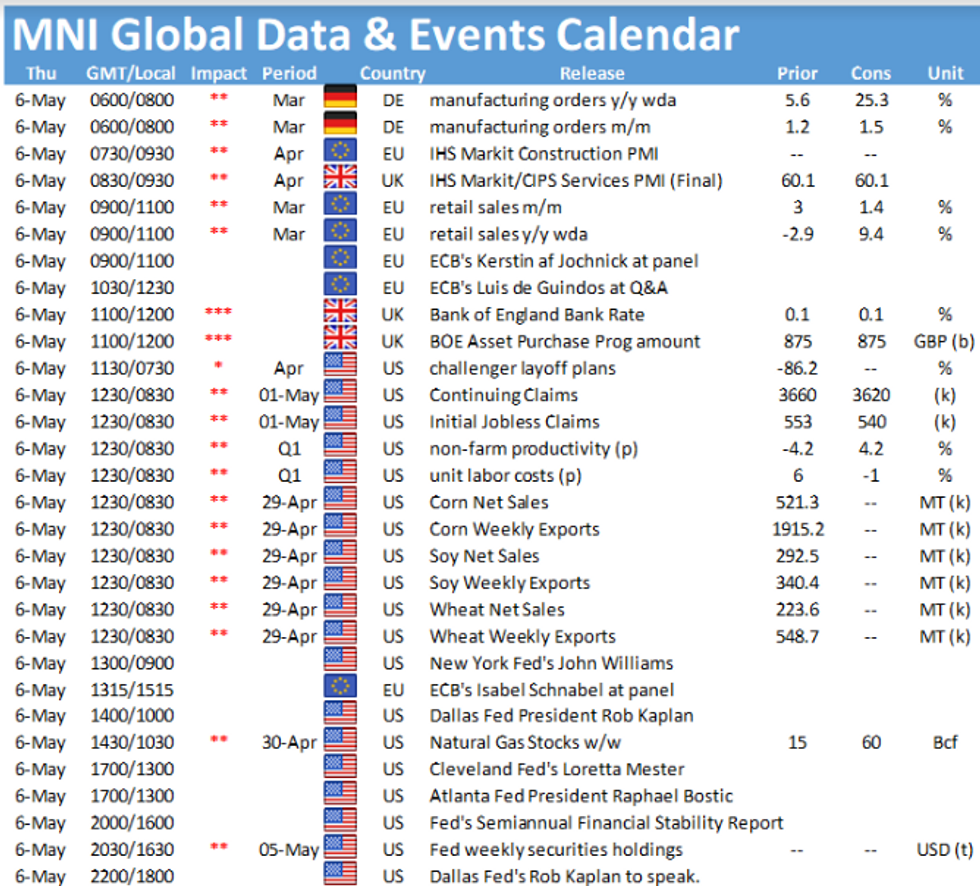

EGBs-GILTS CASH CLOSE: Gilts Underperform With BoE Ahead

Gilts and Bunds weakened Wednesday with some bear steepening.

- Periphery spreads widened, with the exception of Greece - which sold E3bln of new 5-Yr EUR benchmark via syndication; GGBs outperformed on the session as guidance tightened.

- Gilts underperformed, ahead of the BoE decision Thursday.

- Supply weighed on Gilts somewhat. In auctions, Germany allotted E3.3bn of Bobl and the UK sold combined GBP4.75bln of Jul-31 and Jan-46 Gilt.

- Data held some sway over price action, with Spanish services PMI beat and Italian miss alternatively weighing on / boosting EGBs, and later, US ISM Services missing estimates boosted core bonds.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 0.2bps at -0.695%, 5-Yr is up 0.4bps at -0.603%, 10-Yr is up 1bps at -0.228%, and 30-Yr is up 1.6bps at 0.331%.

- UK: The 2-Yr yield is up 0.7bps at 0.054%, 5-Yr is up 1bps at 0.359%, 10-Yr is up 2.4bps at 0.819%, and 30-Yr is up 3.6bps at 1.326%.

- Italian BTP spread up 2.7bps at 112.6bps/ Greek spread down 3.6bps at 120.6bps

OPTIONS/EUROPE SUMMARY: Some Vol Structures And Put Fly Buying

Wednesday's options flow included:

- ERH3 100.50^, bought for 27.5 in 1k

- 0RH2 100.37/100.50^^, bought for 11.25 in 1.5k

- 2RZ1 100.25/100ps 1x1.5 vs 3RM1 100.12/99.87ps, bought the 2yr for half in 3k

- 3RZ1 99.87/62/50 broken put fly, bought for 2.25 in 5k

- 0LM1 99.87p, vs 2LM1 99.50/99.37ps, bought the 1yr for 10.5 in 4k

- 0LU1 99.75/99.625/99.50p fly bought for 3.25 in 7.5k

- 0LU1 99.87/100cs, bought for 1 in 10k (ref 99.705, 5 del)

- 0LV1 99.625 call v 2LV1 99.50 call bought for 2.25-2.5 in 5k

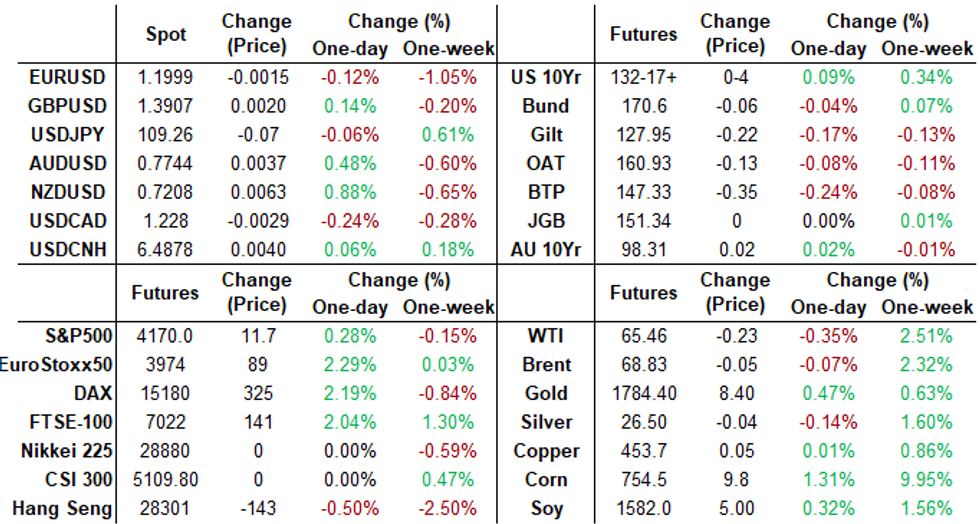

FOREX: NZD Remains Top Of The Pile, CAD hits 3-year highs

- Broad dollar indices are roughly unchanged from yesterday as ADP Employment Change and ISM Services Index numbers were unable to ignite markets on Wednesday with G10 currencies holding tight ranges.

- USDCAD reached three-year lows, matching the lowest level reached in January 2018 at 1.2251/2. The break of 1.2365, Mar 18 low confirmed a resumption of the downtrend that has been in place since March 2020. Moving average studies are also in bear mode, reinforcing current trend conditions. Focus is now on the 1.2251 low as well as 1.2239, a Fibonacci projection, with Canadian jobs data on Friday's docket.

- NZDUSD consolidated overnight gains, above the 50-day MA at 0.7141, following solid employment figures and remains 0.87% higher on the session at 0.7207.

- This dragged Aussie higher with additional impetus stemming from initially higher oil prices and a firm commodity complex.

- EURUSD spent the majority of the session either side of 1.20, however maintains a slightly offered tone and resides down 0.15% on the day at 1.1995.

- Focus now turns to the Bank of England Rate Decision and US Weekly jobless claims on Thursday before Friday's Non-farms Payrolls report.

FX OPTIONS: Expiries for May06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800-15(E525mln), $1.1850-65(E703mln), $1.1875-85(E573mln), $1.1900-05(E511mln), $1.2000-20(E1.8bln), $1.2025-35(E630mln), $1.2050-55(E737mln), $1.2100-20(E1.3bln)

- USD/JPY: Y107.00-15($1.2bln), Y107.80-00($676mln), Y108.80-00($1.0bln), Y109.60-80($1.2bln)

- GBP/USD: $1.4000(Gbp711mln)

- AUD/USD: $0.7700-20(A$705mln), $0.8000(A$1.0bln-AUD puts)

- NZD/USD: $0.7000(N$577mln)

- USD/CAD: Cny6.45($1.4bln-USD puts)

PIPELINE: $2B JP Morgan 5Y Launched

$5.7B to Price Wednesday

- Date $MM Issuer (Priced *, Launch #)

- 05/05 $2B #JP Morgan 5Y 3.65%

- 05/05 $1B #Florida Power & Light 2NC.5 FRN SOFR+25

- 05/05 $800M #Highmark $400M 5Y +68, 00M $10Y +98

- 05/05 $650M #Agree Realty $350M 7Y +90, $300M 12Y +115

- 05/05 $1.25B Vistra Operations Co 8NC3 investor call

- On tap:

- 05/06 $1B EIB 10Y +12a

- 05/06 $500M NIB 5Y FRN SOFR+20a

EQUITIES: Stocks Rebound, Dip Buyers Remain a Force

- After Tuesday's sharp pullback, equity markets were far more settled Wednesday, with all three major US indices higher headed into the close. After initial outperformance, the tech-led NASDAQ faded slightly, but remains on better footing relative to the Tuesday close.

- A quieter session for stocks weighed on the VIX, which retreated the entirety of the Tuesday move higher to head toward the week's lowest levels.

- The energy sector traded well in the US, with oil and exploration firms taking heed from the much firmer WTI crude futures curve. Materials and financials also saw strength while utilities and real estate suffered.

- Across Europe, markets traded particularly well, with Germany's DAX closing with gains of over 2%, while UK, Spanish and Italian indices were higher by well over 1.5% apiece.

COMMODITIES: Energy Complex Solid, But Demand Spotty

- WTI and Brent crude futures firmed for a third session Wednesday, as markets continue to price in the growing likelihood of an economic recovery in the latter half of 2021. Markets boost futures prices across the curve Wednesday, with all contacts out to Jul-25 now north of $54/bbl.

- Saudi Arabia's official selling prices showed further inconsistency of demand, however, with oil headed to the US seeing prices tick higher, while crude headed to Europe and Asia had prices cut.

- Weekly DoE numbers were further supportive for prices, showing an expectedly large draw of close to 8mln bbls, while refinery utilization ticked higher by 1.1%.

- Gold shrugged off early losses, while silver continues to lag. This corrects the pressure seen in the gold/silver ratio throughout April and in the early few sessions of May.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok