Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI Fed's Bullard: Job Market To Stay Strong Amid Hikes

- MNI Fed’s Bullard: Market Turmoil Won't Deter Hikes

- FED'S BULLARD: IMPERATIVE WE AVOID A 1970S INFLATION SCENARIO, Bbg

Key links: MNI: SNB Could Be Forced Into Intra-Meeting Hike / MNI: Commission Favours More Time To Cut Debt- EU Officials

US TSYS: Still Reacting to the BoE Tax Cut/Gilt Buy Program Scheme

Tsys weaker after the bell, well off late overnight lows to near middle of the session range, focus largely remained on the BoE and aftermath of last week's abrupt tax cut annc that spurred Wed's long end Gilt buy program.

- On the open, FI mkts had scaled back decent portion of Wed's BOE buy program-tied rally w/ PM Liz Truss continued defense of the mini-budget on BBC radio, strong regional German CPI overnight adding to moves. Second round of BoE Gilt purchases underutilized: GBP1.415bln of long-dated gilts. Rejects GBP442.8mln offers. Take-up higher than Wed - but still relatively low, GB2.5B of 10B thus far.

- Still working out the kinks, PM Truss on regional BBC TV: BEST TO START TODAY ON GOVERNMENT'S FISCAL PLANS as WE"RE IN A VERY SERIOUS SITUATION.

- Little reaction to Fed speakers on the day, Bullard: "This is probably a good time to get inflation under control while the labor market is doing so well." Weekly claims lower than exp (193k vs. 215k; continuing claims 1.347M vs. 1.385M est), GDP slightly higher at 9.0% vs. 8.9% est.

- On tap Friday: Personal Income/Spending, Chicago PMI, UofM Sentiment and more Fed-speakers: Barkin, Brainard, Bowman and Williams.

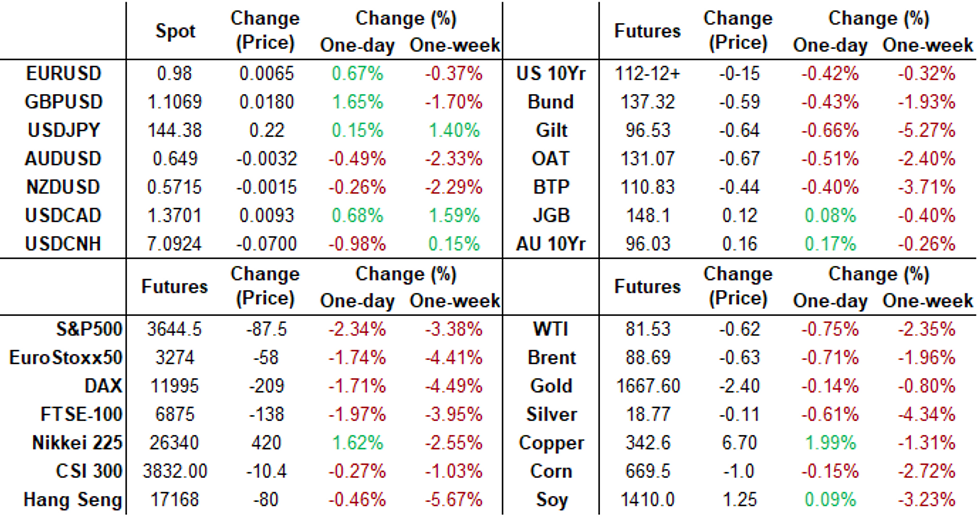

- Currently, the 2-Yr yield is up 3.3bps at 4.1678%, 5-Yr is up 3.8bps at 3.9859%, 10-Yr is up 2.2bps at 3.7534%, and 30-Yr is down 0.1bps at 3.6981%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00300 to 3.06400% (-0.00843/wk)

- 1M +0.01257 to 3.12786% (+0.03757/wk)

- 3M +0.06872 to 3.74286% (+0.11443/wk) * / **

- 6M +0.03943 to 4.20929% (+0.00800/wk)

- 12M +0.01129 to 4.78729% (-0.04757/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 3.74286% on 9/29/22

- Daily Effective Fed Funds Rate: 3.08% volume: $110B

- Daily Overnight Bank Funding Rate: 3.07% volume: $272B

- Secured Overnight Financing Rate (SOFR): 2.98%, $911B

- Broad General Collateral Rate (BGCR): 2.98%, $359B

- Tri-Party General Collateral Rate (TGCR): 2.98%, $338B

- (rate, volume levels reflect prior session)

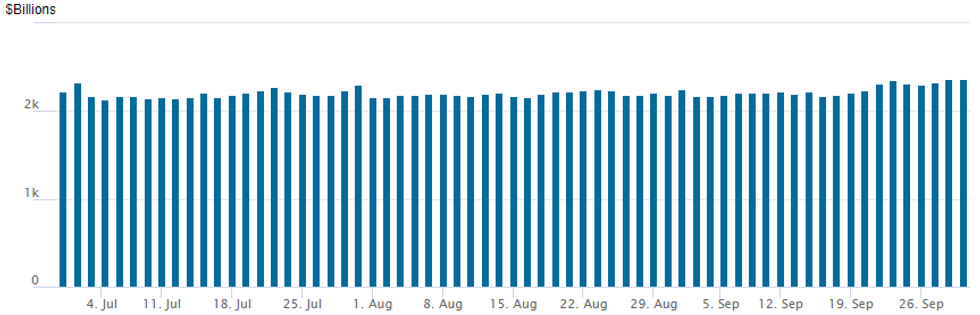

FED Reverse Repo Operation: Second Consecutive New High

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to new record high of $2,371.763B w/ 103 counterparties vs. $2,366.798B record in the prior session. Surpasses last week's record high of $2,359.227B marked Thursday, September 22.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Session trade rotating around significant vol sales in short end SOFR options (Mar'23 strangles) and varied upside call and call spd buying in Tsy options. Interpretation: option accts seeing appr 50% retrace in underlying futures from Wed's post-BoE buy program-tied rally as new support, at least in the near term, with call buyers looking for gradual drift higher through early 2023 as market vol cools.- SOFR Options:

- Block, 30,000 SFRZ2 95.37/95.62/95.87 call flys, 7.0 ref 95.74

- Block, 28,000 long Green Dec (SFRZ4) 93.50/94.00/94.50 put flys, 2.5

- -4,000 SFRZ2 95.68 straddles, 38.5

- Block, 4,000 SFRX2 95.75/96.00 1x2 cal spds, 0.75 net

- Block, -10,000 SFRH3 94.75/95.75 strangles, 38.0 ref 95.545

- Block, total 15,000 SFRV2 95.93 calls 0.5-0.75 over SFRX2 96.12/96.50 call spds

- 1,750 SFRZ2 95.56/95.68 put spds vs. 95.93/96.06 call spds

- Eurodollar Options:

- 10,000 Dec 98.62/98.75 put spds, parity

- Treasury Options:

- 1,000 TYX2 110.25/111.75 2x1 put spds, 5

- 2,100 TYZ2 118/119 call spds, 4

- 5,500 TYZ2 113.5 puts, 231 ref 112-00

- Block, 10,000 TYX2 112.5/113.5 call spds, 23 ref 112-00, adds to earlier Block and screen

- Block, 8,000 TYX2 110.5 puts, 36 ref 112-03

- 4,700 TYX2 110.5 puts, 47 ref 111-31

- 1,700 TUX2 103.5 calls, 5.5 ref 102-21.75

- 10,300 TYX2 110.25 puts, 38-39 ref 111-29

- Block, 5,000 TYX2 110 puts, 38 ref 111-30

- 4,000 TYX 109/110 put spds, 9

- Blocks, total 10,000 TYX2 112.5/113.5 call spds, 23-24 ref 111-29 to -27.5

EGBs-GILTS CASH CLOSE: German Short End Outperforms Amid Broader Weakness

German bonds outperformed through the 10Y segment while the UK long end outperformed Thursday.

- High German state inflation triggered Bund losses early, which carried through to on the national September CPI release in the afternoon coming in at 10% Y/Y vs expectations of 9.5% coming into the session.

- Several ECB speakers reiterated that a 75bp hike was likely in October, though the terminal rate dipped 3bp to the lowest since Sep 23 under 2.90% and Schatz outperformed.

- Long-end Gilt yields fell sharply alongside a GBP rebound on news that the OBR could get a full fiscal forecast by end-Oct. The BoE's bond buying op saw fairly low takeup again (GBP1.5bln), while appearances by Ramsden and Pill brought little new.

- BTP spreads widened as Reuters reported the ECB saw no need to activate TPI to cap Italian yields.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.8bps at 1.818%, 5-Yr is up 1.4bps at 2.042%, 10-Yr is up 7.3bps at 2.193%, and 30-Yr is up 14.4bps at 2.161%.

- UK: The 2-Yr yield is up 10.9bps at 4.402%, 5-Yr is up 15bps at 4.442%, 10-Yr is up 13.5bps at 4.147%, and 30-Yr is up 3.6bps at 3.968%.

- Italian BTP spread up 6bps at 246.9bps / Spanish up 0.7bps at 118.7bps

EGB Options: Large Long-Dated Euribor Call Spread Features

Thursday's Europe rates / bond options flow included:

- ERH4 99.75/100.00 call spread bought for 1.5 in 50k

- DUZ2 106.30/106.00 put spread in 5k bought for 11 vs DUZ2 107.60 call in 2.5k sold at 25

Late Equity Roundup, Off Late Session Lows

Stock indexes trading weaker but off second half lows after the bell where SPX focus had turned to 3600.00 -- round number support after ESZ2 futures fell to 3623.0 low, nearly testing Wed's pre-open low of 3615.75. Currently, SPX eminis trade -85 (-2.28%) at 3647.25; DJIA -521.82 (-1.76%) at 29165.26; Nasdaq -343.8 (-3.1%) at 10708.85.

- SPX leading/lagging sectors: Energy sector (-0.07%), Health Care (-0.98%) and Financials (-1.12%). Laggers: Utilities (-3.78%), Consumer Discretionary (-3.44%) weighed by auto and component shares, and Information Technology (-2.95%) as hardware and semiconductor shares underperform software makers. Notable late session headline from Meta announcing a hiring freeze and warning employees of restructuring.

- Dow Industrials Leaders/Laggers: Travelers (TRV) +1.69 at 154.61, Visa (V) +0.44 at 179.62, Merck (MRK) -0.21 at 86.57. Laggers: carry over weakness for Apple (AAPL) -8.15 at 141.69 after they annd lower IPhone production on softer demand Wed, Boeing (BA) -8.41 at 125.03, United Health (UNH) -5.36 at 508.58.

E-MINI S&P (Z2): Short-Term Gains Considered Corrective

- RES 4: 4313.50 High Aug 18

- RES 3: 4234.25 High Aug 26

- RES 2: 3983.16/4175.00 50-day EMA / High Sep 13

- RES 1: 3783.25/3936.25 High Sep 23 / 20

- PRICE: 3634.50 @ 1500ET Sep 29

- SUP 1: 3600.00 Round number support

- SUP 2: 3558.97 1.382 proj of the Aug 16 - Sep 7 - 13 price swing

- SUP 3: 3506.38 1.50 proj of the Aug 16 - Sep 7 - 13 price swing

- SUP 4: 3453.78 1.618 proj of the Aug 16 - Sep 7 - 13 price swing

S&P E-Minis trend conditions remain bearish following last week’s extension lower and the bearish follow through this week. Short-term gains are considered corrective. The move lower strengthens bearish conditions and attention is on key support at 3657.00, the Jun 17 low. This support has been pierced. A clear break would confirm a resumption of the broader downtrend and opens 3600.00 next. Initial firm resistance is at 3936.25, Sep 20 high.

COMMODITIES: Crude Oil Consolidates Yesterday's Corrective Bounce

- Crude oil consolidates yesterday’s strong gains as it edges down although not before gaining earlier in the session as supply risks from Russia and OPEC offset economic-driven demand concerns, with some downside pressure from Hurricane Ian leaving Gulf platforms undamaged. Attention begins to turn to the OPEC+ meeting scheduled Oct 5 with production cuts expected to be mandated.

- WTI is -1.1% at $81.23, doing little to change yesterday’s corrective bounce with support still seen at $76.11 (1.618 proj of Jul 29- Aug 16 - 30 price swing).

- Brent is -1.1% at $88.36, still holding above support at the bear trigger of $83.65 (Sep 26 low).

- Gold is -0.03% at $1659.4 after yesterday’s surge saw a pause in the downtrend. Initial technical levels are defined by Wednesday’s range, with resistance at $1662.7 and support at $1615.0.

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/09/2022 | 0145/0945 | ** |  | CN | IHS Markit Final China Manufacturing PMI |

| 30/09/2022 | 0600/0700 | * |  | UK | Quarterly current account balance |

| 30/09/2022 | 0600/0700 | *** | | UK | GDP Second Estimate |

| 30/09/2022 | 0630/0830 | ** |  | CH | retail sales |

| 30/09/2022 | 0645/0845 | *** |  | FR | HICP (p) |

| 30/09/2022 | 0645/0845 | ** | | FR | PPI |

| 30/09/2022 | 0645/0845 | ** | | FR | Consumer Spending |

| 30/09/2022 | 0700/0900 | * | | CH | KOF Economic Barometer |

| 30/09/2022 | 0755/0955 | ** |  | DE | Unemployment |

| 30/09/2022 | 0830/0930 | ** | | UK | BOE M4 |

| 30/09/2022 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 30/09/2022 | 0900/1100 | *** |  | EU | HICP (p) |

| 30/09/2022 | 0900/1100 | ** | | EU | Unemployment |

| 30/09/2022 | 0900/1100 | *** |  | IT | HICP (p) |

| 30/09/2022 | 1100/1300 | | EU | ECB Elderson in Discussion at Uni Amsterdam | |

| 30/09/2022 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 30/09/2022 | 1230/0830 | | US | Richmond Fed's Tom Barkin | |

| 30/09/2022 | 1300/0900 | | US | Fed Vice Chair Lael Brainard | |

| 30/09/2022 | 1345/0945 | ** | | US | MNI Chicago PMI |

| 30/09/2022 | 1400/1000 | *** | | US | Final Michigan Sentiment Index |

| 30/09/2022 | 1500/1100 | | US | Fed Governor Michelle Bowman | |

| 30/09/2022 | 1500/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 30/09/2022 | 1530/1730 | | EU | ECB Schnabel Panels La Toja Forum | |

| 30/09/2022 | 1600/1200 | ** | | US | USDA GrainStock - NASS |

| 30/09/2022 | 1630/1230 | | US | Richmond Fed's Tom Barkin | |

| 30/09/2022 | 2015/1615 | | US | New York Fed's John Williams |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.