Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI ASIA MARKETS ANALYSIS - TSYS Hold Near the Highs of the Day

FIXED INCOME: Grinding Higher

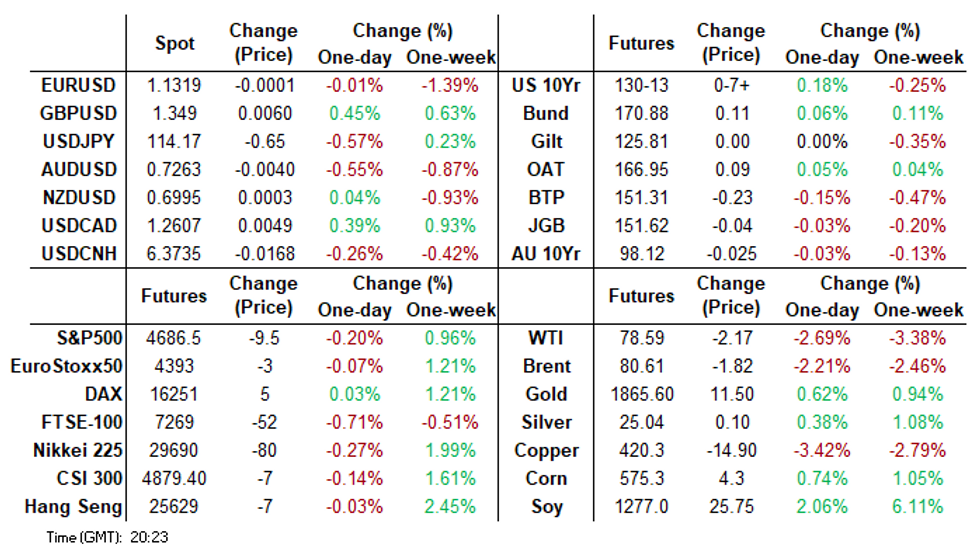

US TSYS have firmed during the day with the belly of the curve marginally outperforming.

- Cash yields are 2-4bp lower on the day with the curve slightly bull flattening.

- TYZ1 is holding near the highs of the day and last traded at 130-14+ (L: 130-01+ / H: 130-16+)

- Today's 20Y auction had a a high yield of 2.065% and bid-to-cover ratio of 2.34x

- The White House earlier indicated that President Biden will likely make a decision on the Fed Chair before Thanksgiving.

- The data slate was light today with mortgage applications and housing starts not giving much for the market digest.

- Focus tomorrow will shift to jobless claims, and the Philly Fed index.

US TSY 20Y BOND AUCTION: HIGH YLD 2.065%; ALLOT 78.36%

- US TSY 20Y BOND AUCTION: HIGH YLD 2.065%; ALLOT 78.36%

- US TSY 20Y BOND AUCTION: DEALERS TAKE 20.44% OF COMPETITIVES

- US TSY 20Y BOND AUCTION: DIRECTS TAKE 19.38% OF COMPETITIVES

- US TSY 20Y BOND AUCTION: INDIRECTS TAKE 60.18% OF COMPETITIVES

- US TSY 20Y BOND AUCTION: BID/COV 2.34

US TSY 119D AUCTION: HIGH RATE 0.055%; 49.68% AT HIGH

- US TSY 119D AUCTION: HIGH RATE 0.055%; 49.68% AT HIGH

- US TSY 119D BILL AUCTION: DEALERS TAKE 49.67% OF COMPETITIVES

- US TSY 119D BILL AUCTION: DIRECTS TAKE 8.49% OF COMPETITIVES

- US TSY 119D BILL AUCTION: INDIRECTS TAKE 41.84% OF COMPETITIVES

- US TSY 119D AUCTION: BID/COVER 3.11

US TSY 22D AUCTION: HIGH RATE 0.130%; 50.50% AT HIGH

- US TSY 22D AUCTION: HIGH RATE 0.130%; 50.50% AT HIGH

- US TSY 22D BILL AUCTION: DEALERS TAKE 60.36% OF COMPETITIVES

- US TSY 22D BILL AUCTION: DIRECTS TAKE 14.08% OF COMPETITIVES

- US TSY 22D BILL AUCTION: INDIRECTS TAKE 25.57% OF COMPETITIVES

- US TSY 22D AUCTION: BID/COVER 2.65

FOREX: USDJPY Strongly Rejects 115, GBP Buoyed By CPI Data

- USDJPY experienced strong volatility on Wednesday as failed momentum above the crucial 114.70 inflection point sparked a strong reversal throughout the US trading session.

- Falling just 3 pips shy of the 115.00 mark overnight, the pair edged back below the breakout throughout European trade. With the path of least resistance defined as lower, USDJPY weakening gathered pace with the pair trading back below 114.00 amid a degree of pressure in global equity indices.

- AUD remained the weakest currency in the G10 space, extending the November downtrend below the 0.73 handle in AUDUSD with AUDJPY retreating well over 1%. The price action was largely in response to wage index data overnight, which showed pay growth well shy of the RBA's cited 3% requirement for rate hikes.

- GBP traded on a surer footing, boosted by the above estimate CPI readings released early on Wednesday. Sterling gains were broad based with cable rising close to 1.35 and the cross slipping to the lowest levels since February 2020, back below 0.8400. This has opened 0.8356 next, the Feb 26, 2020 low. Initial resistance is seen at 0.8463.

- In emerging markets, continued weakness in the Turkish lira remains the standout talking point ahead of tomorrow's central bank decision. USDTRY reached +3% gains for the second day in a row, briefly printing a high of 10.6848 before consolidating around 10.60 heading into the close.

- New Zealand inflation expectations data scheduled overnight as well as potential comments from RBA Assist. Governor Ellis speaking at an online event. US jobless claims and Philly Fed Manufacturing Index headline the US docket before potential commentary from Fed members Williams, Evans and Daly.

FX OPTIONS: Expiries for Nov18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1290(E552mln), $1.1330-50(E646mln), $1.1450-60(E941mln)

- USD/JPY: Y113.90-05($1.4bln), Y114.20-25($1.3bln), Y114.50-55($521mln), Y115.00($510mln)

- GBP/USD: $1.3400(Gbp896mln)

- EUR/GBP: Gbp0.8400(E1.1bln), Gbp0.8450-60(E1.1bln)

- USD/CAD: C$1.2330($1.3bln), C$1.2380($770mln), C$1.2500($1.0bln)

- USD/CNY: Cny6.3830($1bln)

EQUITIES: Risk Appetite Wanes as IPO Darlings Falter

- Headline indices traded lower Wednesday, with the S&P, Dow Jones and NASDAQ all in minor negative territory as stocks of companies that had surged on recent IPOs ran out of stream and traded lower. Most notably Rivian, one of the biggest IPOs of recent years, slipped around 15% as markets retraced a minority of the 130% rally seen since last week's listing.

- Elsewhere, card issuers and payment firms traded similarly poorly following Amazon's decision to end the acceptance of Visa credit cards on their website due to the high fee structure. Shares were marked lower, with Visa off over 5% as traders speculated that either Visa lose out on Amazon's business, or are forced to blink and revise their pricing.

- The e-mini S&P traded wholly inside the Tuesday range, keeping technical parameters intact. 4717 remains the upside target should prices recover through the alltime highs. This level marks the 1.50 proj of Jul 19 - Aug 16 - Aug 19 price swing, with 4615.28, the 20-day EMA, as first support.

COMMODITIES: Oil Slips as Xi & Biden Take Dim View of High Energy Prices

- WTI and Brent crude futures head into the close in negative territory, with both benchmarks shedding around 2% apiece. The WTI-Brent widened marginally, with markets focusing on the supply outlook and potential action from the White House on high fuel costs.

- While prices were briefly supported by weekly DoE data showing a draw of 2.1mln bbls vs. Exp. build of 1mln, pressure built into the close as focus turned to data showing the US SPR shed 3.25mln bbls across the week. While this doesn't equate to a reserve release from the US SPR (these adjustments are usually technical in nature), that's the largest draw on reserves according to data going back over a decade.

- Elsewhere, markets continue to speculate over the likelihood of coordinated action on energy supply from both the US and Chinese Presidents, with wires confirming the two leaders discussed their views on energy, although no decisions were made on the issue.

- Resultingly the WTI futures curve flattened slightly, with the most notable pressure seen in the front month contracts. The Dec-21 future slipped to $78.81, but managed to steer clear of first support at $78.37, the 50-day EMA.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok