Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Curves Crater, Reflation Trade Reversed

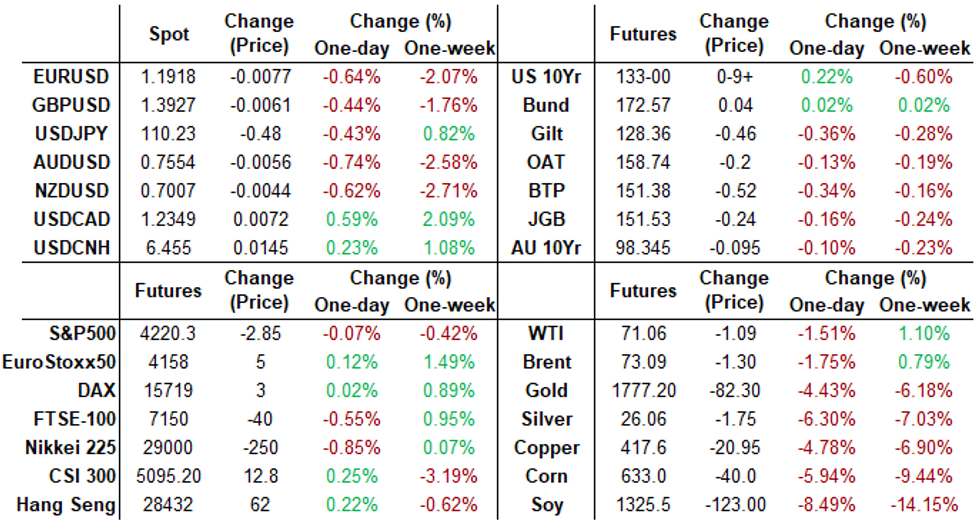

Post-FOMC: Reflation unwinds, slow to get underway but inexorable bull curve flattening into the second half. Little post-claims chop as Bonds started climb higher after weekly claims climb (+37k to 412K vs. +360k exp), continuing claims +3.518M vs. +3.425M exp.- Thu's bull flattening largely result of Wed's FOMC, upping DOTS to pencil in two rate hikes by late 2023. Some technical buying while shorts caught wrong-footed, forced to unwind, exacerbating the move. Long end Tsy Bonds clawed higher, 30YY fell to 2.0468% low (mid-Feb level), 10YY around 1.5% after slipping to 1.4702% low -- stable by comparison.

- Aside from tight stops getting triggered on the rally in long end, curve steepener unwinds contributed: TD Securities reports they are taking off a 5s30s steepener as well as 9Y TIPS BE position. TD explained "reflation trades suffered a significant setback after the Fed delivered a hawkish message at the June FOMC — raising the 2023 dots, upgrading the SEP, and sending a message that tapering discussions had begun. This more hawkish message has led to a significant paring of reflation trades, with short covering exacerbating the moves.

- TD added the "initial curve steepening was driven by a selloff in the 5y sector as the market pulled forward tapering and hike expectations. However, the flattening has been replaced by short-covering buying, exacerbating the move."

- The 2-Yr yield is up 0.6bps at 0.2113%, 5-Yr is down 2.1bps at 0.8744%, 10-Yr is down 6.6bps at 1.5091%, and 30-Yr is down 10.9bps at 2.0982%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00775 at 0.06325% (+0.00788/wk)

- 1 Month +0.01088 to 0.09338% (+0.02050/wk)

- 3 Month +0.01000 to 0.13450% (+0.01562/wk) ** (New Record Low: 0.11800% on 6/14)

- 6 Month +0.00675 to 0.15863% (+0.00612/wk)

- 1 Year +0.01063 to 0.24513% (+0.00575/wk)

- Daily Effective Fed Funds Rate: 0.06% volume: $62B

- Daily Overnight Bank Funding Rate: 0.04% volume: $242B

- Secured Overnight Financing Rate (SOFR): 0.01%, $900B

- Broad General Collateral Rate (BGCR): 0.01%, $375B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $352B

- (rate, volume levels reflect prior session)

- Tsys 22.5Y-30Y, $2.001B accepted vs. $4.419B submission

- Next scheduled purchase:

- Fri 6/18 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +10,000 Blue Sep 87/91 call spds, 5.5 vs. 98.53

- +20,000 Gold Dec 70/73/75 put flys, 4.25

- -3,000 short Sep 95/96 put spds, 3.0

- -10,000 Blue Dec 75/88 call over risk reversals, 0.5 vs. 98.36/0.27%

- over +5,000 Sep 99.81/99.87 1x2 call spds

- +3,500 Mar 100.12 calls, 0.5

- +2,500 Green Mar 87 straddles, 49.0

- Overnight trade

- 4,000 Sep 99.75/99.81/99.87 call flys

- 10,000 short Sep 99.312 puts, 1.0

- 3,000 short Jul 96 puts, 2.0

- 5,000 Green Dec 87/88/91/92 iron condor

- 2,000 Blue Sep 80/82/83/85 put condors

- +5,000 Blue Sep 80/82 put spds, 4.5

- +10,000 Blue Sep 87 calls 5.5-6.0, 5k Blocked 6.0

- 1,500 Blue Jul 83/85/86 put flys

- -6,000 Blue Sep 90 calls, 1.5

- +2,500 USQ 167 calls, 7

- -5,700 TYU 129.5/134 strangles, 34

- +3,000 FVU 122 puts, 12.5

- +20,000 TYQ 131.5 puts at 44 vs. 131-16.5/0.45% traded post-data

- Block, +10,000 TYQ 131.5 straddles, 1-27 at 0829:55ET

- -11,000 FVN 123 calls, 22.5-21.5

- Overnight trade

- +13,000 TYN 133.5 calls, 1

- +6,000 TYN 130.25/130.75/131.25/131.75 put condors, 11

- -5,000 wk3 132/133 put spds, 60

- -4,000 FVQ 123.25/123.5 strangles, 41

- +4,000 FVU 121.25 puts, 6 vs. 123-11.5/0.10%

FOREX: Greenback and JPY Firmer As Risk Sentiment Wanes

- The dollar index edged consistently higher throughout Thursday's session, extending the post-fed renewed optimism for the greenback. The advance was aided by a sharp move lower in precious and industrial metals as well as oil finally ending it's winning streak.

- Gains were broad based as EUR, GBP, AUD, NZD, CAD and CHF all retreated between 0.6-1%.

- EURUSD continued to fall sharply, taking out multiple short term supports to fall 2% from yesterday's highs, finally pausing for breath at a noted support of 1.1893, 2.0% 10-dma envelope.

- The standout performer against the dollar was the resilient Japanese Yen as the reversal in US yields and the initial drop in equity indices soured risk sentiment. Additionally, strong resistance headed into the March high of 110.97 also slowed down proceedings following the overnight rally.

- JPY strength and softer risk led to some sizeable declines in cross-JPY. AUDJPY, CADJPY and EURJPY the notable movers, all shedding over 1% for Thursday as of writing and unable to bounce despite a late recovery in US indices

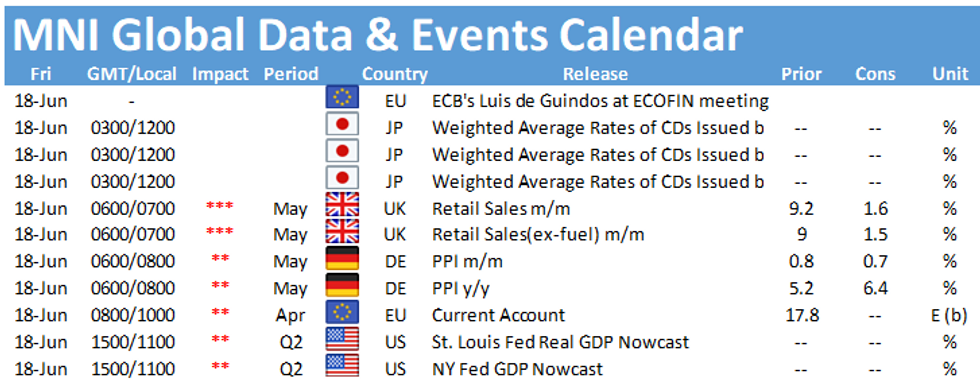

- These moves come ahead of the Bank of Japan due overnight. The June meeting should ultimately prove to be a very bland affair, with no changes in monetary policy expected. There are also no expectations for tweaks to the Bank's overarching economic view and forward guidance, as it continues to fight the well-documented disinflationary forces in play in Japan. UK Retail Sales rounds off the week's data calendar.

FOREX: Expiries for Jun18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1940-50(E1.5bln), $1.2000(E647mln), $1.2065-75(E1.2bln-EUR puts), $1.2100-10(E3.8bln,E3.2bln of EUR puts), $1.2150(E500mln), $1.2170-80(E1.1bln-EUR puts)

- USD/JPY: Y109.25($560mln), Y109.50($625mln), Y110.00($896mln)

- AUD/USD: $0.7700(A$546mln)

- USD/CAD: C$1.2160($1.6bln-USD puts), C$1.2200($1.5bln-USD puts), C$1.2225($1.1bln)

- USD/CNY: Cny6.40($565mln), Cny6.41($575mln)

PIPELINE: $1B Kenya 2034-Bond Launched

- Date $MM Issuer (Priced *, Launch #)

- 06/17 $1B #Kenya 2034 Bond 6.3%

- 06/17 $800M GXO Logistics 5Y +85a, 10Y +120a

- 06/17 $750M #Eagle Materials 10Y +110

- 06/17 $600M #Sun Communities 10Y +125

COMMODITIES: Oil Snaps Winning Streak as Iran Makes Progress on Nuclear Deal

- The extended winning streak in WTI crude futures waned Thursday, with oil closing lower and snapping an impressive 15-session streak of higher highs (a record for that contract). WTI and Brent crude future erased recent strength as markets eyed further optimism from Iranian negotiators, with reports from Tehran stating that the nuclear deal is closer than ever before, despite some fundamental issues remaining.

- While the IAEA stated that upcoming Iranian elections will not impact any deal, markets seem less certain, with the weekend's poll likely a focus for energy markets.

- Precious metals suffered throughout the Thursday session - both gold and silver traded well into negative territory with gold comfortably taking out the $1800/oz support as well as $1796.8 - the 50% retracement of the Mar 8 - Jun1 rally.

- This confirms the bearish cycle and prompts markets to look lower at the$1768.50 61.8% retracement of the Mar 8 - Jun 1 rally and the Apr 29 low of $1756.2.

EQUITIES: Soft Energy Drags S&P, Dow Lower

- US indices were mixed Thursday, with the tech-led NASDAQ the outperformer thanks to solid rallies in the likes of NVIDIA, AMD and PayPal. Countering the strength in tech, poor turnouts from energy, materials and financials dragged the likes of the S&P500 and Dow Jones into negative territory ahead of the close.

- Energy names were the poorest performers on Thursday, with the likes of Devon Energy, Marathon Oil and Occidental Petroleum all slipping 4% or more as the WTI crude futures price edged off the recent cycle high of $72.99/bbl. Materials and financials were also among the sectors contributing to the downtick in headline indices.

- The VIX opened higher, still seeing some support after the hawkish Fed decision Wednesday, but these gains faded throughout the cash session, keeping the index within range of the post-pandemic lows posted last week.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok