Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

- Gilts outperform Bunds, with curves flattening slightly

- AUD/USD narrows gap with key support

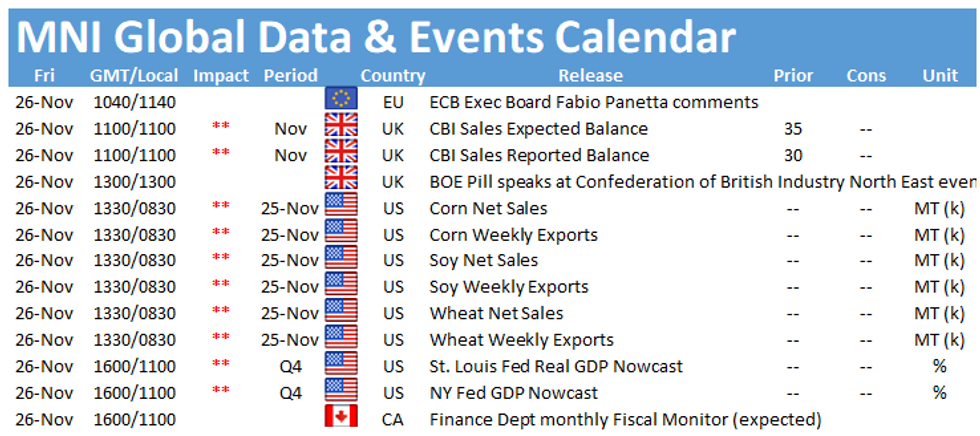

- Focus turns to Australian retail sales, Eurozone money supply

BONDS: Constructive Session For Core Europe, Gilts Outperform

Global core bonds strengthened modestly Thursday, in a session largely devoid of market-moving headlines or trades due to the US Thanksgiving market closure.

- Gilts outperformed Bunds, with both the UK and German curves flattening slightly. Periphery EGB spreads widened <1bp vs 10Y Bunds.

- Unsurprisingly, Treasury futures traded on very light volumes and well within the prior session's ranges.

- In Europe, the accounts of the November ECB meeting suggested among other things that official inflation forecasts would likely be revised up in December (no market reaction).

- Friday's session likewise set to be quiet with another US holiday-shortened session, though a few European speakers (including Lagarde, Schnabel, and BoE's Pill) are on the agenda.

Levels:

- Dec Bund futures (RX) up 47 ticks at 171.01 (L: 170.6 / H: 171.03)

- Dec Gilt futures (G) up 49 ticks at 125.95 (L: 125.52 / H: 125.98)

- Dec 10-Yr US futures (TY) up 1.5/32 at 129-28 (L: 129-24 / H: 129-28.5)

- Dec BTP futures (IK) up 37 ticks at 150.47 (L: 150.17 / H: 150.73)

- Italy / German 10-Yr spread 0.4bps wider at 130.6bps

FOREX: Thanksgiving Holiday Prompts Tight G10 Ranges

- Overall, the greenback traded marginally in the red on Thursday with a mixed and subdued performance across G10 currencies. EUR firmed slightly above 1.1200 but remained in a 32-pip range. NZD and CHF were underperformers, both falling around a quarter of one percent. EURCHF edged back toward the key 1.0505 pivot point.

- Strength in the Swedish krona was a standout after the Riksbank signalled it could start reducing the size of its balance sheet even earlier than their forecast to raise rates from zero in 2024. Broad SEK strength was seen against both the euro and the dollar, in the region of 0.6%.

- In emerging markets, USDMXN traded with a supportive tone, rising around 0.65%. Ongoing concerns regarding the new central bank governor-elect have prompted the pair to hover just below the 2021 highs of 21.6357.

- Aussie retail sales are due overnight before Eurozone M3 money supply data during the European session. The US Treasury is also due to publish their report on international economic and exchange rate policies.

FX OPTIONS: Expiries for Nov26 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1150-60(E503mln), $1.1275-80(E612mln), $1.1380-1405(E598mln), $1.1500-14(E1.1bln)

- USD/JPY: Y113.65-80($1.3bln), Y115.50($582mln)

- GBP/USD: $1.3400(Gbp963mln)

- AUD/USD: $0.7200(A$524mln), $0.7240-50(A$597mln)

- USD/CAD: C$1.2520-25($1.8bln), C$1.2545-55($2.9bln)

- USD/CNY: Cny6.3750-60($500mln), Cny6.4000($650mln), Cny6.4550-55($1.2bln)

Price Signal Summary - Bunds Approach A Key Short-Term Support

- In the equity space, S&P E-minis remain below Monday's high. In pattern terms, the candle formation on this day is a shooting star and still highlights a potential short-term top. If correct, this leaves support at 4625.25 exposed, the Nov 10 low. That said, the contract has recovered off Tuesday's low and this is potentially encouraging for bulls. Key resistance is Monday's high of 4740.50. A break would confirm a resumption of the uptrend. EUROSTOXX 50 futures managed to find support yesterday just ahead of the 50-day EMA - at 4235.50 today. This average marks a key support parameter and a breach is required to signal the next leg lower. For now, yesterday's low of 4236.50 does suggest a potential short-term base. An extension higher would open 4409.50, Nov 18 high.

- In FX, trend conditions are unchanged in the USD and the uptrend remains firmly intact. EURUSD objectives are now set at; 1.1185 Jul 1, 2020 low and 1.1128, 1.764 projection of the Jan 6 - Mar 31 - May 25 price swing. GBPUSD traded lower yesterday. The focus is on 1.3304, the Dec 22, 2020 low. USDJPY remains in its uptrend. The pair has breached the 115.00 handle. This confirms a resumption of the uptrend and the focus is on 116.09, the 1.764 projection of Apr 23 - Jul 2 - Aug 4 price swing.

- On the commodity front, Gold remains vulnerable following this week's move lower. The short-term objective is the base of the bull channel drawn from the Aug 9 low. The channel base intersects at $1756.2 today.

- In the FI space, Bund futures, despite having pulled back this week, remain above key short-term support at 170.06, Nov 5 low. A break of this level would suggest potential for a deeper pullback. While it holds, it can still be argued that the recent pullback is a correction. Gilts traded lower yesterday and breached support at 125.40, Nov 17 low. This undermines the recent bullish theme and highlights the potential risk of a deeper sell-off. An extension of the pullback would expose 124.25, the Nov 1 low.

EQUITIES: EuroStoxx Futures Snap Six Session Losing Streak

- European equity markets traded well in the absence of US traders, with EuroStoxx50 futures adding just over 10 points to snap a six session losing streak. Europe's utilities and real estate sectors drove the recovery off the Wednesday low, with tech names not far behind. Communication services and energy names were the sole sectors to trade in the red Thursday.

- US futures remained open for trade despite the closure of cash markets, with the e-mini S&P partially reversing strength seen across the Asia-Pac session. Nonetheless, the e-mini S&P traded above the 4700 level, cementing the underlying strength in equities.

COMMODITIES: Oil Treading Water Ahead Of OPEC+

Little moves in oil or gold prices today on US Thanksgiving. Further Covid restrictions have weighed on oil prices but the moves have been limited amidst very low volumes, treading water ahead of next week's OPEC+ meeting.

- The OPEC+ meeting on Dec 2 will decide whether or not to go ahead with the 400k bbl/d planned increase.

- There were conflicting sources on the likely outcome yesterday, with Saudi Arabia and Russia in favor of a pause but others seemingly willing to proceed. Russia might have difficulty boosting output in winter.

- WTI is -0.3% at $78.13, still comfortably between the $80.68 (Nov 16 high) required for short-term bullish conditions and the key short-term support of $74.76 (Nov 22 low).

- Brent is almost flat at $82.23, slightly closer than WTI to the resistance level of $83.14 (Nov 16 high).

- Gold is near enough unchanged today, currently $1789.9 after sliding earlier in the week. It remains vulnerable near recent lows, below the 20- and 50-day EMA, and with attention on the base of a bull channel at $1756.2.

MNI London Bureau | +44 203-865-3809 | edward.hardy@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok