Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Late Rate Rally, Risk-Off as Omicron Comes to US

Rates rebounded early in second half, finish session on highs after the first Omicron-Covid variant reported in US (California, from individual that was fully vaccinated). Geopol concerns over Russia/Ukraine and China/Taiwan tensions likely adding to the renewed risk-off tone. Risk assets tumbled late (ESZ1 -57.0; WTI -95.0).

- Tsys held weaker levels for much of the first half, in-line ADP employment (+534K vs. Exp. +525k) largely ignored, started to rebound after Fed Chairman Powell comments largely echoed Tue's hawkish tone until: "Taper need not be disruptive event in markets" spurred some sell unwinds. Trading desks reported decent real$ buying in 2s, 20s and 30s, better deal-tied rate-locks in 10s and 30s in the first half.

- Tsy futures traded steady (10s) to mixed, curves flatter after first Omicron variant reported in California. Noted buyers earlier in the session, trading desks report real$ selling 30s with leveraged$ accts, central bank selling 20s helping keep rates relatively in line. Large Block buys well through offers late in 30Y, 10- and 30Y ultra-bonds.

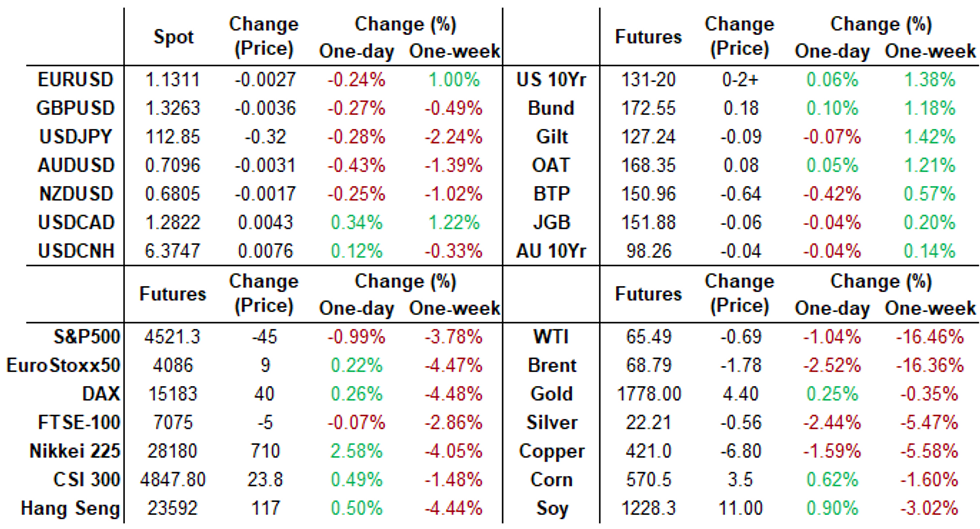

- The 2-Yr yield is down 0.6bps at 0.5592%, 5-Yr is down 1.8bps at 1.1419%, 10-Yr is down 2.9bps at 1.4155%, and 30-Yr is down 3.3bps at 1.7578%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00063 at 0.07713% (+0.00300/wk)

- 1 Month +0.00863 to 0.10263% (+0.01275/wk)

- 3 Month +0.00138 to 0.17463% (-0.00075/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00625 to 0.24950% (+0.00350/wk)

- 1 Year +0.07587 to 0.45825% (+0.04787/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $77B

- Daily Overnight Bank Funding Rate: 0.07% volume: $220B

- Secured Overnight Financing Rate (SOFR): 0.05%, $1,067B

- Broad General Collateral Rate (BGCR): 0.05%, $362B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $334B

- (rate, volume levels reflect prior session)

- Tsy 4.5Y-7Y, $5.251B accepted vs. $15.925B submission

- Next scheduled purchases

- Thu 12/02 1010-1030ET: TIPS 7.5Y-30Y, appr $1.075B

- Fri 12/03 1100-1120ET: Tsy 10Y-22.5Y, appr $1.425B

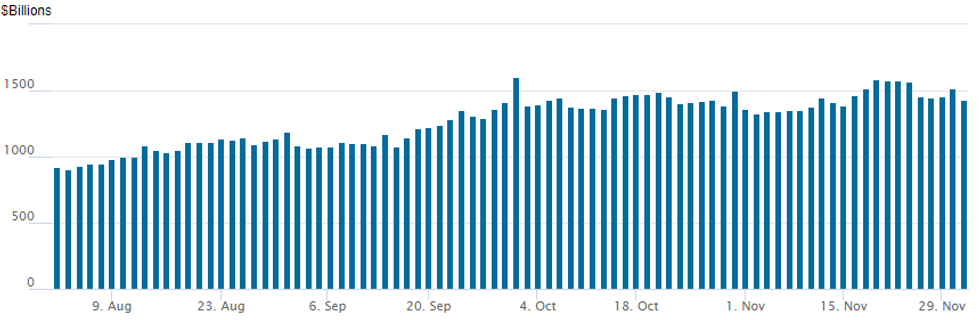

FED Reverse Repo Operation

NY Federal Reserve

NY Fed reverse repo usage recedes to $1,427.347B from 75 counterparties vs. $1,517.956B on Tuesday. Record high remains at 1,604.881B from Thursday, September 30.

US TSYS: Tactical Plays For Potential Accelerated Taper

TD Securities strategists said they are going short 10Y real rates and adding to long 2Y TIPS BEs in the aftermath of Fed Chair Powell's willingness to discuss faster tapering at the Dec FOMC and "time to retire 'transitory'" comments yesterday.- TD anticipates the Fed "will indeed accelerate tapering to give themselves the flexibility to hike as soon as Mar 2022."

- An earlier end to QE and potential faster hikes should move long end real rates higher. There is also a supply effect of tapering as markets will need to absorb more TIPS supply (net supply at $52bn in 2022 vs. -$20bn in 2021), and we go short 10y real rates to position for faster tapering.

- We don't believe the market's low terminal rate pricing (which assumes a policy mistake) and expect real rate term premium to rise. The trade carries negatively at -7.2bp to Jan 1, 2022.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options- +15,000 Red Dec'22 99.75 calls, 4.0

- -10,000 Green Dec 98.56 calls, 2.5

- +5,000 Jun 99.12/99.25/99.50 put trees, 2.5

- +10,000 short Mar 97.93/98.37 put spds 1.5 over Blue Mar 97.62/97.87 put spds, bear flattener

- +15,000 Jun 98.50/99.00 2x1 put spds, 1.0

- -5,000 Jun 99.00 puts, 4.0

- +5,000 Red Dec 98.75/99.00/99.25/99.50 put condors vs. 97.75 puts, 0.5 net debit package

- Overnight trade

- +16,000 Dec 99.81 calls, 1.0

- +5,000 short Dec 99.25/99.31 call strip, 2.0

- +6,000 short Jan 98.62/98.68 put strip, 23.0 vs. 98.775/0.77%

- -20,000 Green Dec 98.37 calls, 6.5

- +9,500 Apr 99.00 puts, 2.5

- +8,000 Dec 99.68/99.75/99.81/99.87 call condors, 5.25

- 5,000 Green Dec 98.18 puts, 3.0

- 7,300 Green Dec 98.37 calls, 6.5

- 4,000 short Jan 98.37/98.50/98.62/98.75 put condors

- -6,600 TYF 129/132 strangles, 22

- 5,000 TYF 129.5/130 3x2 put spds, 8 net

- 20,400 FVF 120.5/121 put spds, 12.5

- 15,000 TYF 129.5/130 3x2 put spds, 0.0

- Overnight trade

- +5,000 TYF 132.5/133.5 call spds, 3

- +3,500 TYF 128.75/129.5 2x1 put spds, 0.0

EGBs-GILTS CASH CLOSE: Bear Flattening, Though Greece Impresses

European FI ended Wednesday largely weaker, though off worst levels seen early in the session, with short-end/belly yields underperforming in tandem with rising U.S. rate hike expectations.

- Bunds and Gilts bear flattened, with the UK underperforming.

- A Reuters sources report that some ECB governors advocate delaying decisions on stimulus plans beyond the Dec 16 meeting a little after midday GMT saw eurozone FI strengthen; Greek bonds easily outperformed on the session following this report.

- We saw further gains into the cash close as headlines crossed that Chancellor Merkel proposing lockdowns for unvaccinated Germans.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.4bps at -0.713%, 5-Yr is up 2.2bps at -0.596%, 10-Yr is up 0.4bps at -0.345%, and 30-Yr is up 0.6bps at -0.052%.

- UK: The 2-Yr yield is up 4.3bps at 0.527%, 5-Yr is up 3.3bps at 0.653%, 10-Yr is up 0.9bps at 0.818%, and 30-Yr is up 3.2bps at 0.885%.

- Italian BTP spread up 3.7bps at 135.5bps / Greek down 5.2bps at 156.1bps

EGB Options: Mainly Downside Wednesday

Wednesday's Europe rates / bond options flow included:

- OEF2 133.5/134.75 RR, bought the put for 10 in 2.4k

- DUH2 112.20/112.00/111.80p fly, bought for 4.25 in 2.5k

- 2RM2 99.87/99.75ps vs 100.25/100.37cs, bought the ps for flat in 2k

FOREX: JPY Trades Firmly As Sentiment Dampens, Greenback Rallies Back To Unchanged

- Growth proxies and commodity-tied FX initially outperformed on Wednesday. However, as both equities and commodities reversed course throughout the US session, the US dollar/haven FX rallied and risk-tied currencies retraced lower.

- The Japanese Yen topped the G10 leaderboard, rising 0.35% against the greenback with greater gains evident on the crosses. USDJPY short-term bearish technical threat remains in place. Tuesday's weakness saw prices test and show below key short-term support at 112.73, Nov 9 low before prices improved ahead of the close. A clear break would open 112.08 next, a recent breakout level.

- One of the sharpest reversals was in USDCAD, bouncing just under 1% from lows of 1.2714 to around 1.2830. A strengthening of the current bullish theme signals scope for strength towards 1.2896 next, the Sep 20 high.

- Despite the early dollar weakness, price action has been supportive throughout the latter half of the session with broad dollar indices trading on the front foot and into positive territory as of writing.

- Back in the spotlight in emerging markets was the Turkish lira, which sharply rallied as the Turkish central bank intervened in the market. This comes following the Presidents unwavering rhetoric towards lowering interest rates. The Turkish monetary authority said that they intervened in markets by selling foreign currencies for the first time in seven years. After the colossal move from 13.88 down to 12.42, the pair consolidated within a 13.00-13.40 range for the rest of the session, currently down 1.8% on the day.

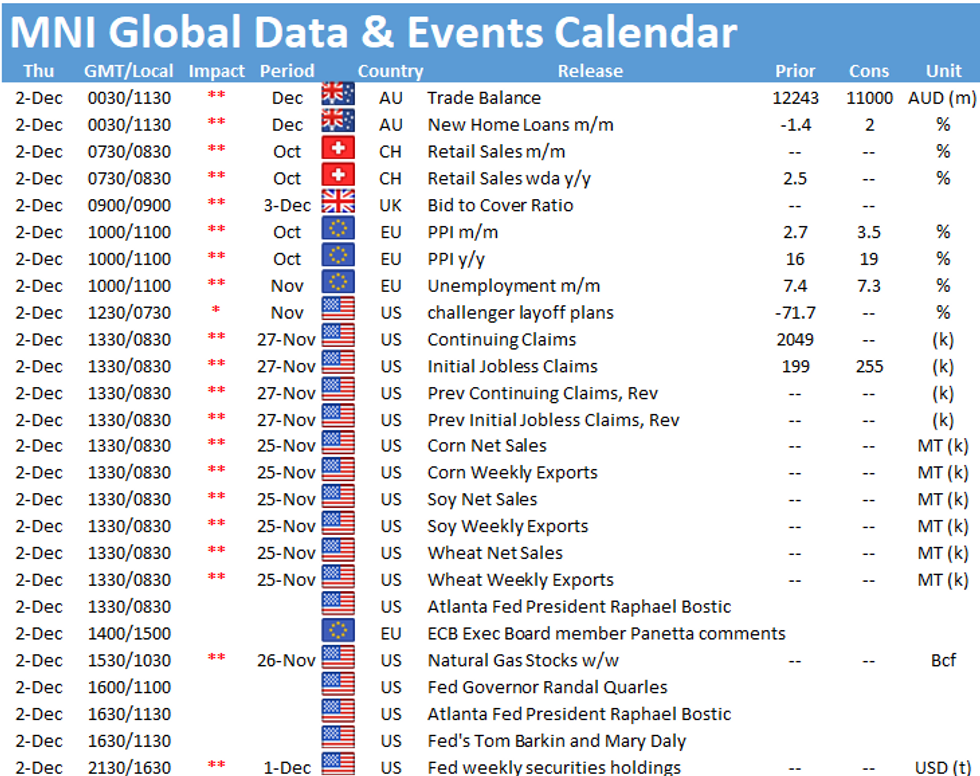

- Australian retail sales and trade balance data due overnight before European unemployment figures. US unemployment claims also due with a number of potential Fed speakers listed as we approach the FOMC blackout. The markets focus will be on Friday’s release of US non-farm payrolls.

FX: Expiries for Dec02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1275-85(E641mln), $1.1375-90(E589mln), $1.1415-25(E1.2bln), $1.1445-50(E1.1bln)

- USD/JPY: Y112.25($522mln), Y112.50($515mln), Y113.60-70($1.2bln), Y113.85-00($1.4bln), Y115.00($1.4bln)

- GBP/USD: $1.3300(Gbp851mln)

- AUD/USD: $0.7280-90(A$708mln)

EQUTIES: Stocks Extend Recovery Off Tuesday Low

- Equity markets continued their recovery off the Tuesday lows well after Wednesday's London close, with the e-mini S&P rallying to just shy of first resistance at 4667.50 / 4669.75.

- All sectors traded in the green Wednesday, led higher by energy as oil & gas producers were buoyed by a rebound across both WTI and Brent crude futures. Financials also traded well, with firm gains seen across diversified banks despite a further flattening of the US yield curve. Nonetheless, most banks remain below the week's best levels printed at the Monday open.

- S&P E-minis remain vulnerable following last week's sharp sell-off and yesterday's weakness. Attention is on the 50-day EMA at 4567.21. This average has in the past proved to be a reliable support and represents a key pivot level.

- European indices outperformed, with particular strength in the EuroStoxx50, which added just shy of 3% in a session led by blue chip German names including Siemens, Daimler, BMW and Volkswagen.

COMMODITIES: Oil Recovers But Still Heavily Down On Pre-Omicron Prices

- Oil has softened in recent trading to leave it up 2% on the day but still down more than 13% from pre-Omicron levels.

- It had been up 5% intraday before headlines on OPEC+ seeing a worsening oil surplus through Jan-Mar, DOE inventories and a more general mild risk-off backdrop.

- DOE inventories were in line at a headline level but there were significant builds across both gasoline and distillates.

- WTI is up 2% at $67.5 with a reasonably wide corridor to run in with initial firm resistance seen at $74.76 (Nov 22 low) and support focus on $64.39 (Aug 24 low).

- Brent is up 2.1% at $70.7 with a similar corridor: initial firm resistance at $74.35 (Nov 30 high) and the next significant support at $66.67 (Aug 24 low).

- Focus is on tomorrow's OPEC+ ministerial meeting and whether it goes ahead with previously planned output hikes. Biden is also due to unveil a strategy for dealing with the Omicron variant.

- Gold prices have firmed 0.6% to $1785.7. It remains bearish with scope for a clear breach of 20 and 50-day EMAs and attention on the base of the channel at $1759.6, drawn off the Aug 89 low.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.